January 31, 2020 4:52 PM

Week Ahead: Coronavirus Continues to Remain Market Focus

Market participants began the week wondering whether China would be able to contain the Coronavirus or if it would spread across the country and to other parts of the world. Markets quickly discovered the answer, and it wasn’t good for risk. For the most part, the FOMC was a non-event. However, the BOE did cause some excitement by leaving rates unchanged. Expectations were a 50-50 chance of a rate cut. As a result, GBP/USD has gone bid from near 1.3000 at the time of the announcement to 1.3200 at today’s close. Earnings were stellar this week for many of the top tech companies such as Apple, Tesla, Microsoft and Amazon.

As of Friday morning, China’s National Health Commission said the total number of confirmed Coronavirus cases was 9,692. That figure does not include cases outside of China and is surely to increase throughout the weekend. Reports suggest that the virus has spread to 25 countries. China has extended its Lunar New Year until Monday and many companies in China are encouraging their employees to work from home next week. In addition, some multinational companies have temporarily closed, and airlines have suspended flights to and from China. This trend is likely to continue until the rate of new cases begins to fall.

This week also brings the beginning of the primary voting season for the US Presidential Election on November 3rd. On Monday, the we get the Iowa caucuses. Current polling shows Joe Biden and Bernie Sanders in a close race for the Democratic delegates.

The US Senate continues its debate next week regarding the Impeachment of President Trump. So far, the process has had no effect on the markets. However, if that changes and markets feel there is a chance he may be impeached, risk off may ensue.

Earnings reports continue through next week with highlights including GOOG, F, DIS, BIDU, and UBER.

In addition, economic data will focus on Manufacturing PMIs, the RBA Interest Rate Decision, and Canadian and US employment data. Expected economic data for next week is as follows:

Monday

- China Caixin Manufacturing PMI

- Global Markit Manufacturing PMI

- US ISM Manufacturing PMI

- ECB’s Lagarde speech

Tuesday

- RBA Interest Rate Decision

Wednesday

- New Zealand Employment Change

- China Caixin Services and Composite PMI

- Global Services and Composite PMI

- RBA’s Lowe Speech

- Euro Area Retail Sales

- ECB’s Lagarde Speech

- Canada Trade Balance

- US Trade Balance

- US ADP Employment Change

- US ISM Non-Manufacturing PMI

- Crude Oil Inventories

Thursday

- Australia Trade Balance

- ECB’s Lagarde Speech

- ECB Economic Bulletin

Friday

- RBA’s Lowe Speech

- RBA Statement on Monetary Policy

- China Trade Balance

- Germany Trade Balance

- Canada Employment Change

- US Non-Farm Payrolls

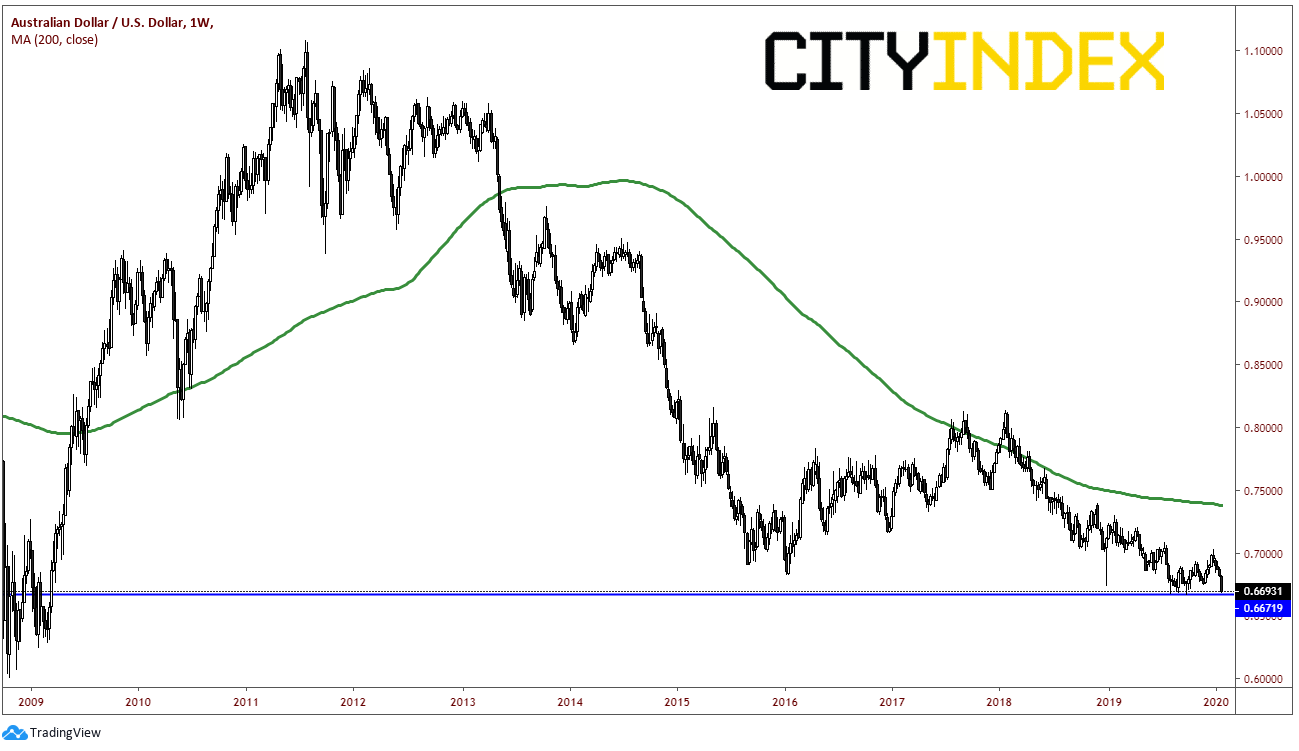

Chart to Watch: AUD/USD Weekly

Source: Tradingview, City Index

The AUD/USD has been trading lower since 2011, when it put in a high near 1.1080. The pair made a low in 2016 near .6850 and bounced to near .8125. However, in late summer of 2019, AUD/USD took out the 2016 lows and traded down to .6670 before bouncing up to near .7000. The pair is now threatening to take out the summer lows near .6670. A series of lower lows and lower highs is a downward trend! The next major level of support is near .6550, which is horizontal support from 2009. Resistance on the weekly chart is up at .7000.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM