* Please note - the next European Open report will be on Monday 19th July

Asian Indices:

- Australia's ASX 200 index rose by 6 points (0.08%) and currently trades at 7,338.10

- Japan's Nikkei 225 index has fallen by -73.7 points (-0.26%) and currently trades at 28,644.43

- Hong Kong's Hang Seng index has fallen by -161.94 points (-0.58%) and currently trades at 27,801.47

UK and Europe:

- UK's FTSE 100 futures are currently down -1.5 points (-0.02%), the cash market is currently estimated to open at 7,123.22

- Euro STOXX 50 futures are currently down -1.5 points (-0.04%), the cash market is currently estimated to open at 4,093.06

- Germany's DAX futures are currently down -8 points (-0.05%), the cash market is currently estimated to open at 15,781.64

US Futures:

- DJI futures are currently down -107.37 points (-0.31%)

- S&P 500 futures are currently up 11.25 points (0.08%)

- Nasdaq 100 futures are currently down -3.5 points (-0.08%)

Learn how to trade indices

Indices and futures lower ahead of Powell Testimony

Asian share markets tracked Wall Street lower after the US inflation report knocked equities from their record highs. Japan’s markets broke a two-day winning streak which saw the Nikkei initially lose -0.8% before recovering to around -0.26%. China’s CSI300 is trading -0.9% and one of the worst performers, the Hang Seng is off -0.6% although the ASX 200 is 0.1% higher despite Sydney extending its lockdown in Sydney. Futures markets are a touch lower for US and Europe which points to a softer open.

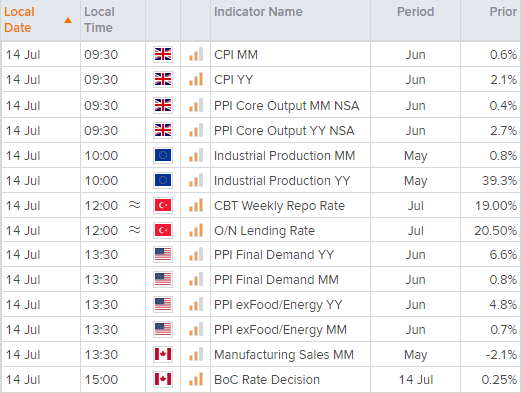

Today’s main event is for Jerome Powell’s testimony in front of congress at 17:00 BST. He could face some tough questioning over such a loose policy, given inflation rose to a 30-year high yesterday. Therefore, any signs of weakness in his responses may be construed as tapering coming sooner (and at a faster pace) than presently suggested, in turn bringing forward expectations for hikes to send the US dollar higher and equities lower. Although, as exciting as that sounds, it’s more likely he’ll stick to his ‘inflation is transitory’ script.

FTSE 350: Market Internals

FTSE 350: 4088.73 (-0.01%) 13 July 2021

- 81.48% of stocks closed above their 200-day average

- 58.97% of stocks closed above their 50-day average

- 19.66% of stocks closed above their 20-day average

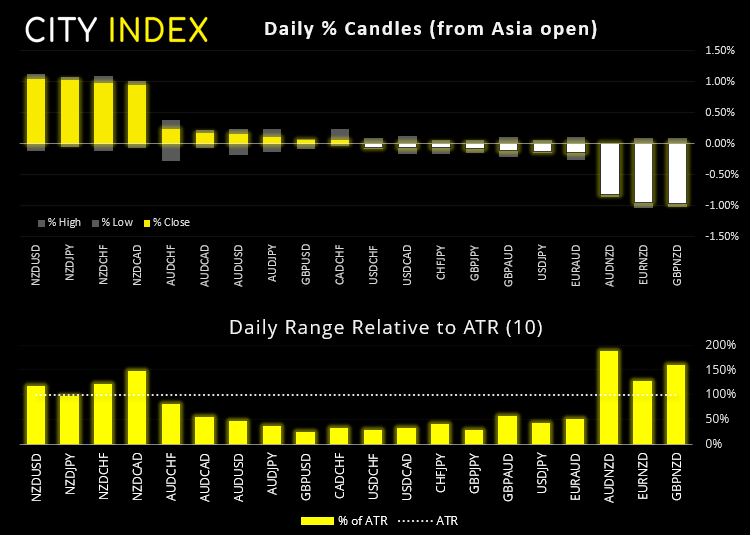

Forex: NZD soars following RBNZ’s less dovish meeting

As it can be clearly seen on the forex dashboard, it was all about the New Zealand dollar in overnight trade. RBNZ confirmed they will halt their LSAP (Large Scale Asset Purchase Programme) by July 23rd which sent the Kiwi dollar sharply higher across the board. Their outlook on the economy was a net-positive although reiterated their view of transitory inflation (sound familiar?) and that risks form COVID-19 remain.

Already ANZ bank have revised their call to now see a hike in August, which was recently bought forward to November just two weeks ago. That one is up for debate as RBNZ still maintain inflation to be transitory, and they’re not likely to want to be ‘first in’ on the hiking path.

NZD/CAD is probing the July high ahead of today’s BOC meeting. As mentioned in the Asian open report, if BOC disappoint with their level of expected tapering then it could help NZD/CAD hold onto early gains from the RBNZ meeting. So far, so good. Of course, the risks here is that BOC do taper which puts a damper on upside potential for this cross.

GBP/NZD was the biggest downside mover overnight falling -1.00% and reaching 150% of its 10-day ATR. Yet the volatility award goes to AUD/NZD which fell around -0.8% but hit around 200% of its 10-day ATR.

GBP/USD is trading around yesterday’s lows after rolling over form 1.3900. It’s holding above 1.3800 and the weekly S1 pivot and trying to hold above the broken trendline outlined in yesterday’s European report. So, we see the potential for a minor bounce from current levels but, if the US dollar index breaks above 92.80 resistance then we should see GBP/USD break below 1.3800. Keep an eye on UK inflation data scheduled for 09:30 BST.

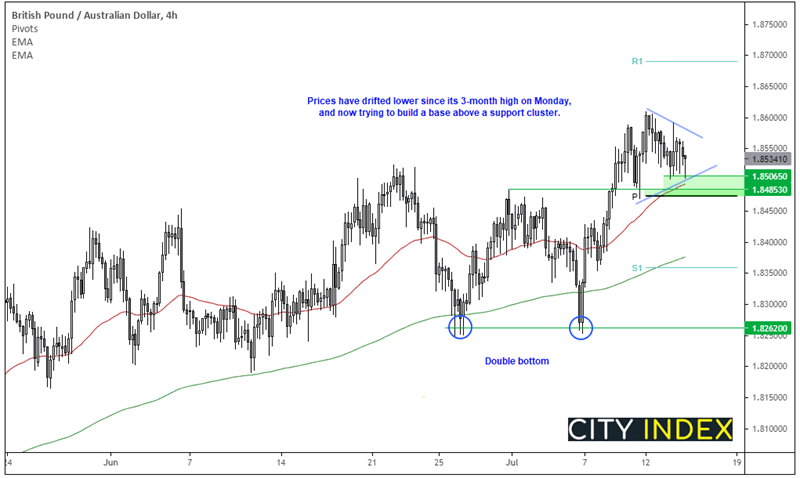

GBP and AUD are both lower this week, but perhaps a stronger than expected CPI print can help support GBP/AUD. It’s been trending higher since the January low and recently hit a three-month high before retracing gently lower. It is now trying to build a base above the support zone mentioned on Monday, so we’d consider a bullish engulfing candle or bullish reversal pattern around current levels to be a clue that momentum is about to pop higher once more.

Learn how to trade forex

Commodities:

Copper futures were slightly lower following the stronger dollar and higher inflation yesterday. But, like most metals at present, they remain between key support and resistance levels and are struggling to breakout during summer trade.

WTI has edged lower from its 5-day high overnight, although we remain bullish above 73.68 (yesterday’s low. Although bullish patterns around or above the weekly pivot at 74.13 could be of interest for bulls.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Indices articles

July 25, 2024 01:30 PM

July 25, 2024 01:01 AM

July 25, 2024 12:41 AM

July 24, 2024 07:26 PM