- Euro to Dollar Analysis: EUR/USD boosted by firmer risk appetite

- Investors eye key US data: Core PCE today, ISM services PMI and NFP next week

- Rising oil prices could weigh on the EUR/USD

Welcome to another edition of Forex Friday, a weekly report in which we highlight selected currency themes. In this week’s report, we will focus the US dollar, EUR/USD and oil prices.

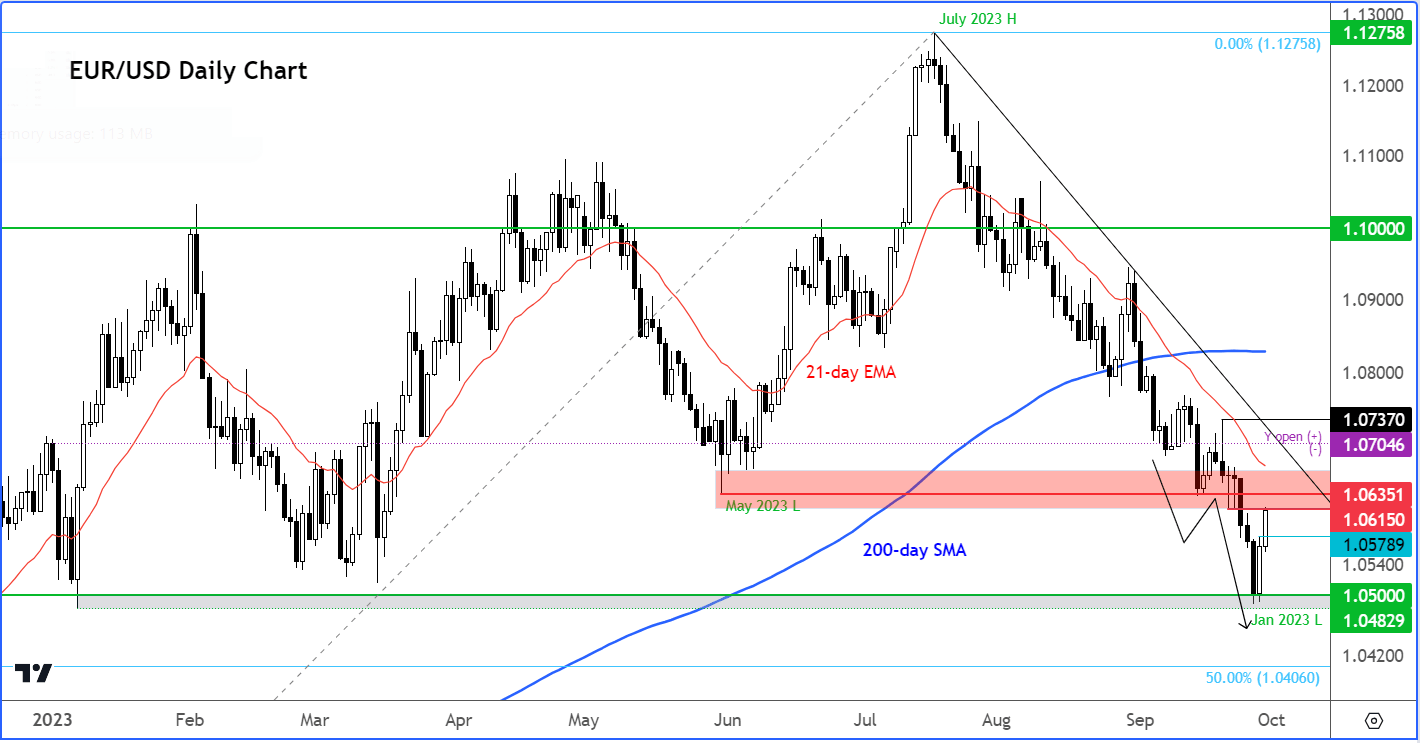

Despite softer Eurozone inflation and German retail sales data, the EUR/USD climbed for the second day in the first half of Friday’s session. It was supported because of firmer risk tone across financial markets, driven by a weakness in US dollar and global bond yields. The popular trading pair was testing a key resistance zone around 1.0615-1.0635 at the time of writing, with investors looking forward to the publication of key US inflation data. The dollar was also lower against other major currencies, while US index futures were extending their recovery from the day before, rising alongside European markets and government bond prices. So, the EUR/USD recovery was aided primarily by a softer dollar and firmer risk appetite, rather than any improvement in Eurozone’s macro-outlook. This gives me doubt that the recovery will last, unless we see further evidence of a shaper slowdown in US economy. Keep an eye on oil prices as they are on the rise again, which could weigh on risk appetite, and therefore the EUR/USD, once more.

Euro to Dollar Analysis: EUR/USD boosted by firmer risk appetite

After heavy selling pressure comes a big bounce. That’s precisely what happened yesterday with global markets recovering sharply off their lows, before extending those gains into the first half of today’s session. Ironically, Thursday’s bounce in stocks appears to have been triggered by softer-than-expected US data. The rationale is that weaker data will discourage the Fed from tightening its belt further, and simultaneously increases the chances of a sooner-than-expected rate cuts. But let’s not jump into any conclusions as the monthly data can be quite volatile. The Fed looks at the trend of data than month-over-month volatility. More evidence is needed to reverse the sharp bullish repricing of US monetary policy that has helped to propel the dollar to new highs on the year and bond yields to their highest levels since 2007.

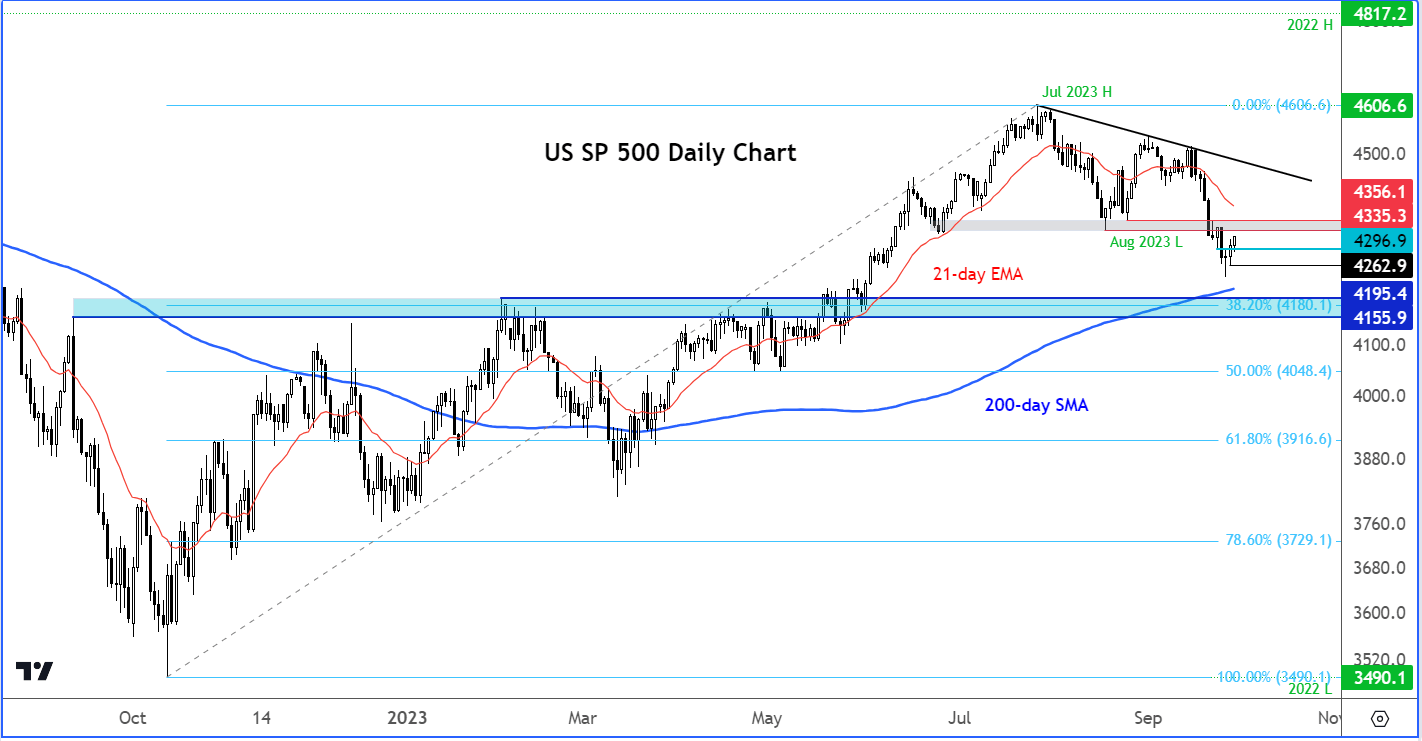

The S&P is now near a potential resistance zone around 4335, so it could head lower again and driven the EUR/USD lower with it:

Bad news = good news for risk assets?

Thursday’s recovery in the EUR/USD coincided with the stock markets reversing earlier losses, which happened around the time when US pending home sales came in much softer. They plunged 7.1% in August from the month before after the 0.9% monthly increase recorded in July. This was a LOT worse than expected (-1.0%). We also found out that GDP was left unrevised, against expectations of a positive surprise.

The EUR/USD also failed to react negatively to softer Eurozone data released earlier today, which is bizarre. Actually, not so bizarre when you consider the fact that the EUR/USD is positively correlated with the stock market. Softer data means no more rate increases by the ECB, which is good news for stocks. Anyway, German retail sales fell 1.2% month-over-month versus 0.5% expected, while Eurozone annual CPI eased 4.3% on the headline and 4.5% on the core front, both lower than expected (4.5% and 4.8%) and below the previous month’s prints (of 5.2 and 5.3 percent, respectively).

Investors will be looking forward to some more important data releases, starting today with the Core PCE Price Index. Next week's economic calendar will include the likes of the ISM Services PMI and the monthly jobs report to look forward to, among the key data highlights.

US Core PCE Price Index

Friday, September 29

This is the Federal Reserve's preferred gauge for inflation, so the market will be watching it closely. It is expected to cool to 3.9% from 4.2% on an annual basis, while the month-over-month print is expected to complete a hattrick of 0.2% reading. Meanwhile, personal spending is expected to rise 0.5% after a 0.8% increase in July. Hotter-than-expected inflation and stronger-than-forecast spending would support the Fed’s more hawkish stance and could lift the US dollar higher once again.

US ISM Services PMI

Wednesday, October 4

The Fed’s tightening cycle may not be over just yet, as macro indicators in the US have remained relatively upbeat compared to the rest of the world, though the market feels like it is probably done. The dollar bulls will be looking for further evidence in incoming data, such as Wednesday’s ISM Services PMI, to support the Fed’s view. But if we now start to see a trend of weaker data emerge, then this will call into question the Fed’s strong inclination towards rate cuts being pushed further out in 2024, with the possibility of one more hike before the end of this year.

US nonfarm payrolls report

Friday, October 6

Concerns over interest rates remaining high for longer in the US has caused lots of volatility in recent weeks. Until Thursday’s reversal, we had seen a sharp sell-off in stocks while bond yields climbed to levels last seen before the global financial crisis. The market is worried about inflation and oil prices remaining high, which could call for one more rate increase before the end of 2023, or keep rate cuts off the table until at least H2 of 2024. So, as well as the headline jobs number, this month’s wages data should be monitored closely. A bigger rise in wages should support the dollar.

Euro to Dollar Analysis: Rising oil prices could weigh on the EUR/USD

More concerning for investors and central banks right now is the rising prices of crude oil, which should make stagflation even worse for oil-importing countries in the Eurozone, Japan and China, among others. This comes as borrowing costs have skyrocketed across the developed economies. In the US mortgage rates surged to a 23-year high this week, providing yet another blow to the housing market. According to Freddie Mac, the rate on the average 30-year fixed mortgage increased to 7.31% from 7.19% the week prior, reaching levels last seen in the year 2000.

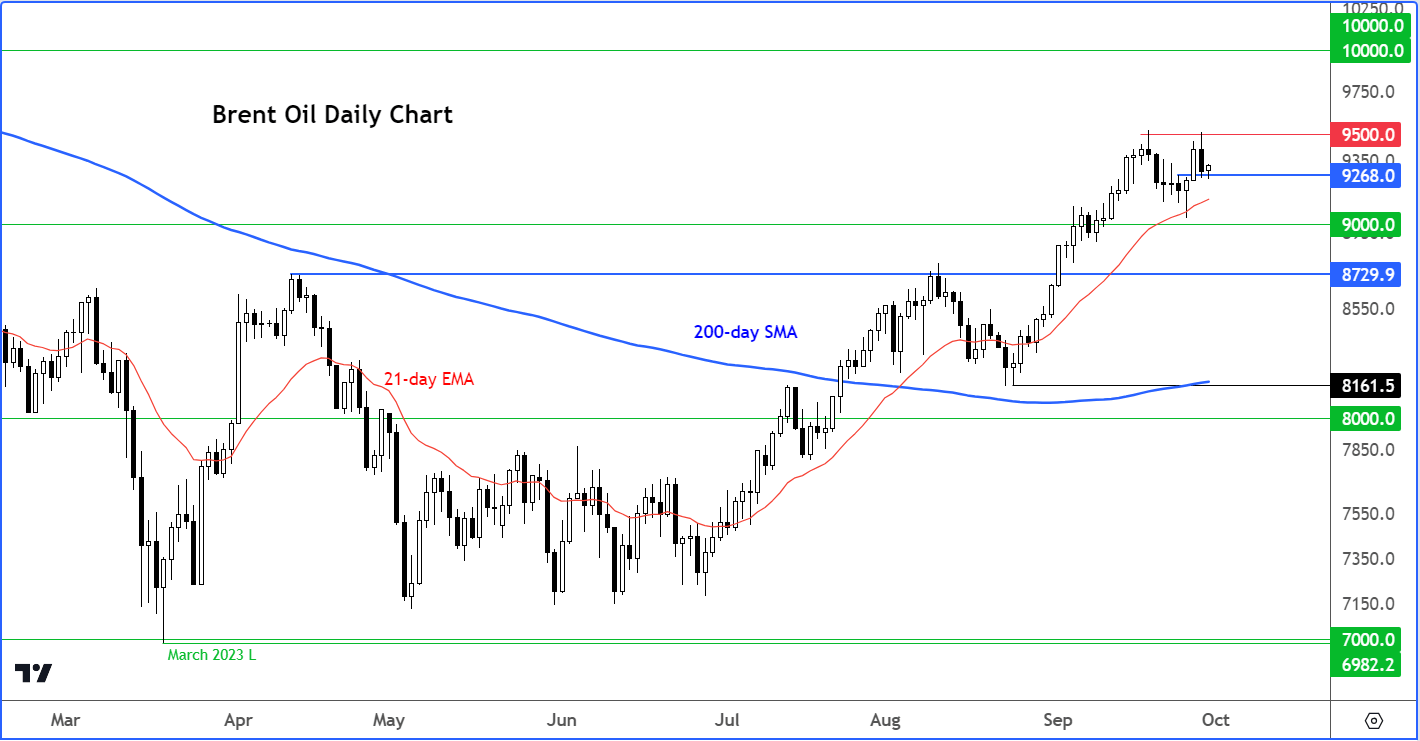

Brent oil is finding support right where it should, at $92.50 to $93.00 area. It looks like it was wants to head towards $95 again, a closing break above which could pave the way for $100 next:

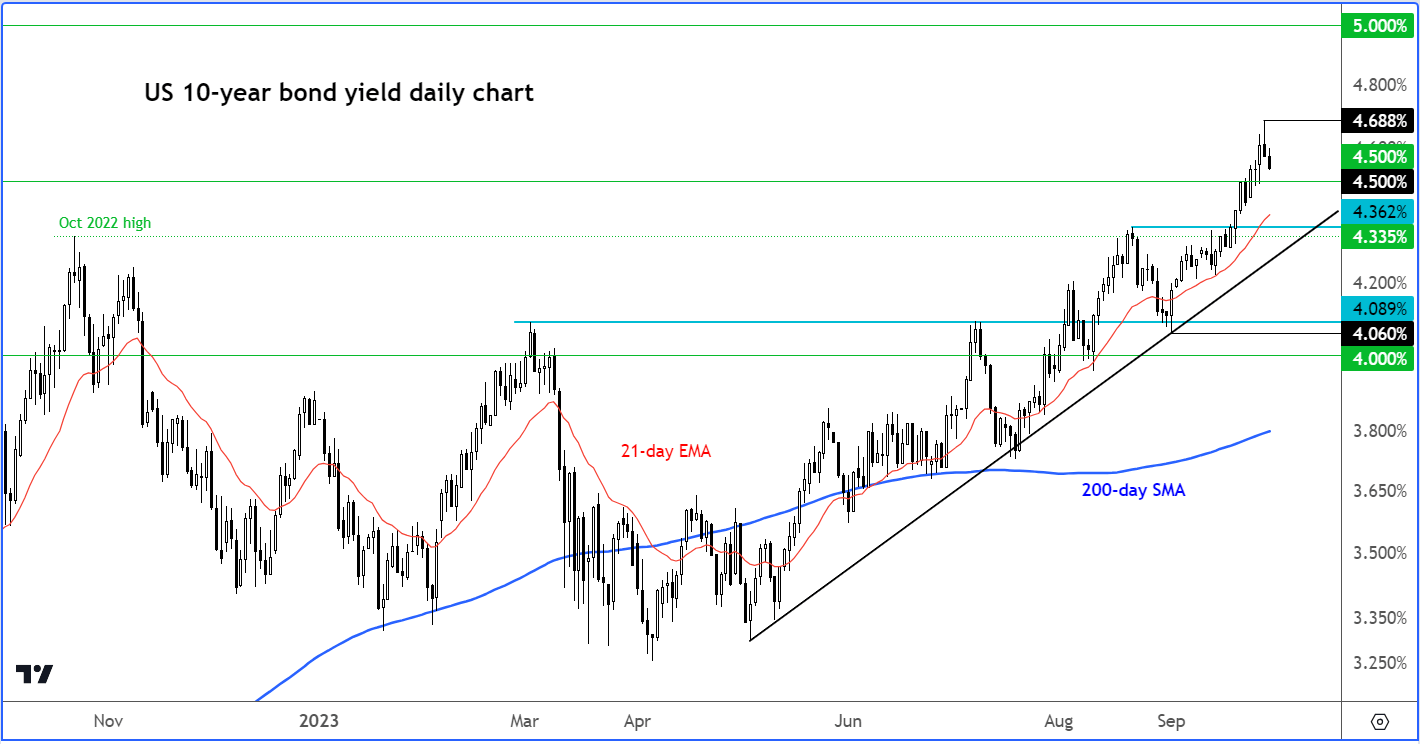

If crude oil were to rise again, this could further fuel inflation worries and thus drive bond yields higher again. Keep an eye on the 10-year yields, as they remain inside a larger uptrend, despite the two-day pullback:

So, taking everything into consideration, I think that the risks remain skewed to the downside for the EUR/USD and it could start heading lower from around the current levels of 1.0615ish.

Source for all charts used in this article: TradingView.com

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 10:19 PM

Yesterday 06:59 PM

Yesterday 04:50 PM

Yesterday 01:18 PM

Latest EUR/USD articles

Yesterday 05:43 AM

April 29, 2024 04:03 AM

April 23, 2024 04:19 AM

April 22, 2024 03:42 AM