- EUR/USD outlook: US bond auction, CPI and consumer sentiment survey in focus next

- DAX outlook improves by relief rally, but will the optimism last?

- Chinese CPI in deflation – good or bad thing?

- DAX technical analysis: 16,000 key level to reclaim

European stock markets were able to recoup Tuesday’s sharp losses in the first half of Wednesday’s session, which also helped to fuel a modest recovery in the risk-sensitive EUR/USD pair. Sentiment improved for two reasons, but whether the recovery will hold remains to be seen. First, there was some clarity on Italian government’s windfall tax on banks that had weighed heavily on the sector yesterday. So, today’s bounce is nothing more than a relief rally. Second, data out of China showed CPI was in deflation for the first time since January 2021, boosting hopes that China can export disinflation to the rest of the world still suffering from high levels of inflation. This raises an important question: will we see another weaker-than-expected US CPI report on Thursday? But will the stock market rally hold given that China is struggling, while concerns over valuations remain high, and the fact that there is the lack of fresh news to drive sentiment?

DAX outlook: European stocks stage relief rally

Italian banks were leading the recovery after Tuesday’s sharp falls. This helped to lift the FTSE MIB more than 2% higher, while the rest of the European indices also climbed. So, everything that had fallen on the back of yesterday’s announcement from the Italian government of a surprise windfall tax on bank profits, reversed. There was little clarity on the details of the new tax, but now that the government confirmed that the levy won’t exceed 0.1% of each bank’s asset, this was met with relief.

But will the optimism last?

Apart from the clarity on Italy’s tax on bank profits, there are other factors at play, which may cap the gains for European and US indices moving forward. This is especially the case for the financial sector after ratings agency Moody’s cut the credit ratings for 10 small and midsize US lenders. There are also worries about valuations after the big rally on Wall Street lifted the major indices near record levels this year, at a time when sales growth has been particularly weak.

Chinese CPI in deflation – good or bad thing?

Concerns over China is another reason why investors might err on the side of caution. While falling Chinese prices is good news on the inflation front, CPI in deflation territory is indicative of a weak economy.

Chinese inflation was in deflation at an annual pace of -0.3% last month. This was the first time since January 2021 that prices deflated in China, which is important because China is the world’s largest exporting nation. This means that the rest of the world can buy things cheaper from China, which should translate into weaker inflation globally, everything else being equal.

However, deflation in China is a sign of weakness in the economy, which may mean less demand from China for products and services from the rest of the world. This is something that was highlighted in the trade data earlier this week, showing weaker-than-expected import figures. In fact, imports were very weak, falling 12.4% from last year in July compared to forecasts of a fall of just 5%. Exports declined 14.5% vs 12.5% expected, plunging by the most since the height of the pandemic in early 2020.

US CPI and consumer sentiment survey in focus next

Investors will turn their attention towards consumer inflation data, due on Thursday. US CPI inflation has fallen sharply in recent times, printing below-forecast readings in each of the past 4 months. Annual CPI fell to just 3.0% in June from around 6.5% at the start of the year, increasing the likelihood that interest rates have now peaked.

But services inflation remains high as strong wage growth continues to push up input costs. This is something that was highlighted in the NFP report, which showed average hourly earnings rising 0.4% month-on-month or 4.4% year-on-year, which was more than expected. Annual earnings have now increased by 4.4% in April, May, June and July. This shows that wage inflation is still going strong, and it is a concern for the Fed. This is especially the case for the services sector – which was also highlighted by the rise in prices paid index of the ISM services PMI.

So, there is a risk that CPI could overshoot expectations on Thursday. But with the manufacturing sector clearly struggling, and now jobs market softening a little, the Fed will feel that its policy is restrictive enough to help cool price pressures further. So, a small beat wouldn’t matter too much.

The Fed’s policy decision in September will be entirely data dependent. Until then, we will have one more inflation report after this week’s one. Any further weakening of CPI could cement expectations of a policy hold. But the Fed will also monitor other macro indicators, including consumer confidence. On Friday, we will have the latest reading on the University of Michigan’s Consumer Sentiment and Inflation Expectations surveys.

A goldilocks outlook in the US is what stock market investors on Wall Street have been enjoying this year – until the recent weakness. They will be looking for signs that the health and sentiment of the consumer remains positive, enough not increase the risks of a further Fed rate increase, and yet not too depressing to raise recession alarm bells. Somewhere in between could support stocks. FX investors will have already had the and inflation report to consider along with the UoM consumer sentiment and inflation expectations surveys. If most of these indicators point to strength in the US economy, then this should keep the dollar supported on the dips. But the bigger risk is tilted towards to the downside as most of the positive influences have already been mostly priced in, if not fully.

EUR/USD outlook could be impacted by bond auction

There are no major data out of the eurozone to impact the EUR/USD outlook today, which means the popular currency pair may only find direction from the general direction of risk appetite – or lack thereof – until the release of the US CPI on Thursday (see above).

So, the US dollar will continue to trade sideways after finding good support tat the start of the week. Clearly, many traders are unwilling to open any bold positions ahead of the key risk event this week i.e., US CPI on Thursday.

That said, the greenback could weaken if risk sentiment improves further. Yesterday, the 3-year US Treasury note auction resulted in a slightly lower yield than expected, suggesting that demand for US debt is not as badly affected by Fitch’s ratings downgrade as some had feared. There are bigger auctions taking place today and tomorrow of $38bn in 10-year notes and $23bn in 30-year notes, respectively. Given that these are long-dated bonds, they should be watched more closely.

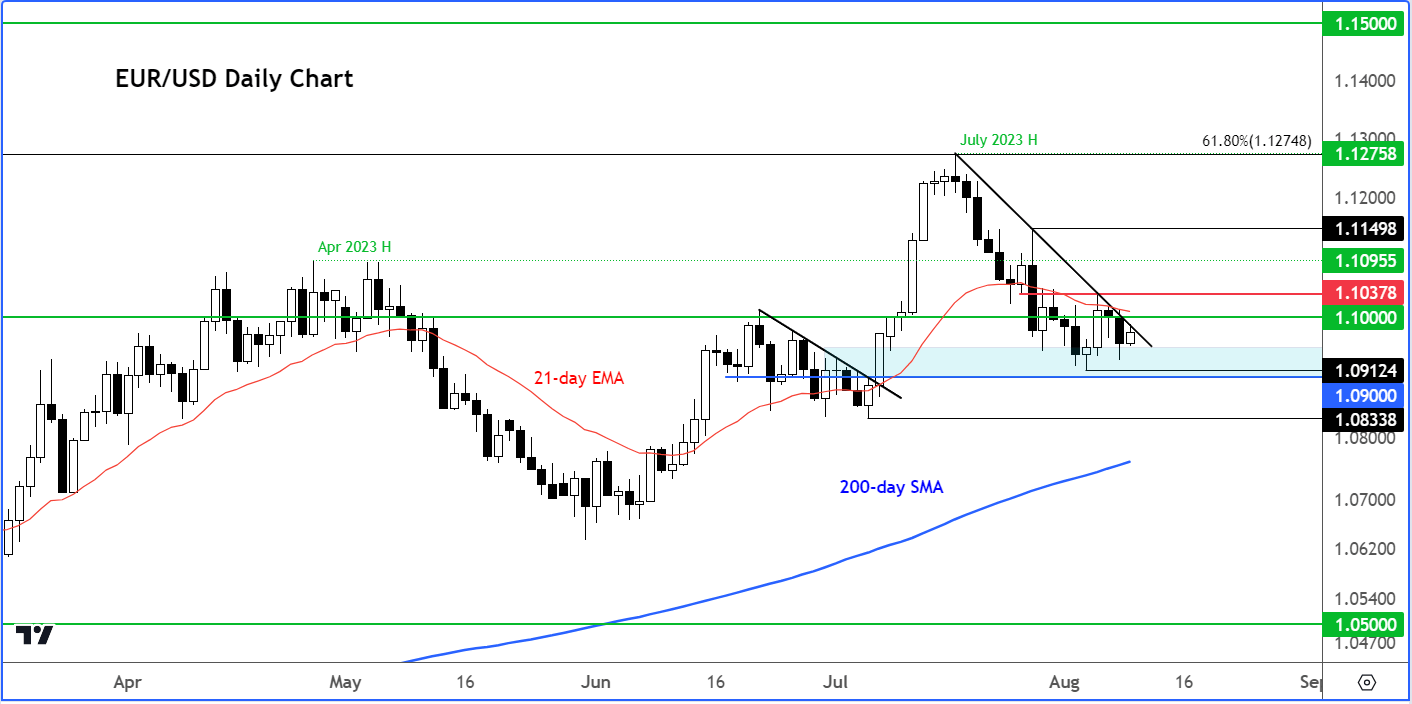

EUR/USD outlook: Technical analysis

After being unable to reclaim broken support around 1.1030-1.1050 area following Friday’s rally, the EUR/USD dipped back into the key support area around 1.0900-1.0920 area on Tuesday, before bouncing back. While it remains stuck between these ranges, the EUR/USD outlook remains uncertain from a technical view point.

But the underlying strength in the euro means the EUR/USD could bottom out soon. A couple of euro crosses like the EUR/AUD and EUR/NZD have broken to new highs on the year recently, pointing to strength in the single currency.

So far, we haven’t seen any signs of a bottom for the EUR/USD. But a break above that 1.1030-1.1050 resistance range could be a sign the bulls are waiting for.

The line in the sand is at 1.0833, the low from July. Any move below that level would nullify this year’s bullish trend because we will then have a lower low in the EUR/USD.

But clearly, the onus is on the bulls. They will need to show up and fast. Perhaps a potentially weaker US CPI could trigger the recovery on Thursday.

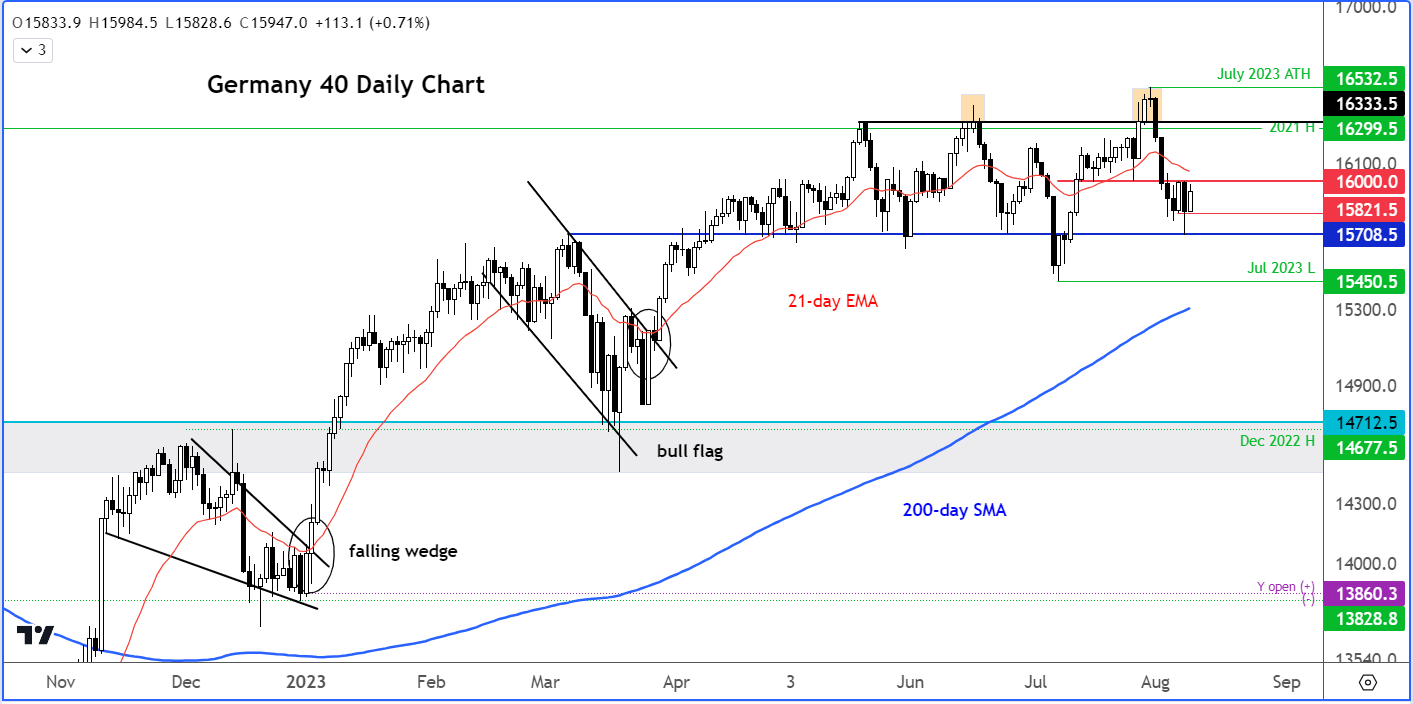

DAX technical analysis

As mentioned in my report on Tuesday, the DAX was testing a key support area where I expected to see a recovery.

While the markets were in full risk-off mode on Tuesday, the retreatment was taking place inside a larger bullish trend. As such, many investors were still looking to buy the dip, because they have missed out on the rally or took profit at higher levels and want to go back in.

So, I was expecting to see a rebound – even if it ultimately didn’t last long. And that’s precisely what happened around the 15700-15720 area on the DAX. This is where the German index had rallied from in July. It has now arrived near that support-turned-resistance area around the 16K mark, where the earlier rally had stalled at the time of writing.

With the market recently moving below the short-term 21-day exponential moving average, the near-term path of least resistance is still technically bearish until proven otherwise. A potential move back above 16,000 would therefore be a welcome sign for the bulls as this would invalidate the bearish bias.

However, in the event of a bullish no-show around here, there is a risk the DAX could fall back to re-test that big support area again around 15700-15720… and if that area eventually breaks then the July low at 15450 would become the next downside target for the bears to attack.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Source for charts used in this article: TradingView.com

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 08:00 PM

Yesterday 01:03 PM

Yesterday 12:52 PM

Yesterday 12:11 PM

Latest EUR/USD articles

May 1, 2024 05:43 AM

April 29, 2024 04:03 AM

April 23, 2024 04:19 AM

April 22, 2024 03:42 AM