- US Dollar Analysis: Dollar Index testing key support as focus turns to PPI inflation after a hot CPI earlier this week

- US dollar was hurt by weak retail sales on Thursday, but rising import costs is inflationary

- Week ahead features global PMIs among a handful of other macro data

Welcome to another edition of Forex Friday, a weekly report in which we highlight selected currency themes. In this week’s report, we will discuss the US dollar, upcoming data releases from the US next week, and look ahead to next week.

US Dollar Analysis: Dollar mixed ahead of key data

The US dollar was little-changed by mid-morning European session, ahead of the release of important PPI inflation data later on, and a long-weekend for North American investors with markets closed on Monday in observance of Presidents’ Day. Gains in the likes of the USD/JPY and USD/CHF were offset by a slightly firmer EUR/USD. The week ahead features a lighter macro calendar, which could see the dollar trade sideways but potentially maintain its relative strength.

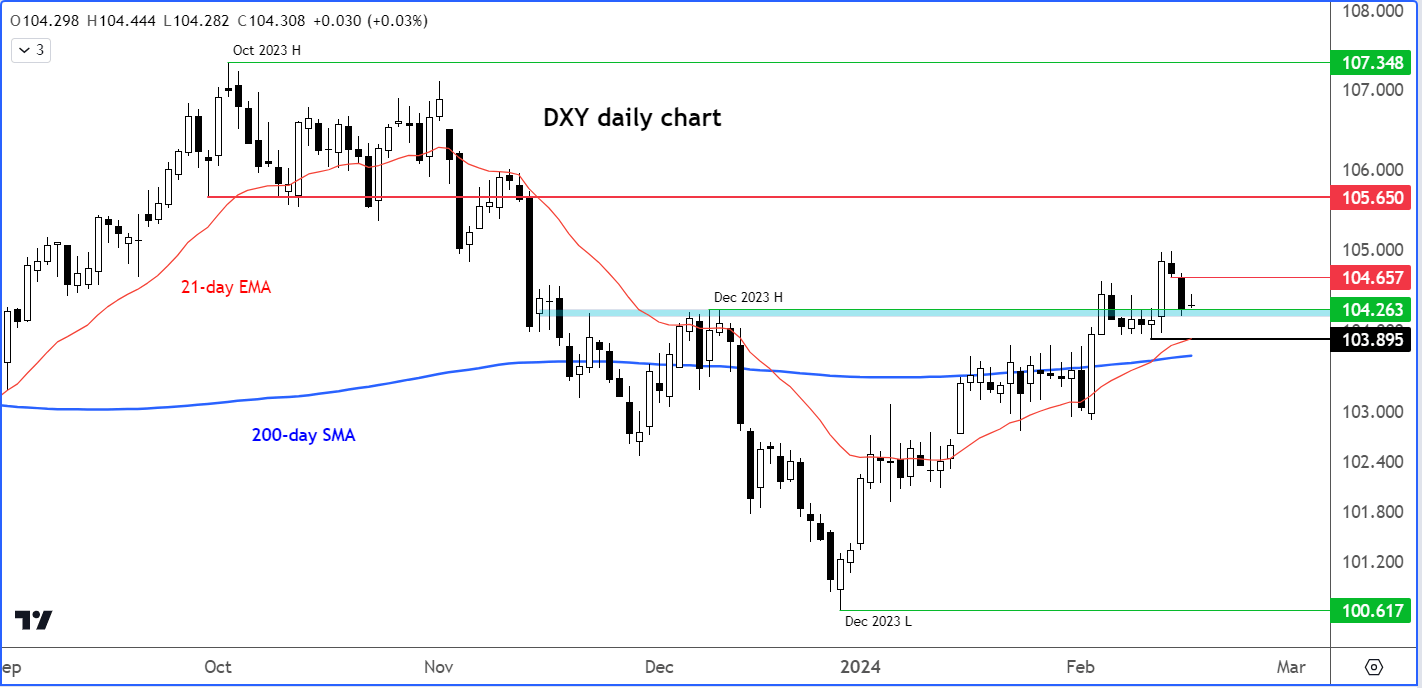

Before discussing today’s upcoming PPI data release in greater detail and look ahead to next week, let’s have a quick look at the Dollar Index’s chart to remind ourselves about the greenback’s general direction.

US Dollar Analysis: Dollar Index testing key support

Source: TradingView.com

Ahead of PPI data, the dollar index has now reached a critical support zone ranging around 104.26 to 104.00 area. Earlier this week, the upper limit served as resistance, before giving way on the back of the hot inflation report. This level also aligns with December's high. To sustain its bullish momentum, the DXY must maintain its position above this pivotal range. Any failure to do so would indicate a bearish outlook, especially given the robust inflation data released on Tuesday. Personally, I consider 103.90, the week's low, as the decisive level. A breach below this point would invalidate the short-term bullish technical outlook by establishing a lower low.

Assuming that the abovementioned support area remains intact, the Dollar Index could potentially ascend to 104.65, the low from Wednesday. Subsequent bullish targets include 105.00, above this week’s high, followed by 105.65 thereafter, an area which has acted as support previously.

Focus turns to PPI inflation

The producer price inflation report, coupled with consumer inflation expectations from the University of Michigan, will provide us further insights into the inflation picture of the US. The narrative of steady disinflation in recent months has helped to fuel a major rally in stocks, while keeping the dollar’s gains in check. Bizarrely, traders have consistently increased their bets on Fed rate cuts despite data remaining strong. However, if we witness an unexpected increase in PPI inflation, this will likely strengthen the argument for the Fed to delay rate cuts, potentially leading to higher yields and a stronger dollar.

PPI is seen rising by 0.1% month-over-month on both the headline and core basis. On a year-over-year basis, PPI is expected to print 0.6%, down from 1.0% previously, while core PPI is expected to come in at 1.6% vs. 1.8% last.

Meanwhile, the Michigan Consumer Sentiment report is expected to show a slight improvement to 80.0 from 79.0 previously but watch out if Inflation Expectations will show any notable change from 2.9% that was reported last time.

US Dollar analysis: Rising import costs is inflationary

Indications of persistent inflation are widespread. Last month’s sharp 0.8% m/m increase in import costs, as we found on Thursday, was largely attributed to rising petroleum expenses. Although this marked the largest surge since March 2022, a revised 0.7% decrease from zero in the previous month suggests the data might not be as concerning as the headline implies. Nevertheless, the unexpected rise was notable. This development follows closely after CPI data revealed that price pressures eased less than anticipated last month. With inflationary pressures slow to head lower, yields may remain elevated for an extended period, exerting pressure on lower-yielding currencies such as the yen and franc.

Retail sales hurt US dollar

The US dollar was hit by weak retail sales data on Thursday, which further ate into the CPI-related gains made on Tuesday. However, it's premature to discuss the dollar's peak, as a rebound is probable due to its long-term bullish trend, recent strong economic data from other sectors, and a hawkish Federal Reserve. Retail sales' softness may be an anomaly after consistently exceeding expectations for the past six months. Additionally, January saw the largest increase in import costs in nearly two years, potentially halting the disinflation process, which may prompt a cautious stance from the Fed following a hot inflation report. Consequently, the likes of the USD/JPY could surpass 150.00 more meaningfully and break its two-year resistance near 152.00, while the EUR/USD could head back towards 1.0700 now that it has staged a decent comeback to trade near resistance around 1.0780 to 1.0800 area. Despite slight recent weakness for the dollar, the hot CPI data suggests support for the dollar is there on any dips, amid diminishing talk of an early rate cut in March and uncertainties surrounding a May cut. Today’s PPI report could provide further insights into the inflation picture in the US.

Thursday’s release of jobless claims exceeded expectations, as did the manufacturing indices of Philadelphia and New York. However, softer industrial production and retail sales resulted in a decline in the dollar, a move that, as mentioned earlier, is unlikely to be sustained. Headline retail sales experienced a 0.8% decrease, while core sales dropped by 0.6%, both falling short of expectations. Industrial output also declined by 0.1% month-on-month.

US Dollar analysis video

Looking ahead to next week

With US markets closed on Monday in observance of Presidents’ Day, and most of the major data releases published in preceding weeks, the week ahead will feature not so significant macro highlights, apart from a handful discussed below.

Canadian CPI

Tuesday, February 20

In December, Canada's annual inflation rose to 3.4% from 3.1%, meeting expectations. This aligns with the Bank of Canada's projection of sustained elevated inflation around 3.5% for a lengthy period, potentially keeping rate cuts off the table for a long time. The increase was driven by higher gasoline costs, leading to rebounds in transportation and shelter prices, including rents and mortgage rates. Passenger vehicle prices also rose. With US inflation falling less than expected, will we also see a positive surprise for Canada’s CPI?

FOMC minutes

Wednesday, February 21

In January, the Fed kept rates steady at 5.25%-5.5%. Powell and his FOMC colleagues emphasised a reluctance to lower rates until confident about reaching 2% inflation sustainably. The Fed chair hinted at possible rate reductions later in the year but expressed scepticism about a March cut. The Fed omitted further rate hike references, noting improved risk balance but remained prepared to adjust policy if necessary due to persistently high inflation. Let’s see if the meeting minutes will convey any notable surprises that we don’t already know about.

Global PMIs

Thursday, February 22

Among the global PMIs to watch on Thursday will be those of Germany and the Eurozone, where the economy has been struggling, remaining well below the pace of growth observed in the US. This has not stopped the DAX to hit record highs, with nearly all mainland European indices doing rather well, but the EUR/USD has been stuck in a downward trajectory for a couple of months. But if we start to see improvement here, then the EUR/USD may start finding some much-needed support.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Forex Friday articles

July 19, 2024 01:00 PM

July 5, 2024 04:26 PM

June 21, 2024 12:02 PM

May 31, 2024 11:00 AM