Asian Indices:

- Australia's ASX 200 index fell by -45.6 points (-0.63%) and currently trades at 7,202.80

- Japan's Nikkei 225 index has fallen by -458.48 points (-1.65%) and currently trades at 27,363.64

- Hong Kong's Hang Seng index has fallen by -111.16 points (-0.46%) and currently trades at 23,992.99

UK and Europe:

- UK's FTSE 100 futures are currently down -45.5 points (-0.65%), the cash market is currently estimated to open at 7,031.60

- Euro STOXX 50 futures are currently down -34 points (-0.84%), the cash market is currently estimated to open at 4,031.43

- Germany's DAX futures are currently down -107 points (-0.7%), the cash market is currently estimated to open at 15,087.49

US Futures:

- DJI futures are currently up 311.75 points (0.92%)

- S&P 500 futures are currently down -81 points (-0.55%)

- Nasdaq 100 futures are currently down -19 points (-0.44%)

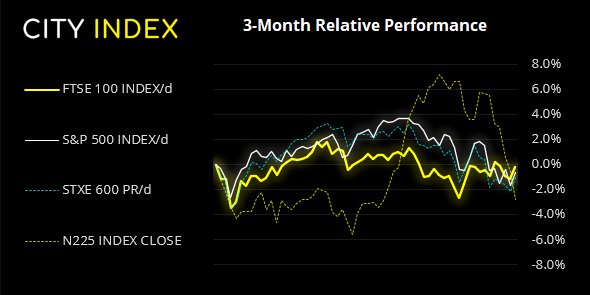

Asian equities (ex-China) turn lower

We didn’t see the rebound we had hoped for during Asian trade for equity markets overall. The ASX 200 stalled at yesterday’s high and quickly reversed and is not on track for a bearish outside day. Japan’s equity markets continued to slide and were some of the weakest of the session. Although China’s share markets remained buoyant with the CSI 300 the strongest of the session.

Rising oil prices remains a concern across the region, and a hike by RBNZ also signalled there could be other hikes (from other central banks) should inflation not actually be transitory at all. But there is also the general feeling that the fallout from Evergrande will sting overseas investors, whilst any intervention from Beijing will cushion the blow of onshore investors. (Well, it has happened before so it can happen again).

FTSE 350: Market Internals

FTSE 350: 4059.89 (0.94%) 05 October 2021

- 215 (61.25%) stocks advanced and 126 (35.90%) declined

- 8 stocks rose to a new 52-week high, 14 fell to new lows

- 57.26% of stocks closed above their 200-day average

- 41.88% of stocks closed above their 50-day average

- 9.12% of stocks closed above their 20-day average

Outperformers:

- + 11.1%-Greggs PLC(GRG.L)

- + 6.33%-Darktrace PLC(DARK.L)

- + 5.40%-Restaurant Group PLC(RTN.L)

Underperformers:

- ·-4.00%-Elementis PLC(ELM.L)

- ·-3.55%-Endeavour Mining PLC(EDV.L)

- ·-3.48%-Babcock International Group PLC(BAB.L)

Forex:

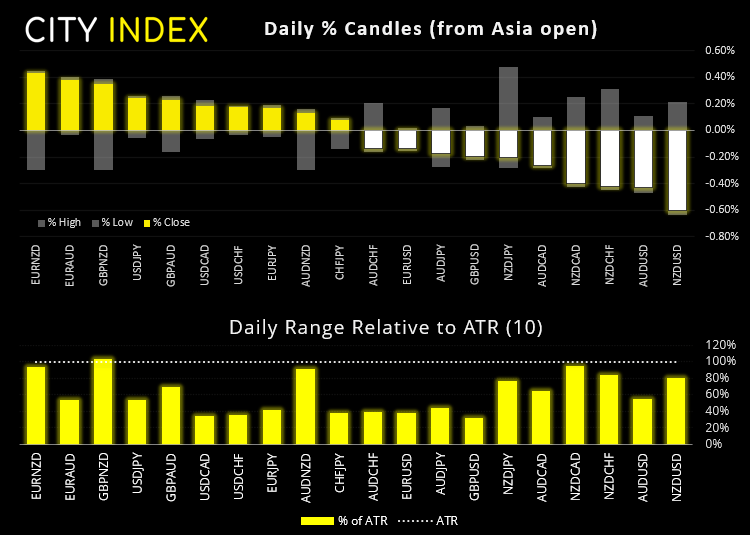

RBNZ hiked by 25 bps, a first for the central bank since 2014. Their outlook was positive for the medium-term which points to further hikes from here. Markets are currently pricing in another hike next month but (personally) do not see it as a given. In today’s statement, they said of their awareness of the impact the latest lockdowns had on many businesses. Moreover, their forecast rate from the August MPS (Monetary Policy Statement) is 0.6% by December, below the 0.75% expected by November by some. I’m not saying it will not happen, but we saw RBNZ hold off-from an ‘all-but-given’ hike the day prior to their September meeting. And these points likely help explain why NZD is weaker following the event. Basically, the situation is fluid.

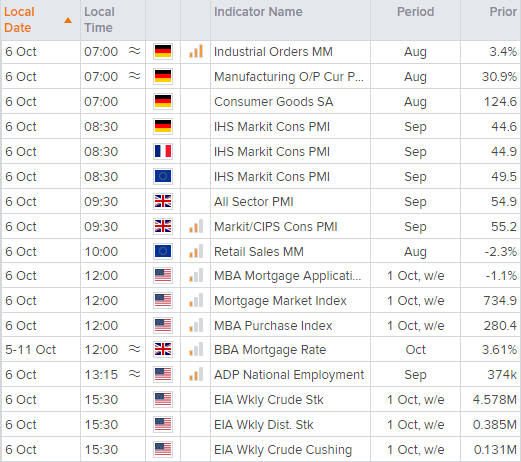

German industrial orders at 07:00 BST, construction PMI at 08:30 and UK PMI’s at 09:30 are the main economic data sets in today’s European session. Although the highlight of the day is likely to be September’s ADP employment set at 13:15. It will be taken as an early proxy for Friday’s highly anticipated NFP report, which itself is a proxy as to whether the Fed will taper at their next meeting or not. Should it come in weaker than expected we would expect the US dollar to take a knock and make our 112 target for USD/JPY seem a little further away.

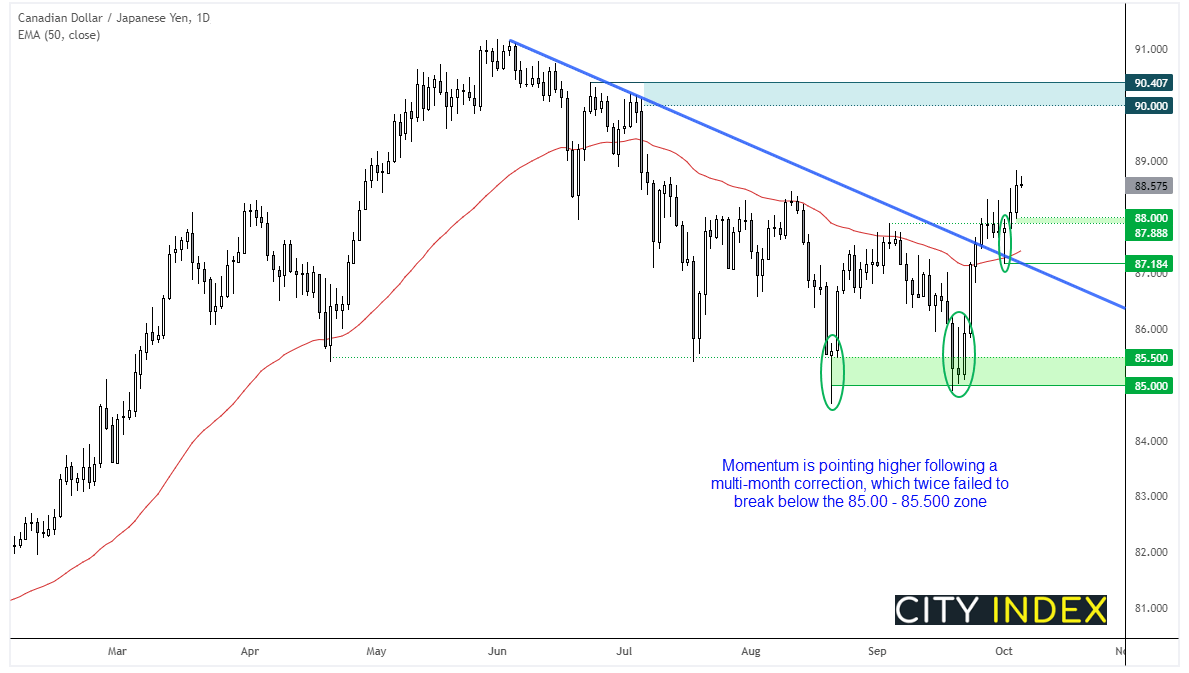

Should sentiment remain buoyant and oil prices continue to rally, CAD/JPY remains of interest for bullish setups. The daily chart shows it has broken above a retracement line on the daily chart, after twice failing to break below 85.00. A minor retracement last week confirmed the broken retracement line as support and momentum points higher. The daily trend remains bullish above 87.18 although we’d be keen to see any volatility dips towards 88.00 as part of a larger move north.

Commodities:

WTI is coiling up in a nice bull flag on the hourly chart, and momentum suggests traders want to take it to $80. But with it being such a round psychological number then it’s a likely area for traders to book profits and bearish momentum shows its face (even if only temporarily).

Silver is trying to turn lower after printing a small inside day / hanging man reversal candle. A break of 22.29 confirms a near-term reversal although $22 could provide support initially. Should prices continue to chop around ahead of NFP (plausible) then we’d consider bearish setups below $23.

Up Next (Times in BST)

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Forex articles

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 03:59 PM

July 25, 2024 04:37 AM