View our guide on how to interpret the FX Dashboard

FX Brief:

- Currency markets traded in tight ranges whilst traders awaited more clarity over the much-hyped phase-1 trade deal. Meanwhile, US Trade Representative Lighthizer is claiming the deal is “totally done” and will nearly double US exports to China over the next couple of years. Quite rightly, markets clearly want confirmation form both sides before committing.

- Chinese retail sales expanded by 8% YoY versus 7.6% expected, industrial production rise 6.2% versus 5% expected and fixed asset investment rose 5.2% as expected. Separately, China threatened to retaliate if Germany exclude Huawei from 5G.

- A report from NZIER suggested slightly lower growth expectations for New Zealand, whilst consumer confidence remained positive with respondents continuing to feel buoyant about making big ticket purchases. Inflation expectations remained anchored around 2%.

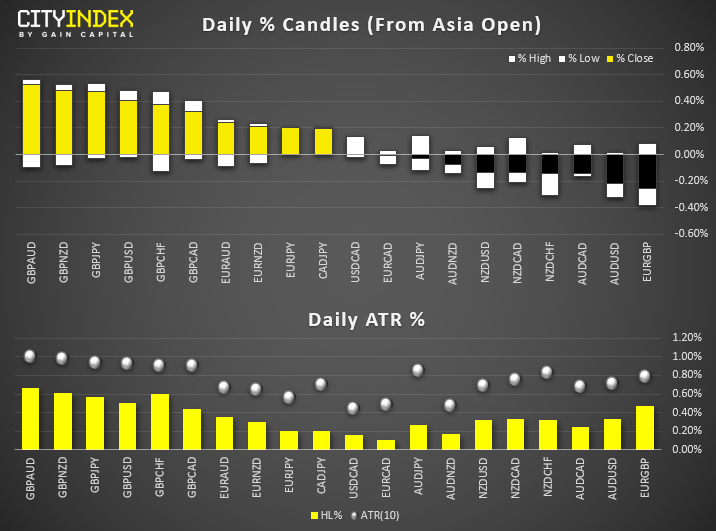

- GBP is the strongest major (and saw the most volatility) whilst JPY and CHF are the weakest. Narrow ranges outside of GBP pairs.

Price Action:

- DXY: Friday’s recovery saw the dollar index retest the trendline it broke on Thursday’s volatile selloff. The trendline also marks today’s high

- AUD/USD: Friday’s bearish outside day saw a reversal at the 200-day eMA to warn of further downside. A break below 0.6864 warns of a run for 0.6800.

- USD/JPY: Friday’s elongated Doji shows solid resistance is at 109.93. Bias remain neutral until we see momentum break out of the indecision candle.

- EUR/USD: The elongated bearish pinbar warns of a reluctance to break above 1.1200 Bias is for it to range between 1.1000 – 1.1200.

- GBP/USD: Potential for further upside although we’d also expect prices to consolidate within Friday’s range whilst the dust settles, following such a volatile spike.

Equities Brief:

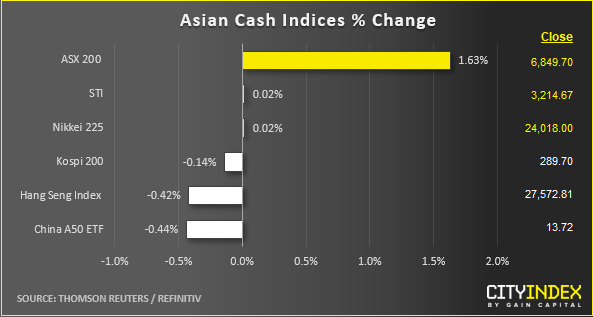

- After a strong performance seen on last Fri, 13 Dec, key Asian stock markets are mostly trading flat after the positive outcome from major risk events; UK General Election and U.S-China Phase One trade deal agreement that has been agreed in principal.

- China’s Industrial Production and Retail Sales for Nov have fared better than expectation; 6.2% y/y versus consensus forecast of 5% y/y and 8% y/y versus consensus forecast of 7.6% respectively. However, caution is warranted due to one-ff seasonal factor and last month ‘s mega online sale “Single Day” event.

- Profit-taking can be seen in China A50 and Hong Kong’s Hang Seng Index that has dipped down by -0.35% dragged down by another round of weekend clashes between ant-government protestors and the police. Also, Chinese Premier Li Keqiang has commented that Hong Kong is not yet of out “dilemma” after a meeting with HK leader Carrie Lam today. This remark from China’s top leadership has suggested that the current situation in Hong Kong may not be returning to “normalcy” soon after a period of extended street protests.

- Australia’s ASX 200 is the best performer today as it rallied by 1.63% which is now just a whisker away from its current all-time high of 6893, that has been rejected for a bullish breakout on 02 Dec 2019 (2nd attempt). Technology stocks are leading the gains such as Nearmap and Appen that have recorded gains of 8.75% and 5.23% respectively.

- The S&P 500 E-Mini futures has recorded a modest gain of 0.30% so far in today’s Asian session to print a current intraday high of 3184, a whisker away from last Fri, all-time high of 3188.

Matt Simpson and Kelvin Wong both contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM