week ahead what happens after the fed 2683622016

Post Fed opportunities: blood on the streets for G10 FX Sky and the Fox takeover: Sky Falls, probably… Indices: 20,000 for the Dow Jones Commodities: […]

Post Fed opportunities: blood on the streets for G10 FX Sky and the Fox takeover: Sky Falls, probably… Indices: 20,000 for the Dow Jones Commodities: […]

1, Post Fed opportunities: blood on the streets for G10 FX

EUR/USD is taking the brunt of the dollar surge post Wednesday’s Fed meeting. It has traded as low as 1.0395 in the London session on Thursday, however, 1.04 proved to be a sticky level and cushioned the blow to the single currency, at least in the short-term. The single currency has had a double whammy of central bank action recently, first the dovish ECB, then the market’s hawkish reaction to the Fed, which has seen it drop more than 450 points since the intra-day high on 8th December.

EURUSD: Is parity on the cards?

The risk of a decline to parity in EUR/USD has increased, due to the sheer ferocity of the move in the buck in the last 24 hours. However, we will be watching the German- US sovereign yield spread very closely in the coming days, as relative yields are a big driver of FX. The 10-year spread is close to its lowest ever level at -2.3%, but the 2-year spread is worth watching. This is currently -2%, the low from 1997 was -2.75%. While there is still more room on the downside for this spread (and thus, for the EUR/USD rate) considering Treasury yields have already risen so sharply since Trump won the US Presidential election, if we see some selling fatigue in the Treasury market (bond prices move inversely to yields), then the euro may be spared.

Why the surge in the dollar:

The market’s reaction seems out of proportion to Fed chair Yellen’s more moderate press conference. The market isn’t reacting to what the Fed did, or will do in 2017, but rather using it as an excuse to herald in the era of Trumpenomics and boom-bust growth cycles. Animal spirits are driving this decline in the bond market and the subsequent rise in the US dollar. Eventually fatigue will set in. However, considering this is a powerful trend, the dollar may not retreat for some time, but when the pullback comes, the dollar bulls should be ready.

USD/JPY: 120.00 cometh

The Fed meeting has made life above 120.00 in USD/JPY very likely in the coming weeks. The high over the past year was 123.56, reached on 18th December 2015. Interestingly, after USD/JPY reached that high, it sold off sharply until late summer 2016, so if we do move back to the 123.00 zone, we will be watching to see if this pair can sustain its uptrend beyond this level.

The key driver of USD/JPY going forward will be the market’s perception of two things: firstly, if Trump can deliver on his fiscal plans to boost growth, and secondly, if the Fed will deliver on its planned three rate hikes in the coming year, when in the past it has been known to under-deliver on the rate hike front. With USD/JPY tracking the US –Japanese 10-year yield spread so closely: over the past year this correlation has been 0.55%, since the start of this month the correlation has surged to over 80%, and 90% since the start of this week, where yields go, so too does USDJPY. Interestingly, the yield spread looks like it has run ahead of itself, as you can see in the chart below, so even if there is further upside to go in USD/JPY, we would urge caution if you decide to go long at these high levels.

Figure 1:

Source: City Index and Bloomberg

2, Sky and the Fox takeover: Sky Falls, probably…

There was an air of inevitability over Fox’s second attempt to snatch up Sky when the news filtered into the market recently.

So, the mildly negative share price reaction following news of an agreed deal on Thursday last week is little surprise. Sky had already run up around 40% since talk of the deal started filtering into the market on 6th December.

The lack of surprise factor doesn’t explain the 1% slide of Sky’s stock entirely though. Customary pre-offer jockeying by investors aside, Sky shares trading below the £10.75 offer price points to some scepticism.

Such doubts do not—this time—ride primarily on the regulatory side. Critics of the spit between Rupert Murdoch’s Fox and News Corp can rightly point to the permeability of the divide given that his son is chairman of Sky and is Fox’s CEO. In terms of governance though, the point is a non-starter now. It is the matter of valuation where material grievances lie.

To begin with, Sky is worth 14% less than it would have been had the Brexit vote not happened, implying the stock would have closed at £9 on the day before Fox officially announced its intention to make a firm offer. (In reality it closed at £7.895).

So the 36% premium to Sky’s 8th December close offered by Fox looks more like a 19% mark-up, factoring in sterling’s devaluation. We assume that was the rationale behind calls from one of Britain’s largest pension fund groups this week for an “appropriate” premium. The independent committee of directors Sky set up to consider the deal has also faced polite pressure.

Political momentum from a mixture of concerns over press freedom and on concentration of media ownership could yet cause the Murdochs a few sleepless nights. However our assessment points to noise rather than material opposition. We don’t expect the Secretary of State for Media and Culture to refer the deal to the U.K. competition regulator. That should leave the shares in range and some vocal institutional shareholders disappointed.

It’s certainly possible that the stock could, in time, have recouped all of its 33% loss between January and the year’s low in late November, without a Fox buy-out. That would, however, require a smooth ride for stock markets and the pound into Britain’s official Brexit notification to the EU, probably next March. We would also need to ignore relentless inflation of Premier League broadcast rights, and continuing encroachment by Amazon and Netflix.

Shareholders are likely to vote for jam today, particularly given that only 75% agreement required under the deal’s Scheme of Arrangement structure instead of 90% under a straight takeover.

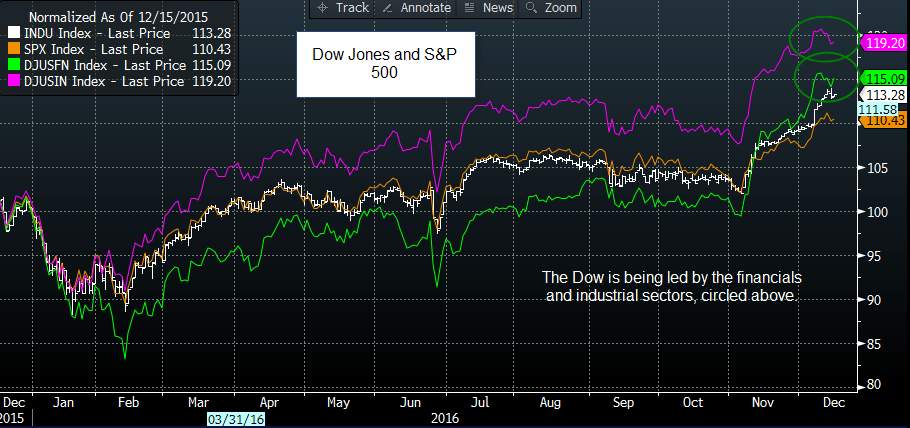

3, US indices: 20,000 on the cards for the Dow Jones

The market’s excitement at the prospect of a Donald Trump Presidency shows no signs of abating. Not even the Federal Reserve’s plans to hike interest rates at a faster pace next year caused a significant disruption of this rally. We believe that, for now, stocks will continue to rally alongside the dollar, and we could see 20,000 in the Dow Jones by the end of this year.

Interestingly, the Dow Jones is outperforming the S&P 500, as you can see in the chart below, we think that this is due to the prevalence of the financial and materials sector in the Dow Jones. These sectors have been leading the rally in US stock markets ever since Trump won the US election, as he is perceived as being positive for banks, by scrapping some Dodd Frank regulation, and for materials and infrastructure businesses, due to his plans to boost fiscal stimulus. In contrast, the SPX 500 has been held back by the relative under performance of defensive sectors like healthcare, and by the tech sector. However, tech has started to make a comeback as stronger US growth is good news for the IT sector.

Overall, we continue to see stocks pushing higher in the coming weeks, as there doesn’t appear to be a convincing reason why the rally should stop. It is also traditionally the ‘Santa rally’ season, with stocks historically performing well at the end of December. We think that the Dow is a pure play on Trumpenomics. At some stage the market will wake up to the threat from higher yields and the potential for a bust scenario after Trump’s fiscal fuelled economic boom, but we doubt that will happen by year end. Instead we see the potential for this index to surge back to the psychologically important 20,000 level, as animal spirits drive financial markets.

The chart below, shows the Dow Jones index (white), the S&P 500 index (orange), the Dow Financials index (green) and the Dow industrials index (purple). Financials and industrial stocks are surging, and driving the strong performance in the Dow.

Figure 2:

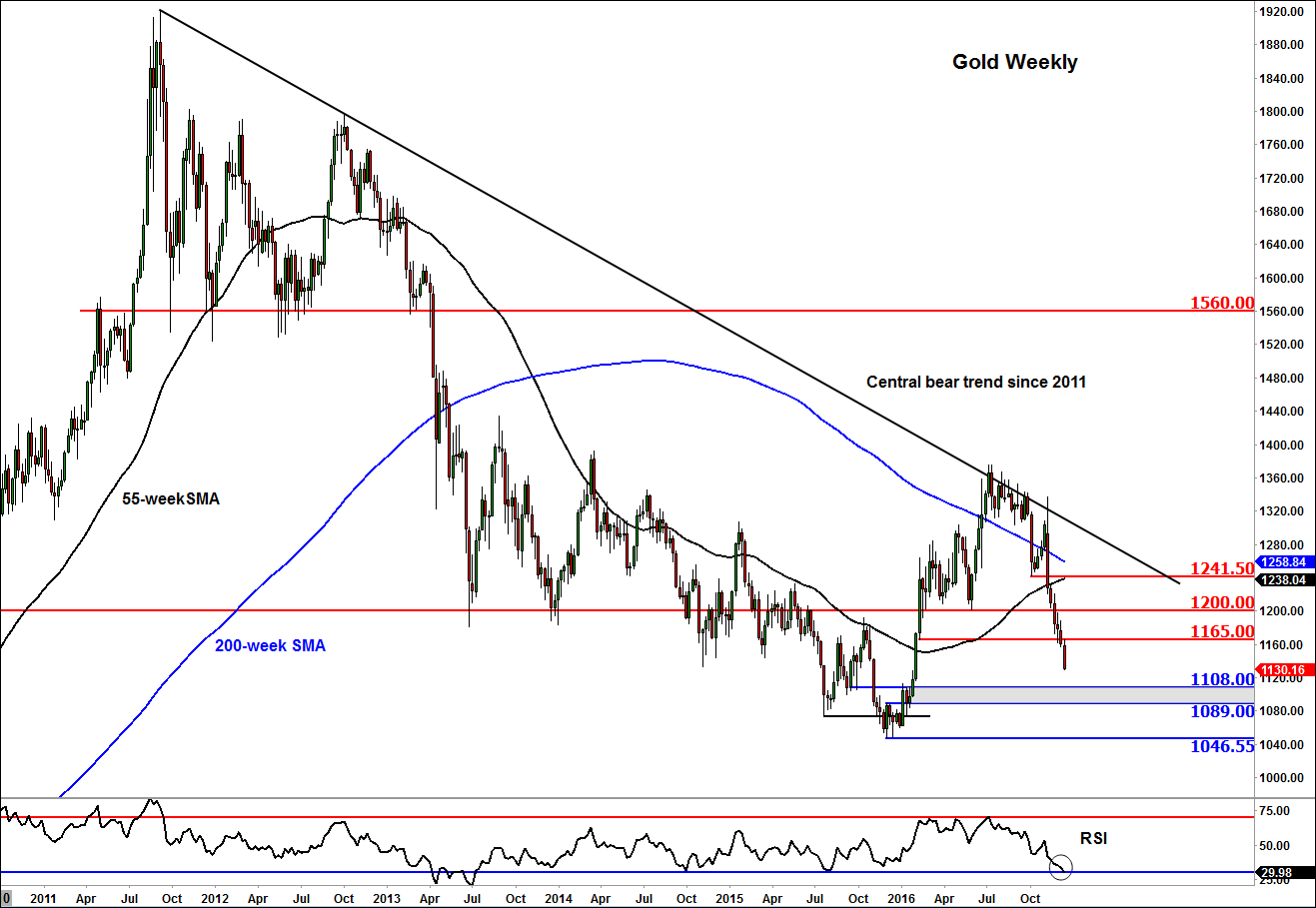

4, Look ahead: Gold

Precious metals have been big victims of the Trump- and now Fed-inspired dollar rally, especially gold. Silver has only just made a lower low relative to last month’s $16.15/20 print, whereas gold is fast approaching its 2015 lows. Thus precious metal bulls may be better off with silver once a bottom is formed, although this could still take a while. Conversely, the bears may be better off with trading gold. Unlike gold, silver has dual usages as both a precious metal and an industrial material, so it tends to do better than the yellow metal when base metals are rising. For now though, both metals are falling and risk sentiment appears be quite positive despite the rising yields and dollar. So far, no one is paying much attention to gold as a hedge against inflation. But this may be something that could help limit the losses for the metal in the coming months. From a technical perspective, there are not many positive things we could say about gold, except that even on the weekly time frame it looks a little bit oversold (see the RSI). The good news is the metal is fast approaching some key support levels around the $1089-$1108 area, which was previously resistance. The bad news is we don’t know if this support area will hold and if it does, for how long. Until there is a break in market structure of lower lows and lower highs, the path of least resistance remains to the downside. We never recommend catching falling knives, unless in a counter trend move and even then only around key support/resistance.

Figure 3:

Source: eSignal and City Index.

5, Look ahead: USD/JPY

The USD/JPY is on steroids. You don’t need the RSI to tell you it is ‘overbought’. But it can remain so for a long period of time, of course. Overbought in itself is not a sell signal, rather it is a sign for caution for existing longs and/or bullish speculators. Price action is clearly bullish, so any potential retracements here needs to be viewed as a pause in the trend, unless there is break in market structure of higher highs and higher lows. With the key 116.00 old support broken in the aftermath of the Fed decision, there are not many big resistances to watch apart from around psychologically-important levels such as 120 and 125. But on the weekly time frame, there is an interesting area around 118.75-119.20, which needs to be watched closely. As per the chart, this area marks the open and midpoint of the last weekly up candle prior to the breakdown sub 116.00. So in the past it was actually here when the selling pressure first started. Thus we may at the very least see a pause for breath here. But if price turns lower, then the initial levels of support to watch include 117.50 and then that 116.00 handle. The technical bias would turn bearish once again if the latter fails to hold as support.

Figure 4:

Source: eSignal and City Index.

{kind=link}

{kind=link}