Summary of the RBA’s February 2023 statement:

- The RBA hiked the cash rate target by 25 basis points to 3.35%

- Underlying inflation was above expectations at 6.9%

- Strong domestic demand is adding to the inflationary pressures

- CPI is expected to decline this year due to global factors and slower growth in domestic demand

- Medium-term inflation expectations remain well anchored, and it is important that this remains the case

- The labour market remains very tight

- Wages growth is expected to continue picking up due to the tight labour market and higher inflation

- The board will continue to pay close attention to labour costs and the price-setting behaviour of firms in the period ahead

- Further increases in interest rates will be needed over the months ahead

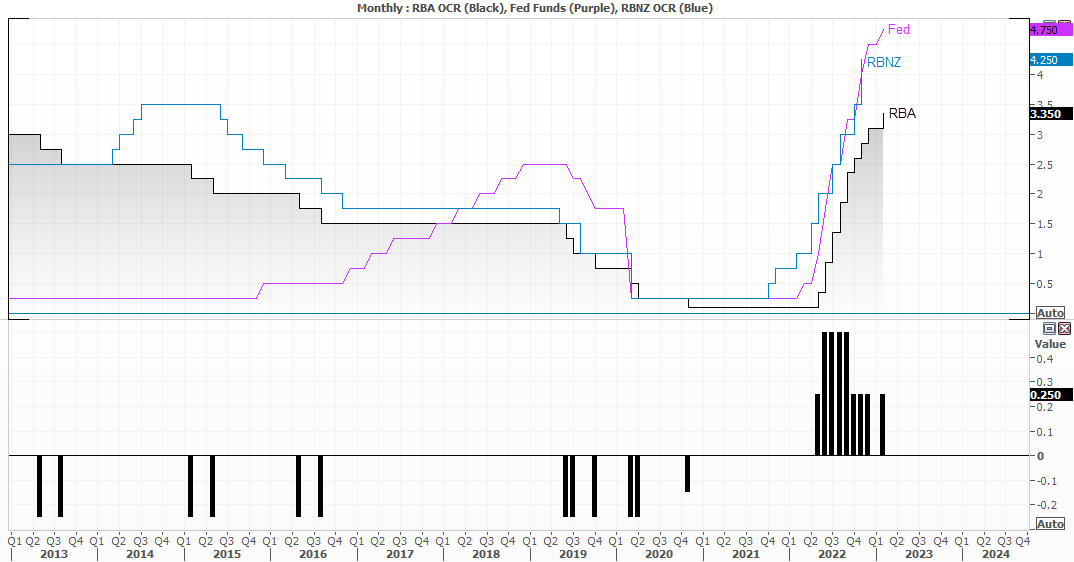

The RBA hiked the overnight cash rate by 25bp to 3.35% - its highest level since September 2012 – and warned of further increases in the months ahead. The two key words here are ‘increases’ and ‘months’, as it implies more than one hike over the coming months. And with rates at 3.35% it means the market pricing and consensus among economists for a terminal rate of 3.6% is not correct.

Given that the employment situation remains robust (or tight, as they say), inflation is higher than they expected and ‘strong domestic demand is adding to inflationary pressures’, we have several green lights for a hike in March and perhaps in May. Perhaps we’re closer to the elusive pause they teased us with last year, but I see no immediate threat of one in that statement.

And whilst the RBA expect CPI to decline as global factors and growth in domestic demands slows, what is going to happen if they do not slow quickly enough? Yep, more hikes. For now, a March hike seems like a done deal and I live in hope they hint at a pause, but I will not hang my hat on that given the data overall and strong levels of inflation.

The RBA’s quarterly SOMP is due to drop on Friday

The focus now shifts to Friday’s quarterly SOMP (Statement on Monetary Policy) which includes their revised forecasts.

The past three reports have seen growth forecasts decelerate and inflation upwardly revised. Given the new monthly annual CPI read rose to 8.1% y/y, and trimmed mean and median inflation beat expectations, there’s a decent chance we’ll see CPI revised higher once more – which in itself could signal another rate hike or two. Wage growth has also been revised higher over the past three reports and could be taken as another hawkish cue should it be revised higher for a fourth.

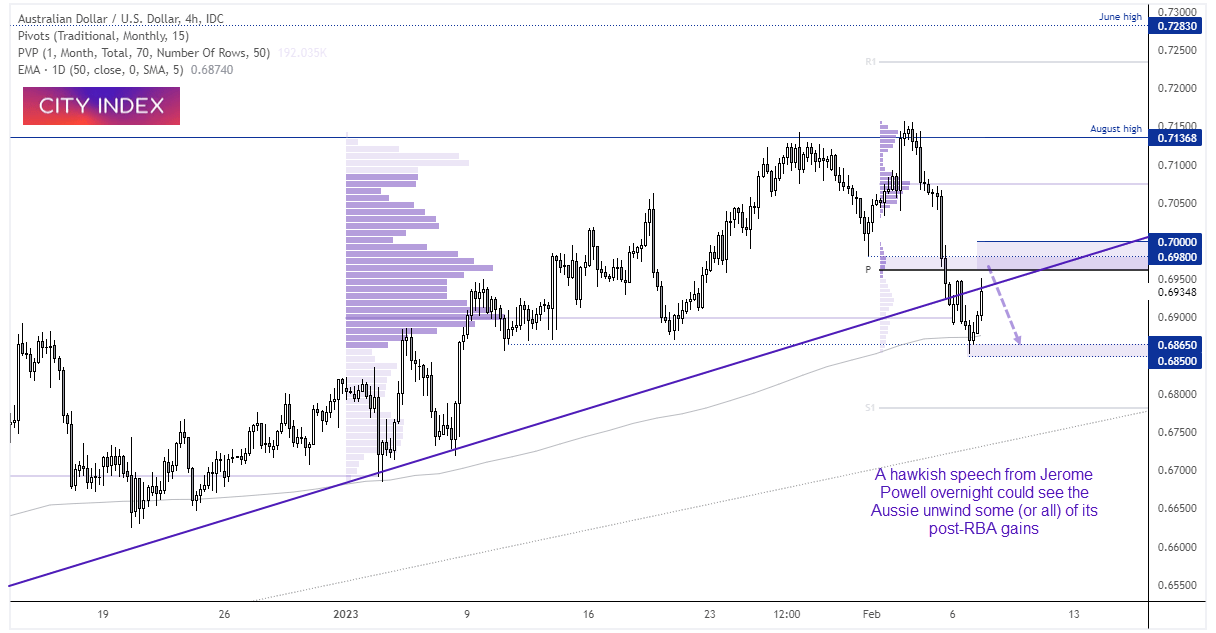

AUD/USD 1-hour chart:

The Aussie bounce around 1% after the rate decision, but it is debatable as to whether it can retain its strength if Jerome Powell delivers a hawkish message overnight. The Fed’s rate remains above the RBA’s, with a higher expected terminal rate.

AUD/USD found support around the 50-day EMA and has since spiked higher, but bears may want to seek evidence of weakness around 0.6900 as it houses the monthly pivot point and broken trendline. Of course, should Powell fail to deliver the hawkish message, then it leaves AUD (and other FX majors) more wriggle room to unwind some of their post-NFP losses.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM