The debt limit stalemate continues as we approach the Memorial Day weekend. With the June 1 deadline now just a stone’s throw away, the pressure is growing on both sides to strike a deal. Will the markets stage a recovery in the event of a deal? That is highly likely. But whether that potential recovery will hold, is what I am not too sure about.

If you take out technology out of the equation and not look at the Nasdaq 100, you will realise the markets are not looking very good for the bulls, and this is not just because of the debt limit uncertainty. This is hardly surprising, thanks to the ongoing weakness in commodity prices, concerns over China and rising bets that the Fed may tighten its belt even more.

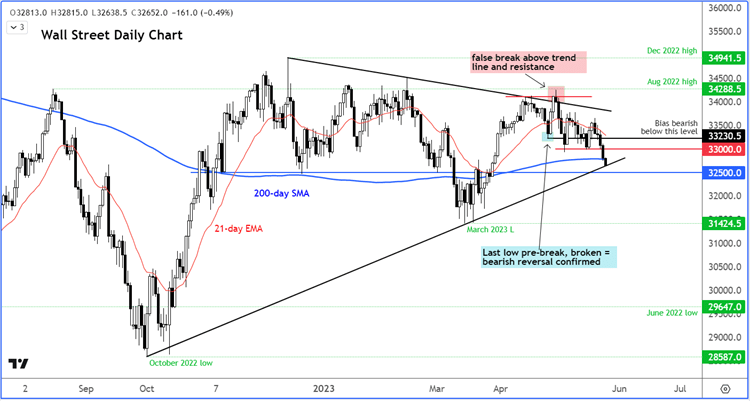

Before discussing the macro factors in detail, let’s take a quick look at the DJIA chart. It is not painting a pretty picture right now.

Dow breaks 200-day, tests trend line

As a debt deal still remains elusive and macro concerns are on the rise, the Dow forecast doesn’t look great, with the index breaking the 200-day average today. But just below the 200-day, there is a bullish trend line which could trigger some buying activity.

Source: TradingView.com

Still, for as long as the lower highs remain in place, even if we see a bounce this wouldn’t not necessarily mean the bear trend is over. Only if and when the index goes back above 33K resistance convincingly, will the bears ease the pressure.

Why are stocks falling?

While the Nasdaq may have hit a new high for the year, thanks to Nvidia, other global indices have continued to struggle today. The German DAX, for example, relinquished its entire gains from last week, before hitting a new low earlier this morning. The FTSE also displayed similar characteristics. Chinese mainland shares turned negative on the year earlier this week. Worries over global growth, US debt ceiling and sticky inflation are all unnerving investors.

The focus remains firmly fixated on the US debt limit situation. A sell-off in the markets was always going to be needed to put pressure on the two sides to make a compromise. Negotiators are still far apart on key issues. They must act quickly to avert a default – and to stop the market turmoil. But have they left it all too late?

It is not just stocks. Sentiment towards nearly all risk assets has turned negative quite abruptly this week. Concerns are on the rise about the health of the Chinese and European economies and fears about the US debt ceiling. You also have a Fed still keen to tighten its policy further, while inflation in some parts of the world continues to remain very high, causing all sorts of problems and hurting the pockets of consumers. Businesses are not doing very well either, especially in the manufacturing sector, as we found out on Tuesday with those weak PMI numbers.

Will we see a relief rally on debt deal?

Well, if we see some concrete signs a debt deal will be reached, I would be expecting a sharp relief rally in the major indices. Whether or not the spoos would go back above 4200 in that event is something I wouldn't bet my life on, simply because there are so many other risks to consider - from China slowing down to the Fed potentially raising rates even further.

The latest from Washington is that it is going to the wire, once again. US House speaker McCarthy said he doesn’t know if they will have a debt deal today.

NVIDIA powers Nasdaq higher – for now

The only bright spot is technology right now after NVIDIA shares jumped a massive 25% on the back of its strong results. But if markets continue to struggle, I don’t think technology would be immune to a sell-off. If anything, rising yields are not meant to be good for stocks that carry low div yields, like many of those found in the Nasdaq. So, watch out for a false breakout on the Nasdaq.

US economy more resilient than expected

Meanwhile, there was more evidence of to suggest the Fed might, after all, raise interest rates further, or at least put off rate cuts for longer. US GDP came in at 1.3% compared to 1.1% expected and reported initially. The GDP deflator was 4.2%, higher than 4.0% expected. Jobless claims surprised, too, printing 229K vs. 249K expected. Following the release of the data, bond yields rose further, as too did the dollar.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Dow Jones articles

July 18, 2024 11:14 PM

July 17, 2024 04:24 PM

July 16, 2024 09:49 PM

July 15, 2024 01:39 PM