US futures

Dow futures +1% at 29578

S&P futures +1.3% at 3700

Nasdaq futures +1.5% at 11430

In Europe

FTSE +0.7% at 7043

Dax +0.8% at 12330

Learn more about trading indices

Market mood improves for now

US stocks are heading higher after steep losses over the past week, which saw the Dow Jones join the S&P500 and the Nasdaq in bear market territory.

Stocks have sold off sharply as the Fed has hiked interest rates aggressively and indicated that there are plenty more to come. Recession fears are growing, which is making stock picking that much harder. Whilst stocks are edging higher, this is more a pause in the market selloff rather than the start of anything more positive.

The fundamentals remain the same, and a recession is looking increasingly more likely. When the likes of Goldman Sachs downgrade global shares to underweight for over three months, we can expect the final quarter of the year to be a shocker.

Blackrock has adopted a similar stance, saying that the recession isn’t priced in yet. A soft landing is looking increasingly unlikely.

The sharp selloff in bonds historically points to a selloff in equities. With bond yields so high with ess relative risk, there appears little incentive to buy equities.

Looking ahead, US consumer confidence will be in focus. Expectations are for a tick higher in morale to 104 in September, after rising in August.

Corporate news:

Tesla rises pre-market as management push to deliver as many electric vehicles as possible before the of the third quarter.

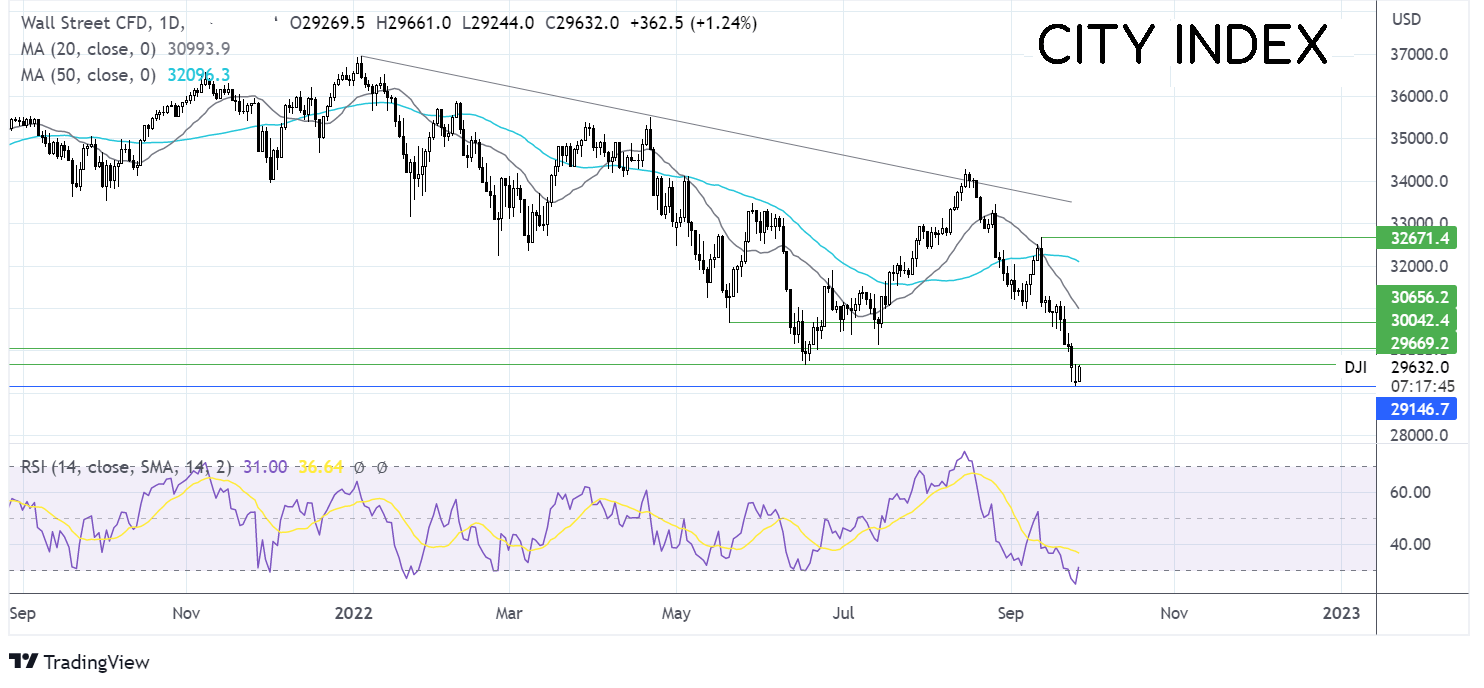

Where next for the Dow Jones?

The Dow Jones has found a floor at 12660, yesterday’s low, and is attempting to rise. The move higher is pulling the RSI out of oversold territory. Buyers would need to rise above resistance at 29600, the June low, to attract 30000 psychological level. It would take a move over 30660 to negate the near term selloff. Meanwhile, sellers will look for a move below 29150, the 2022 low to extend the bearish trend.

FX markets – USD eases, GBP rebounds

The USD is easing back from a 20-year high reached in the previous session as risk sentiment improves, increasing safe have outflows. Bulls are pausing for breath after the greenback rose to a fresh 20-year high yesterday.

EUR/USD is rising, boosted by the improved market mood. Data has been in short supply. The euro falls away from session highs after reports of sabotage on the Nord Stream pipeline, which sends European gas prices higher.

GBPUSD rises from an all-time low after the Treasury and the BoE attempted to calm the selloff. Both entities acknowledged the turmoil in the market, but neither was prepared to take action. As a result, the rally in the pound could be limited.

GBP/USD +1% at 1.08

EUR/USD +0.35% at 0.9640

Oil rebounds from 9-months.

Oil prices rose from a 9-month low, helped higher by the softening in the US dollar amid the hurricane in the Gulf of Mexico and as attention turns to next week’s OPEC+ meeting.

The supply side of the equation is in focus now, lending support to the price. BP and Chevron have shut production at offshore platforms in the Gulf of Mexico as Hurricane Ian approaches. Furthermore, the recent decline in the price of oil could mean that OPEC+ is more likely to intervene and cut production again.

API crude oil stockpiles are expected to rise by 300,000 barrels. The data is due later.

WTI crude trades +1.67% at $77.70

Brent trades +1.6% at $84.50

Learn more about trading oil here.

Looking ahead

15:00 US Consumer confidence

21:30 API oil stockpiles

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM