Asian Indices:

- Australia's ASX 200 index fell by -90.2 points (-1.25%) and currently trades at 7,119.10

- Japan's Nikkei 225 index has fallen by 448.71 points (-1.43%) and currently trades at 30,879.45

- Hong Kong's Hang Seng index has fallen by -417.64 points (-2.25%) and currently trades at 18,178.14

- China's A50 Index has fallen by -208.09 points (-1.66%) and currently trades at 12,341.47

UK and Europe:

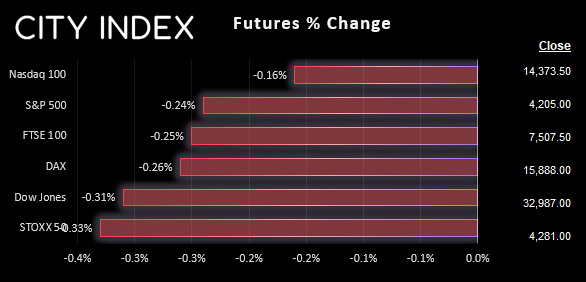

- UK's FTSE 100 futures are currently down -19 points (-0.25%), the cash market is currently estimated to open at 7,503.07

- Euro STOXX 50 futures are currently down -14 points (-0.33%), the cash market is currently estimated to open at 4,277.58

- Germany's DAX futures are currently down -41 points (-0.26%), the cash market is currently estimated to open at 15,867.91

US Futures:

- DJI futures are currently down -100 points (-0.3%)

- S&P 500 futures are currently down -10 points (-0.24%)

- Nasdaq 100 futures are currently down -23.25 points (-0.16%)

- China manufacturing PMI contracted at its fastest pace in six months, whilst services PMI fell to a 4-month low to further undermine China’s economic recovery

- This knocked sentiment in Asian to send equities lower (led by China), commodity currencies NZD and CAD become the weakest majors overnight whilst the USD, JPY and gold accepted safe-haven flows

- NZD/USD fell to a 6-month low, AUD/USD probed its YTD low, USD/CHF appears set break to a 7-week high and USD/CAD sits at a 4-day high ahead of the European open.

- AUD may well have been the weakest major, were it not for the fact that inflation rose to unexpected (and uncomfortably high) levels could force the RBA to hike at next week’s meeting

- Earlier in the session, RBA Governor warned that inflation risks were to the upside (it appears he was right) and that the central bank remains data dependent.

CPI and selling price expectations remain elevated for the Eurozone

We saw a small victory in Spanish CPI numbers yesterday which unexpectedly deflated -0.1% m/m (core was -0.2% m/m) and the annual measures were also beneath expectation. However, a business and consumer survey report for the Eurozone showed that inflationary pressures can’t come down quickly enough. Both consumer inflation and selling price expectations slowed, but not as fast as anticipated and remain elevated by historical standards. And if prices are expected to stay high, they probably will.

Events and themes in focus

- A host of inflation reports for parts of Europe are released today for Germany, France, Italy and Portugal which can help set the tone and expectations for Eurozone overall CPI tomorrow. In particular, state CPI reports for Germany 09:00 and 10:00 BST warrant a look, as it can give a lead for German nationwide (and therefore Eurozone) CPI numbers

- Three Fed members speak which could further sway opinions on whether the Fed will hike or pause in Jube, with Bowman hitting the wires at 13:50, Harker at 17:30 and Jefferson at 18:30

- The debt-ceiling bill is to be held to a vote in the House of Reps, and whilst it is expected to get the required votes to be passed on to the Senate, traders should be aware of any potential stumbling block would could weigh further an sentiment and send safe havens such as gold and the yen higher

- BOE member Mann speaks at 14:15

- SNB President Jordan speaks at 16:00

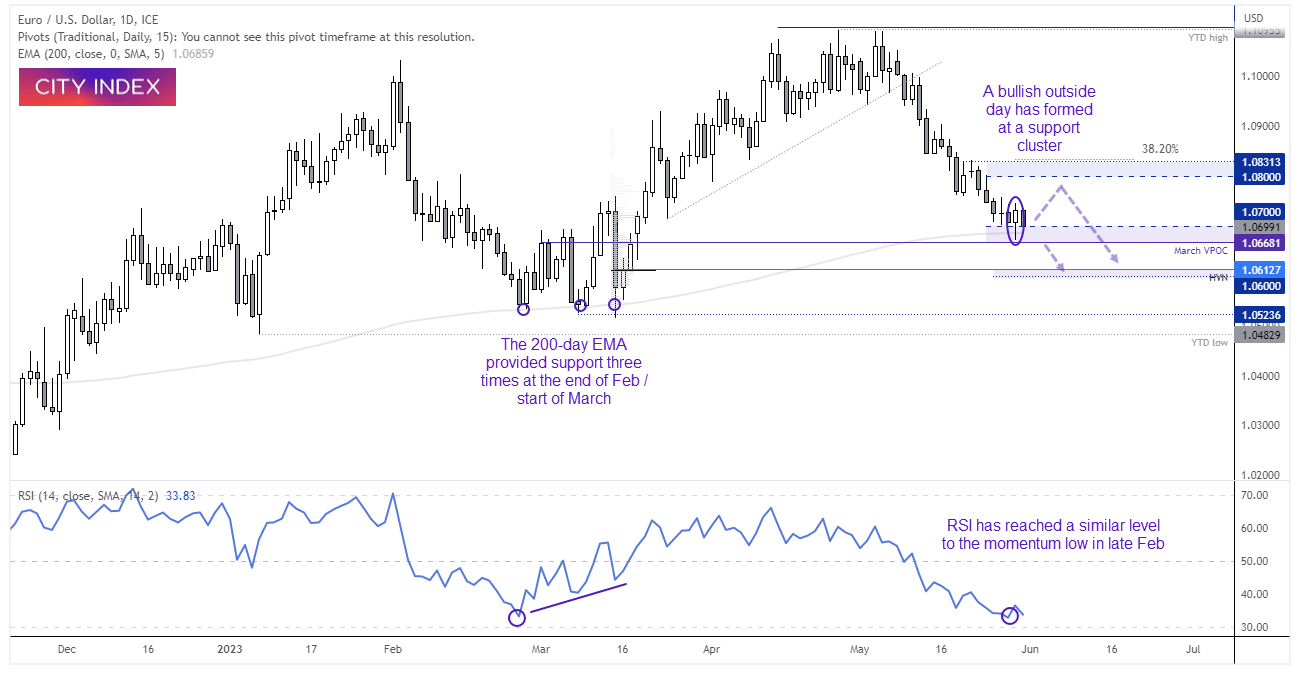

EUR/USD daily chart:

EUR/USD has fallen in a relatively straight line since the May high, but it has reached a zone of potential support which could potentially see the downtrend take a pause or even trigger a countertrend rally. The 200-day EMA provided support last week, and yester prices failed to hold beneath it before printing a bullish engulfing / outside day. The 200-dy EMA also provided support three times late February / early March.

Prices have also struggled to close below 1.0700 handle, the RSI (14) has reached a similar level as the momentum low which preceded the March rally. Furthermore, yesterday’s low held above the March VPOC (volume point of control) to suggest demand at those lows.

The longer EUR/USD struggles to break beneath the current cycle low, the grater the odds could be for mean reversion move higher. And if we are to see a combination of stronger euro inflation data and weak US employment figures (JOLTS), it could further support EUR/USD prices. However, a break below 1.0665 assumes bearish continuation towards the 1.0600 support zone.

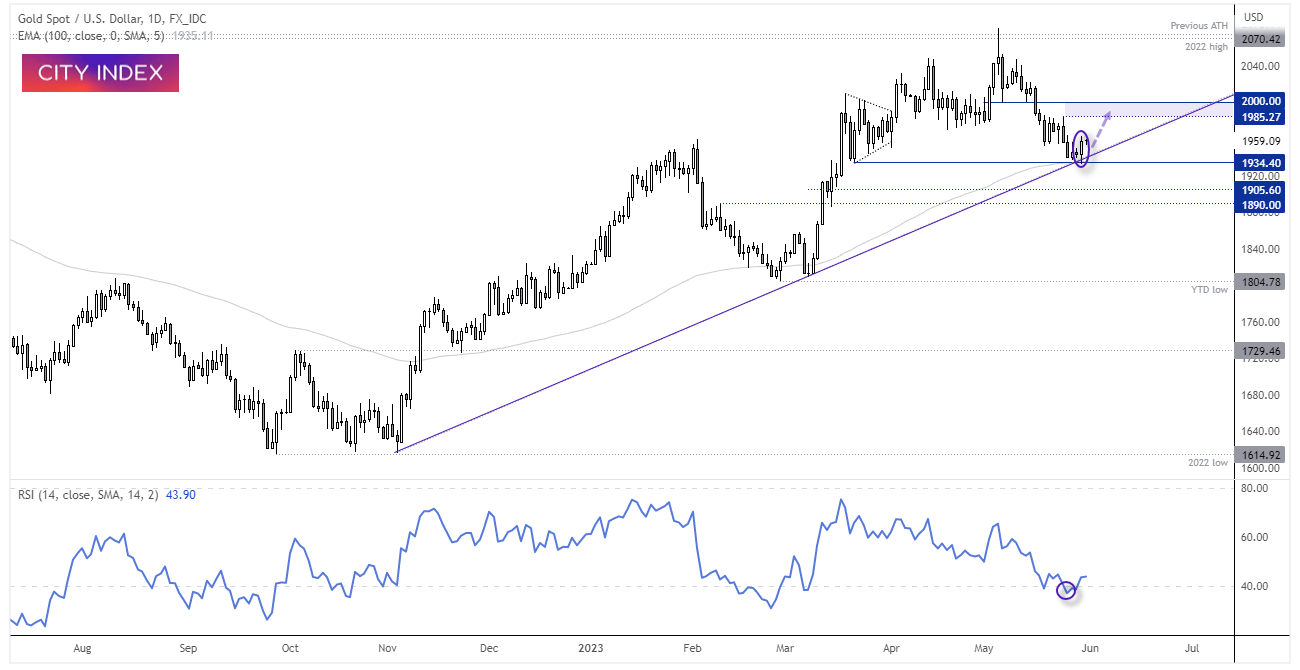

Gold daily chart

Gold prices have rebounded from a key area of support including the 1934.4 low, 00-day EMA and November trendline. Yesterday’s bullish engulfing / outside day shows strong demand from the cycle lows, and RSI has also dipped below 40 (which can be deemed ‘oversold’ during an uptrend).

Given weak PIM data denting sentiment, a move up towards the 1985 – 2000 resistance zone seems feasible. And it could get there fairly quickly if the debt-ceiling bill stalls at the Republican House today. Ultimately, the bias remains bullish above yesterday’s low on the daily chart, but bulls can also use 1950 for tighter risk management (and also not a potential bull flag on the 4-hour chart).

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM