Asian Futures:

- Australia’s ASX 200 futures are down -2 points (-0.027%), the cash market is currently estimated to open at 7318.1

- Japan's Nikkei 225 futures are down -70 points (-0.25%), the cash market is currently estimated to open at 27978.94

- Hong Kong's Hang Seng futures are up 199 points (0.8%), the cash market is currently estimated to open at 25036.85

European Friday close:

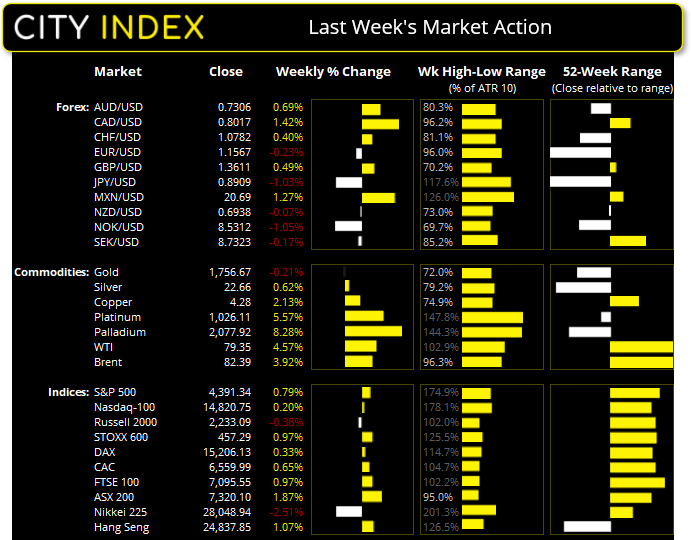

- UK's FTSE 100 index rose 17.51 points (0.25%) to close at 7095.55

- Europe's Euro STOXX 50 index fell -25.05 points (-0.61%) to close at 4073.29

- Germany's DAX index fell -44.73 points (-0.29%) to close at 15206.13

- France's CAC 40 index fell -40.2 points (-0.61%) to close at 6559.99

US Friday close:

- The Dow Jones fell -8.65 points (-0.02%) to close at 34,746.25

- The S&P 500 fell -8.42 points (-0.2%) to close at 4,391.34

- The Nasdaq 100 fell -76.385 points (-0.51%) to close at 14,820.75

Global indices bounce from corrective lows

Indices were higher overall last week (excluding the flailing Nikkei 225) as equities recovered from their multi-week corrections with the aid of risk-on sentiment. News that Biden and Xi are to speak by the end of the year signalled tensions between the two major powers were thawing, and the US government will avoid a historic default as the Senate voted to extend the debt ceiling until December. We suspect that the correction for global equities of the past few weeks is now complete.

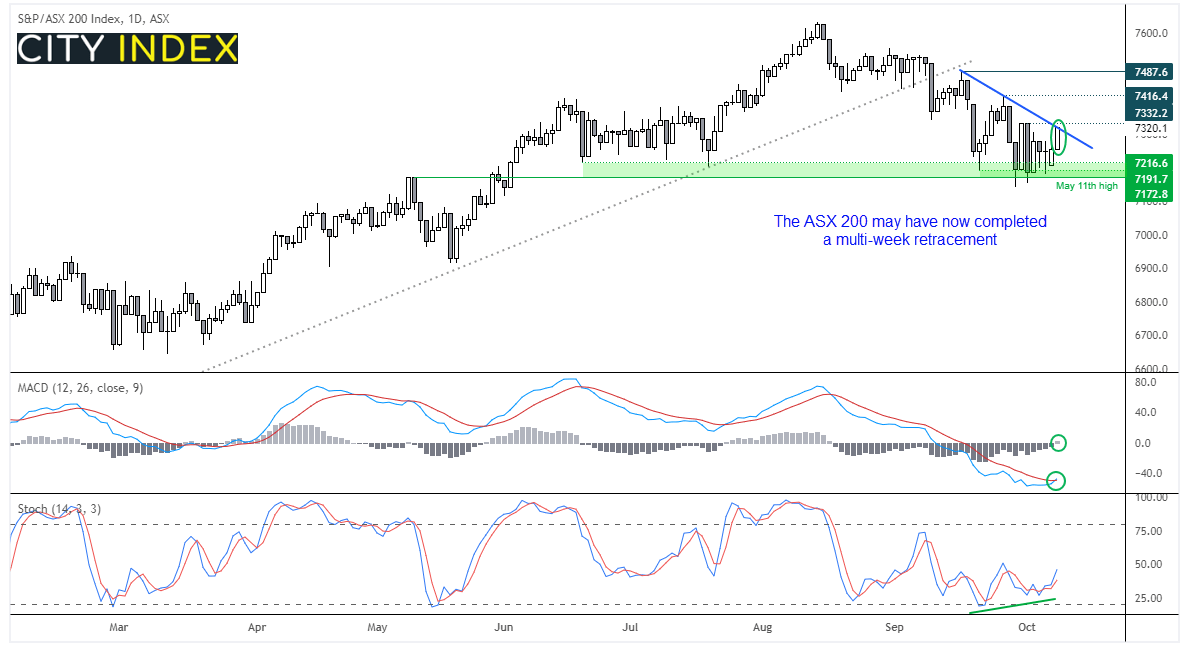

If the MACD is to be believed, the ASX 200 may have seen a significant low at the end of September and its bullish run could be set to resume, as it generated long-term buy signal on Friday. Note the histogram has been rising and flipped to positive territory on Friday, and a bullish divergence also formed on the stochastic oscillator.

It closed back above 7300 on Friday to a 1-week high and tested trend resistance. We are now seeking a break above the 7332.20 high in line with last week’s bias and hope to see it extend Friday’s breakout from compression.

ASX 200 Market Internals

ASX 200: 7320.1 (0.87%), 09 October 2021

- Materials (1.77%) was the strongest sector and Industrials (0.15%) was the weakest

- 11 out of the 11 sectors closed higher

- 4 out of the 11 sectors outperformed the index

- 140 (70.00%) stocks advanced, 54 (27.00%) stocks declined

- 64% of stocks closed above their 200-day average

- 42.5% of stocks closed above their 50-day average

- 49.5% of stocks closed above their 20-day average

Outperformers:

- + 7.4%-Chalice Mining Ltd(CHN.AX)

- + 5.7%-Hub24 Ltd(HUB.AX)

- + 5.6%-Magellan Financial Group Ltd(MFG.AX)

Underperformers:

- -14.6%-EML Payments Ltd(EML.AX)

- -3.51%-Clinuvel Pharmaceuticals Ltd(CUV.AX)

- -3.29%-Whitehaven Coal Ltd(WHC.AX)

Canadian dollar dominated the forex arena:

The Canadian dollar was the strongest major currency last week thanks to hawkish comments from BOC’s governor, higher energy prices and stronger economic data (PMI and employment). CAD/JPY hit our target our 90.0 and was the strongest pair on Friday. USD/CAD extended losses, fuelled by the weaker headline NFP print and a stronger-than-expected Canadian employment report.

The Australian dollar was also higher on thawed tensions between the US and China, whilst the mild risk-on tone for equities cemented JPY’s place as the weakest major currency of the week. Yet AUD/USD failed to break convincingly higher from its inverted head and shoulders. AUD/NZD however did rise to a 9-week high in line with our bullish bias.

If you look across all yen pairs it looks like we could be entering a decent phase of risk-on, as each pair appears to have completed a multi-month correct and momentum is now pointing higher. Whilst CAD/JPY is the clear winner, even weaker majors such as EUR and GBP appear set to rally against the yen. We just need price action to now confirm that expectation.

Volumes will be lower in the US session as some exchanges are closed for Columbus Day.

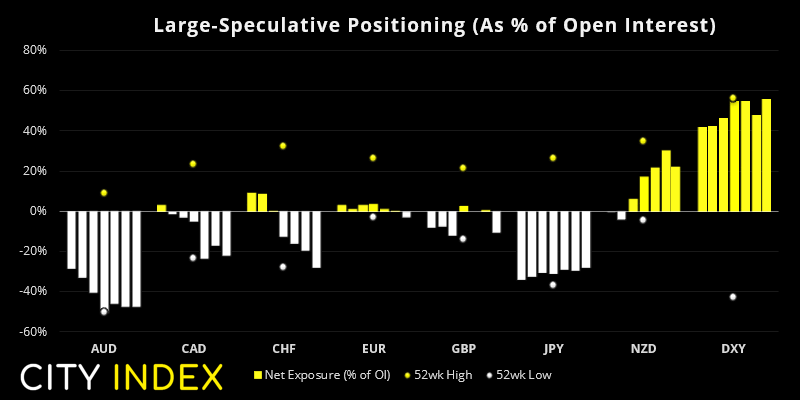

From the Weekly COT Report (Commitment of Traders)

From Tuesday

- According to data compiled by IMM, markets increased net-long exposure to the USD against other currencies by US +$7.2 billion, taking it to a total of $22.5 billion – its highest level since June 2019.

- Net-long exposure to the US dollar index (DXY) hit a 2-year high.

- Traders flipped to net-short exposure on EUR, GBP and BRL futures.

- With traders now net-short 22.3k contracts on EUR futures, they are their most bearish on the anti-dollar since March 2020.

- Large speculators increased net-short exposure to CHF futures for an 8th consecutive week, which takes them to their most bearish level since December 2019.

- Short exposure to AUD futures hit a new record, although there was a slight increase in both gross longs and shorts. Given prices remain elevated we suspect there could be more short covering to follow.

Commodities: The lows could be in for palladium and platinum

It was an uneventful week for gold and silver, which have essentially closed each week and covered little ground over the past three. However, palladium and platinum is where the action was, which rose 8.3% and 5.6% respectively. In palladium’s case it found support at its 50-month eMA and 200-week eMA, which are pretty strong technical levels to break. We therefore suspect we have seen the lows for now.

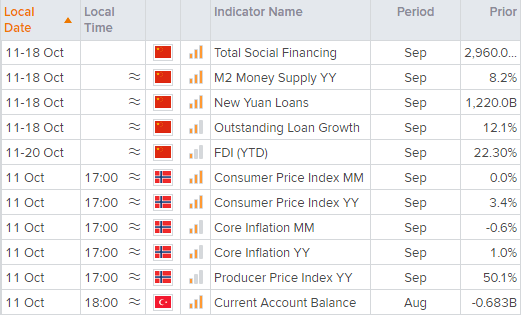

Up Next (Times in AEST)

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM