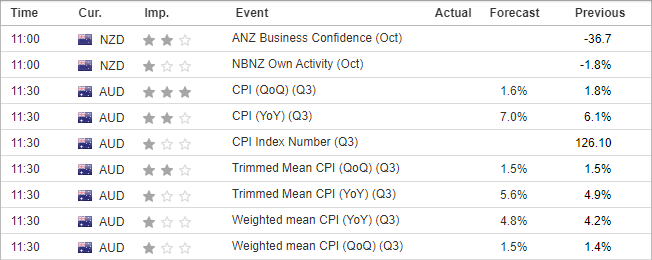

Inflation rose 6.1% y/y in Q2 and is expected to rise to 7% - which would be its highest level since 1990 and more than twice the RBA’s 2-3% target band. The quarterly read is expected to soften to 1.6%, down from 1.8% - which seems feasible given the newly released monthly CPI read softened slightly to 6.8% m/m from 7% m/m.

However, the RBA pay more attention to the Trimmed Mean and Weighted CPI prints, which are also widely above the RBA’s target. Trimmed mean is expected to rise to a record high of 5.6% yet remain at 1.5% q/q for a second consecutive quarter, whilst the Weighted CPI is expected to rise to 4.8% - its highest level since 2008 – and the quarterly read to rise to 1.5% (1.4% previously).

It is no secret that the RBA were late to respond to inflationary forces seen across the globe – based on the premise that ‘it was different in Australia’. Alas, inflation is here and it is indeed rising. And the RBA expect it to rise further, and estimate 2022 inflation to land at 7.75% before pulling back to around 3% over 2024.

Yet the RBA surprised markets with a mere 25bp hike at their last meeting, and interest rates are just 2.6% which is well below current rates of inflation. Yet during a testimony to the House of Representatives, RBA Governor Lowe pointed out that inflation expectations remain anchored – and it makes more sense to base policy decision on expectations of future inflation over current levels of inflation. For reference, the 5-year breakeven rate is around 2.4% and as the RBS said in their October statement, “Medium-term inflation expectations remain well anchored, and it is important that this remains the case”.

In a nutshell, whilst inflation expectations continue to behave then the RBA are in no rush to hike rates aggressively. Cash rate futures currently imply a 68% chance of a 25bp hike, and have fully priced in a 3% cash rate by their December meeting (although two meetings of 25bp would take rates to 3.1%).

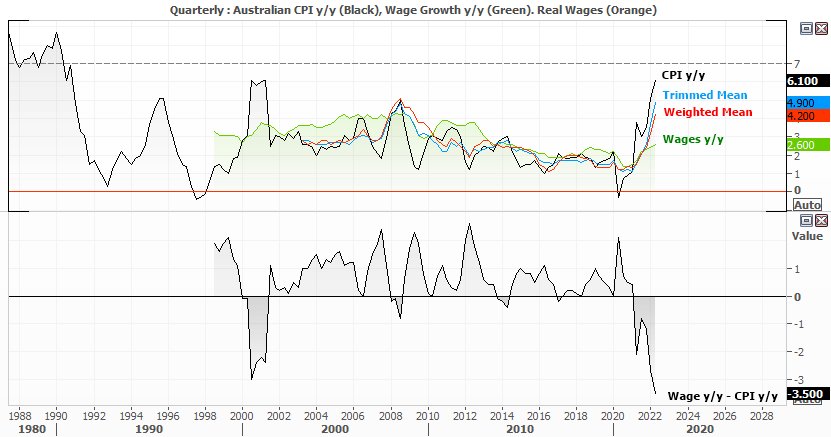

So from a policy perspective, tomorrow’s inflation report is unlikely to change the course of the RBA’s direction. Although if prices come in hotter than expected (like we saw with New Zealand last week) it could send the Aussie higher as it places pressure on the RBA to hike more aggressively. Not that they want to, or likely will anyway - especially as wage growth remains relatively tame compared to inflation.

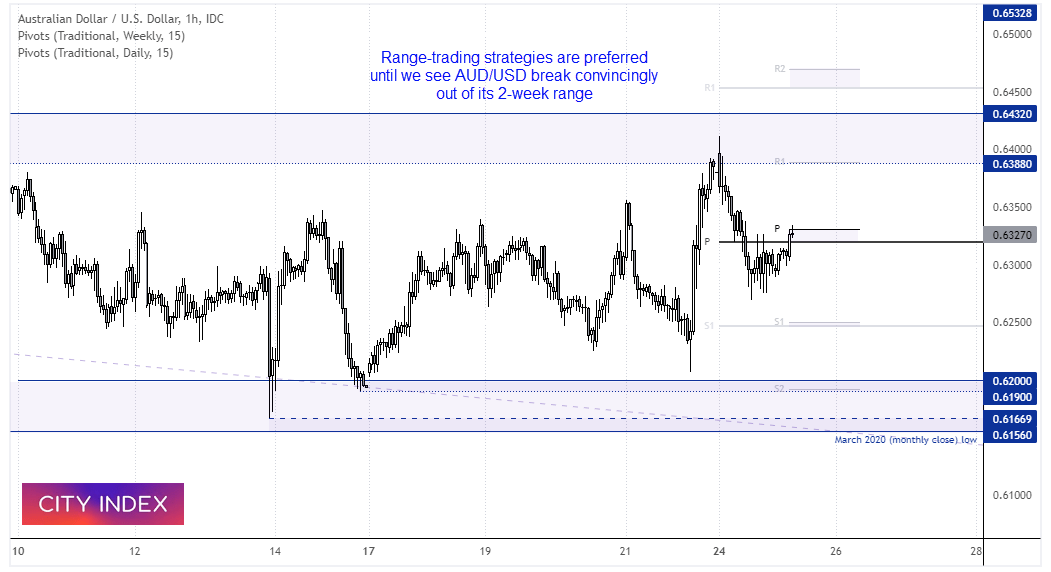

AUD/USD 1-hour chart:

The Aussie has been confined to a range over the past two weeks. This has made it frustrating for breakout trader, but a delight for range traders. It does not come as a huge surprise that prices have held above the 2020 (close) low, due to the significance of the level. And the longer it holds as support, the higher the odds favour a break higher (in theory). But until we see a decent break of its current range, bears will likely be tempted to fade into rallies into resistance and bulls seek to buy dips around support.

How to trade with City Index

You can easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM