It has been a quiet-ish day in the markets, with many investors and traders sitting on their hands ahead of a very busy week of macro events next week. We have seen the earlier weakness in stock averages being bought after the US cash markets opened, with the dollar also softening across the board. Crude oil was unable to hold onto its earlier gains, after initially rising sharply on news Keystone oil pipeline was shut down following a leak. Will the major indices follow oil lower after a positive start in early US trade?

I wouldn’t be surprised if the markets were to give back their gains, after what has been a somewhat bearish last few days in the markets amid growing concerns over economic growth. In addition, there are so many event risks awaiting investors in the week ahead. Thus, investors may not be willing to buy every breakout, including this one.

Investors fear that volatile market conditions might return after the relative calm in the last couple of months. It is clear that the sharp central bank policy tightening will become less aggressive before rate hikes are paused altogether in the first half of next year. But that’s where the good news might end. Inflation may remain sticky, and the global economic slump is likely to worsen, thus holding back consumer spending. This could weigh on companies’ top and bottom lines, and excessive risk-taking by investors. Thus, European and US indices should remain under pressure, although China’s move away from Covid Zero policy may help keep the downside limited for the local markets.

In terms of the more immediate risks facing investors will be next week’s busy schedule of data and central bank meetings.

US CPI (Tuesday) is arguably going to be the most important macro data next week. US inflation has fallen to 7.7% from a peak of 9.1% in the summer, leading to speculation that the Fed is going to hike less aggressively moving forward, starting with a 50 basis point hike on Wednesday. CPI is expected to have eased for the fifth consecutive month to 7.6% in November.

A day after the CPI report, it will be the eagerly anticipated FOMC monetary policy meeting on Wednesday. After several 75 basis point rate hikes, the Fed has already hinted strongly to the market that it is going to hike by 50 basis points at this meeting. The key question will be about the pace of future rate hikes and the terminal interest rate. If the Fed hints at a 5% or higher terminal rate, then this could trigger a risk-off response in financial markets, and a rally for the dollar.

Central bank action is not going to end there, as we will have the likes of SNB, BoE and ECB all to look forward to Thursday of next week. You are spoilt for choice. It could well be the last hurrah for major market events before things start to wind down ahead of the Christmas holidays. They are all expected to hike their respective rates by 50 bps each.

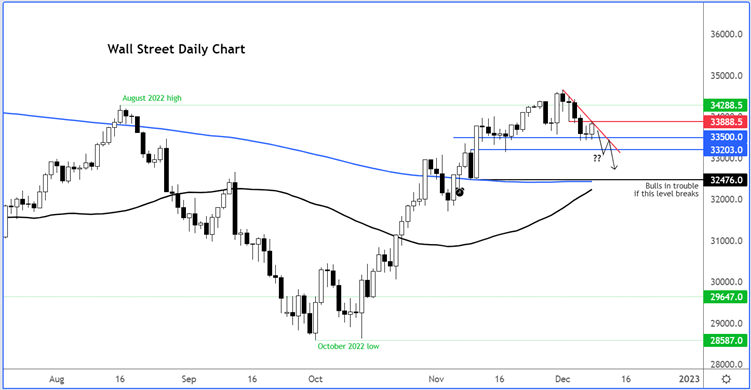

Ahead of all that, the Dow was testing a key short-term resistance level around 33850 at the time of writing. This is the short-term resistance trend that has been established over the past few sessions.

The Dow has been going lower in recent days after failing to hold above the August high. So far, the downside has been limited. But if the above macro concerns intensify as we think might be the case, then look out below.

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Indices articles

July 25, 2024 01:30 PM

July 25, 2024 01:01 AM

July 25, 2024 12:41 AM

July 24, 2024 07:26 PM