Energy market volatility

Since the start of the Russian war, the market’s focus on the energy sector has been intense.

While it has now been over 6 months since the start of the war, the focus on markets such as oil and gas shows no signs of easing. Volatility in these markets remains elevated as the political and fundamental landscapes change.

Oil rebounds after OPEC cuts output

When Russia invaded Ukraine, the price of oil surged to $130 per barrel. As the West applied sanctions to Moscow, the price of oil remained elevated. More recently, oil prices have been falling, trading lower across the past three months from the $123 June high to current levels below $90 the barrel. The recently agreed G7 oil price cap could see prices fall lower. Meanwhile a surprise move by OPEC+ could keep prices well supported.

Economic slowdown

One of the main reasons for the decline in oil prices has been rising concerns of a global economic slowdown as central banks raise interest rates to tame inflation. As central banks across the globe hike rates, economies are slowing, which hurts the demand outlook for oil.

COVID lockdowns in China, the world’s largest oil importer, have added to the weaker demand outlook. Just last week, China locked down Chengdu, a city of 21.1 million inhabitants.

Iran

The US and Iran have been working hard toward an agreement to revive the Iran 2015 nuclear deal. Should a deal be reached, sanctions on Iran could be lifted, which would result in Iranian oil flooding back into the market. Iran has large quantities of floating oil reserves and could ramp up to around 1.3 million barrels per day of production, which would help reduce supply-side tightness.

While sanctions may not be lifted immediately, the market is forward-looking. Therefore, the prospect of Iranian oil returning to the market could be enough to lower prices.

OPEC+

OPEC+, the oil cartel group which includes Russia, has been conservative in its efforts to bring oil prices lower. The group stated that oil prices rose because of a political reason rather than an oil supply reason. Still, the group increased the output across July and August to 648k barrels a day, up from 340k. At today’s meeting, the group surprised the market by cutting production by 100k bpd from October despite supply remaining tight. It would appear that OPEC+ is keen to keep oil prices around $90 / $100 per barrel, even as global recession fears rise, and inflation stays elevated. Should OPEC+ stay on this path of tightening supply, oil prices could quickly rise again.

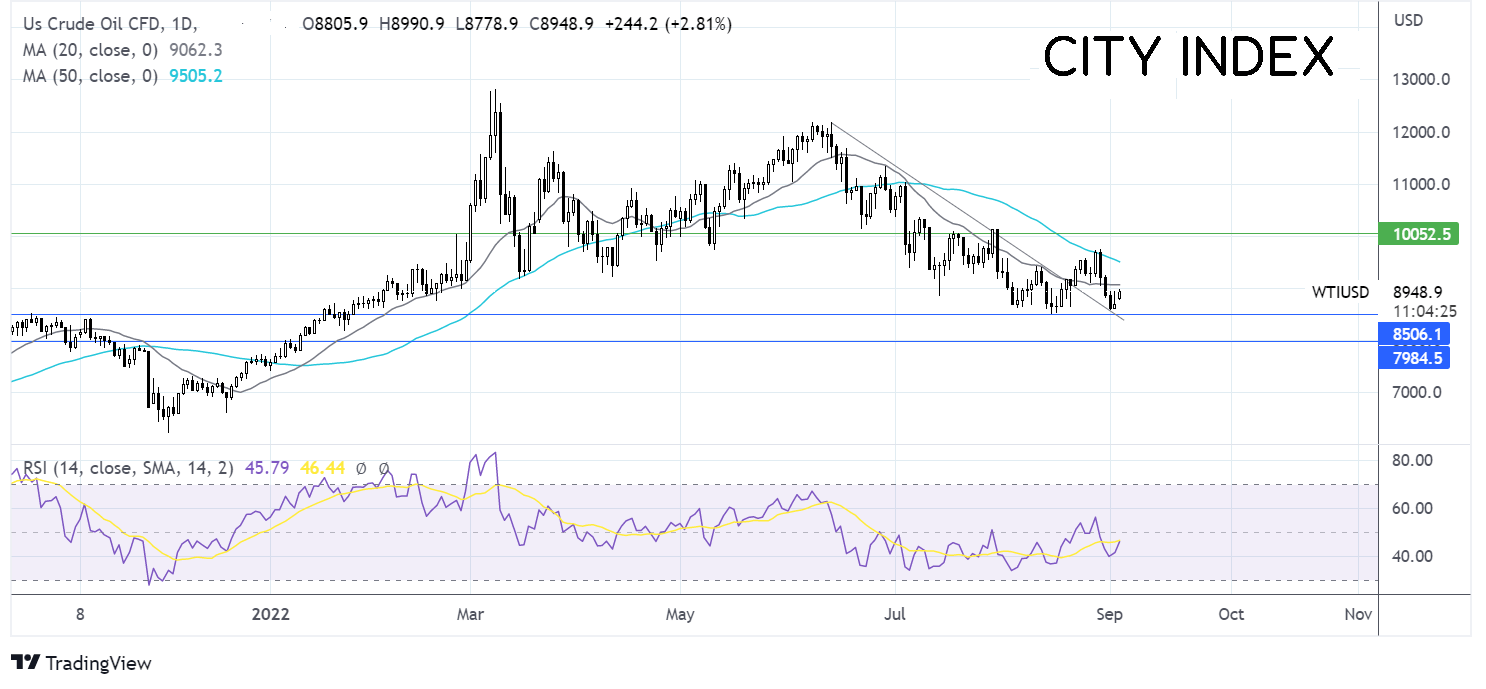

Where next for oil prices?

Oil found support on the multi-month falling trendline and is attempting to rebound higher. The price needs to rise above the 20 sma at 90.55 to expose the 50 sma at 95.00. A move above last week’s high of 97.00 would create a higher high and bring 100.00 psychological level into target. Meanwhile, sellers will look for a move below 85.00, the August low, and the falling trendline support to extend the bearish move towards 80.00, the round number.

Gas prices rise in the Lehman Brothers moment for the gas industry

Gas has been weaponized as part of the fallout from the Russian war. In retaliation for the West applying sanctions to Russia, Moscow slowed gas supply to Europe along the Nord Stream pipeline, reducing it to just 30% of pre-invasion levels. The tightening of supply saw both European and US gas prices head higher, reaching an all-time peak in August.

An announcement from Germany and the European Union that winter gas storage was filling up ahead of schedule resulted in gas prices falling last week.

European gas prices -Dutch TTF dropped 36% last week on optimism that the EU would manage to fill gas stores. US natural gas fell 5.7%

Nord Stream supplies stop

However, that optimism was short-lived. Russia announced that gas flow along the Nord Stream 1 pipeline had been halted indefinitely.

Following the announcement, gas prices in Europe have surged 30% but remain below the August record high. Meanwhile, the less volatile US gas prices have risen 2% and remain below August’s record highs, at least for now.

The crunch moment for gas prices is likely to come later in the year as temperatures drop. Should Europe experience a particularly cold winter, demand could quickly rise while supply remains weak.

Surging gas prices have a much broader implication, fuelling inflation and the cost of living crisis while slowing industry and economic growth.

European governments are announcing support packages to help energy-intensive firms and the most vulnerable.

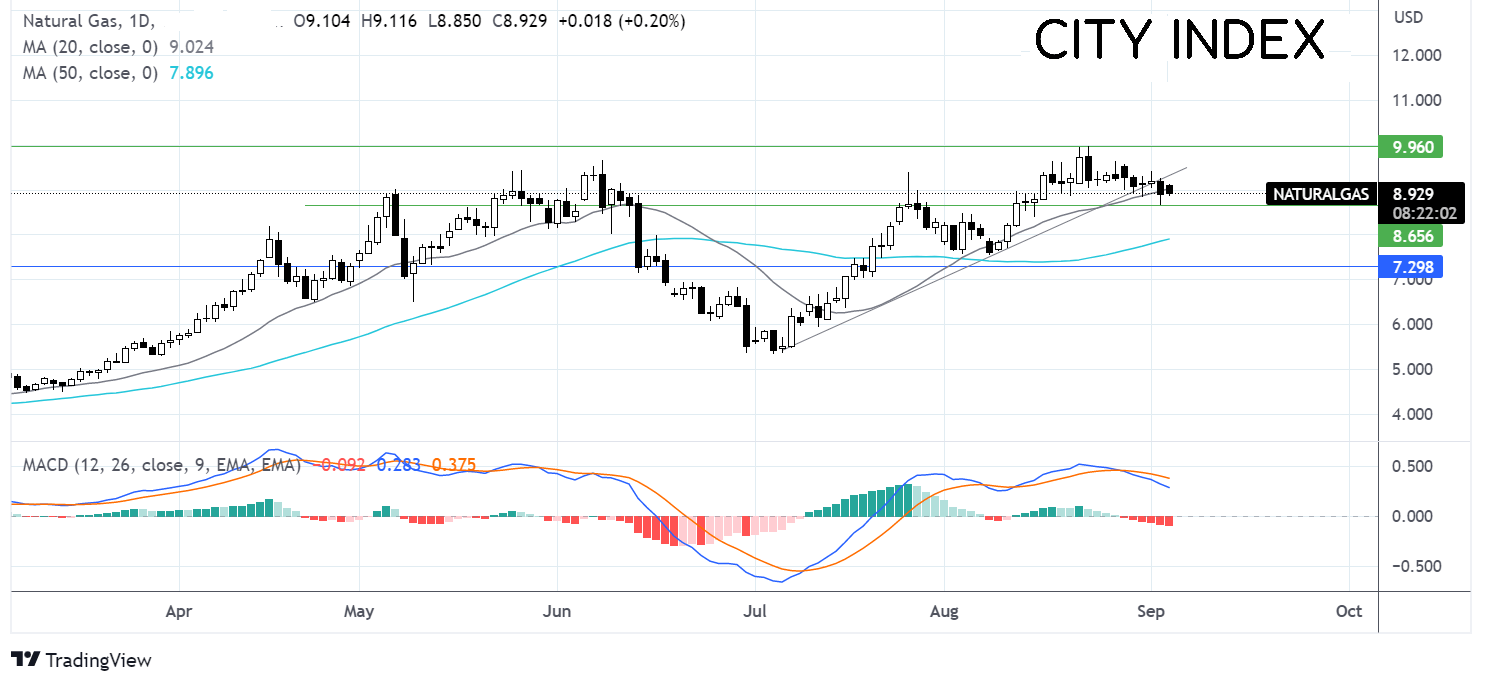

Where next for Natural Gas prices?

Natural gas ran into resistance at 9.969 and has been easing lower. The price has fallen below the multi-week rising trendline, which, combined with the bearish MACD, keeps sellers hopeful of further downside.

Bears need to break below 8.8900, the 20 sma, and 8.650, last week’s low, to extend the bearish trend and expose the 50 sma.

Should the bulls successfully defend the 20 sma, buyers could look to test the rising trendline resistance at 9.425. A rise above here brings the all-time high back into focus.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM