Stock market snapshot as of [5/11/2019 2:26 PM]

- Fresh positive geopolitical stimuli have appeared, turning the dial on risk appetite even higher. At the same time, chart and quantitative gauges suggesting risk assets are becoming ‘overbought’ are piling up too

- The S&P 500 is set to tag the latest in a string of recent records shortly after opening, as signs mount that Washington is signalling the limits of escalation in its trade confrontation with Beijing

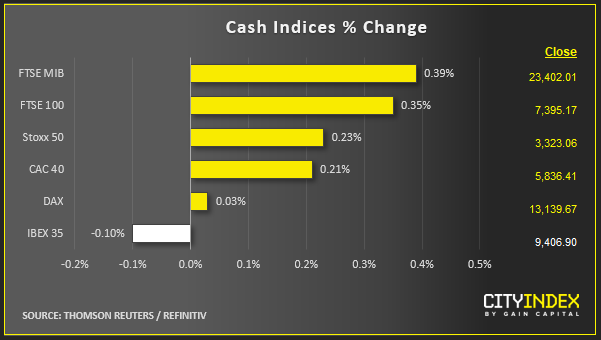

- Meanwhile, the largest European stock markets continued their tentative advances predicated on the same sentiment. Investors are waiting for some sort of official response to a Financial Times report stating that the Trump administration is actively considering whether to remove some tariffs it imposed on Chinese goods as a means sealing the so-called ‘phase-one’ aspect of a trade deal that is meant to pave the way for an eventual comprehensive accord

- The 10-year Treasury yield edged 3 basis points higher to 1.8265% by late morning in Europe, signifying a tailwind for the dollar whilst a falling yen confirms the switch to ‘risk-on’ remains in effect

- MSCI Asia Pacific index added 0.7% as Nikkei gained 1.8% after JGB futures extended losses in reaction to some marginal ‘yield control’ by the Bank of Japan. More importantly, Governor Haruhiko Kuroda suggested more super-long debt issuance was likely, a possible precursor to curve steepening; Japan’s benchmark yield jumps 4bps to -0.145%

- Further support came in the form of the PBOC’s first reduction of the cost of one-year funds to banks since 2016. The 5bp cut is a mild aid for liquidity, though a major one symbolically. China’s 10-year yield swung 4bps lower; Shanghai Composite was 1% higher. Onshore yuan strengthened for a sixth day and also caught the spotlight due to rising above the psychologically important and officially significant level of 7 yuan per dollar for the first time since 5th August. In key commodities Brent crude oil was firm at $62.76; Dalian iron rebounded 1.3% during the Asian session

- With vanilla sterling implied volatility now approaching September’s lows – down some 50% from highs seen during mid-October Parliamentary turmoil, Brexit and Britain’s election may not be the top focus for major investors at the moment. The Conservative’s poll lead vs. Labour is relatively steady at 38% to 25%, whilst the Lib Dems are unchanged at 16% and the Brexit Party’s standing rose 4 points to 11%

- Few game-changing trends have emerged with campaigning set to begin in earnest, though the Scottish National Party’s Nicola Sturgeon has hinted that it might be prepared to side with Labour in the event of an inconclusive vote

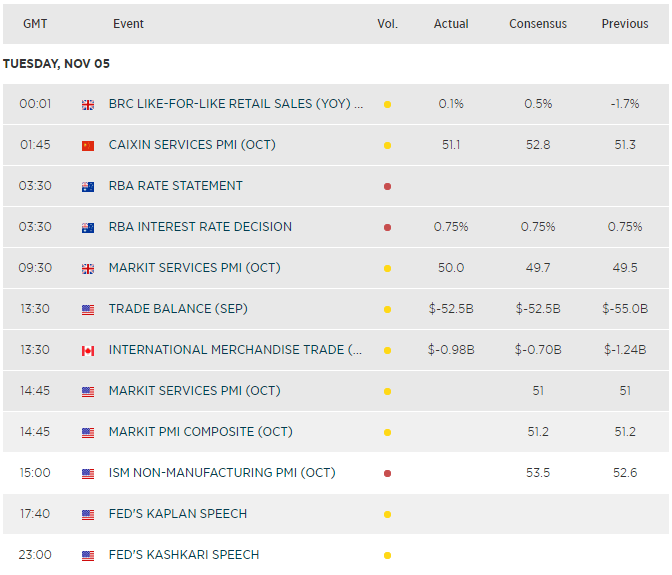

- A 40-odd pip rise by sterling against the dollar off lows had as much to do with weak, though not weaker than forecast business sentiment data out earlier. Markit’s service sector PMI printed at 50 in October vs. 49.7 expected and 49.5 in September. Downbeat details included a new business component that was the softest in 6 months and an all-sector orders index that fell at the fastest rate since 2009

Stocks/sectors on the move

- Energy shares were leading in Europe at latest check. Oil super majors rebound from the negative reactions to many of their earnings reports in recent sessions. Their results were clearly marked by declining oil prices as the trade conflict exacerbated pressures on global growth

- Mining and Financials were the other broad industrial segments in the green, though the remaining 9 STOXX super sectors were lower, denoting that current market advances are relatively narrow. Broader gains will be required if stocks are to extend their recent swing higher this week

- Higher cash incentives for electric vehicles in Germany appeared to benefit car parts manufacturers more than carmakers themselves. Whilst the country’s giant auto firms have ambitious programmes for electric vehicle production, these are at a relatively early stage, and the share of such vehicles purchased by consumers as a proportion of total production still reflect that

- Breadth was a little more evident in the first half hour of U.S. stock trading as technology shares joined in lifting Nasdaq indices and SPX 0.5%-0.6%. A utilities decline backs the perception that participants are less inclined for the moment to orbit generally safer assets

- Standout movers include: Xerox, +7% as Fujifilm said it will buy XRX’s stake out of their 60-year old JV. Adobe, +5% on a note from Citigroup lauding its digital media prospects. Shake Shack tumbles a messy 18% after cutting same-store sales guidance. Uber’s better than expected Q3 revenues and lower than forecast loss aren’t being credited. The stock slides 7% as investors focus on gross booking of $16.47bn, compared with $16.70bn expected, as the miss may imply that slowing overall growth. Chesapeake Energy a pre-market fall to as much as 14%. The group issued a ‘going concern warning’ after posting Q3 loss per share that was towards the weaker end of estimates

FX snapshot as of [5/11/2019 2:27 PM]

View our guide on how to interpret the FX Dashboard

FX markets

- The yuan extended gains into the U.S. session, even as the risks rise that something as simple as one tweet could dash them rose, as per numerous times in the recent past

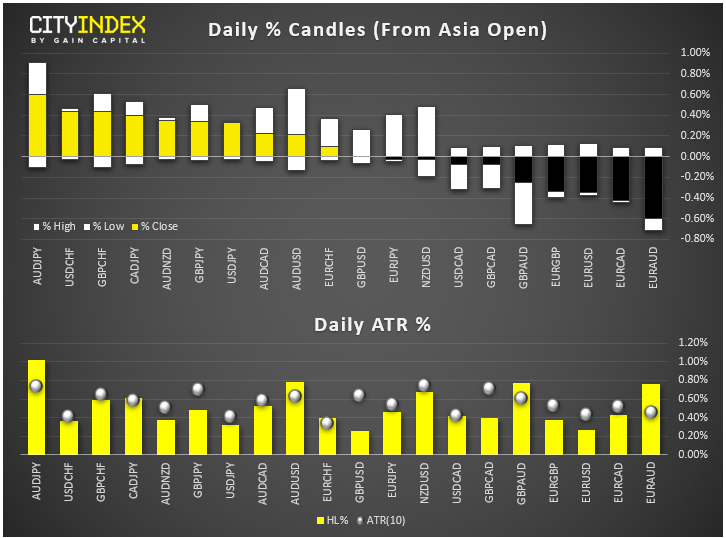

- FOREX.com senior technical analyst Fawad Razaqzada adds: “the U.S. dollar is doing well against havens franc, yen and gold, while falling against commodity dollars & yuan. Put simply, so far, it has been another risk-on session. Will the trend continue? S&P 500 has been up for multiple days in record highs, pushing oscillators to overbought levels”

- The Dollar Index also extended gains to stand around a quarter of a point up at 97.745 just now, though still down some 2%-plus from end-October’s around 18-month highs DXY reached on the back of haven flows

- A broad yen retreat also denotes participants continuing to relinquish aversive moves in favour of risk

- The Aussie dollar also catches a bid as yields rise following an RBA rate decision that appeared to put further distance between its policymakers and potential near-term loosening

Upcoming economic highlights

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Bonds articles

July 1, 2024 11:04 PM

May 30, 2024 06:11 AM

May 3, 2024 01:00 AM