Global recessionary signals are continuing to pour in. Today’s macro data from around the world have been quite poor, especially the latest PMI data, underscoring the challenges central banks face at a time when inflation remains very high. With the global economy slowing, and central banks having to tighten their belts further, it is difficult to see how stock markets would thrive in this sort of environment, after this year’s mostly weakening asset prices.

Busiest week of company earnings

With this also being the busiest week for US tech earnings, be prepared to hear more about how the strong dollar and high inflation is hurting US sales abroad. As such, I very much doubt that the rebound in indices we saw on Friday will hold. At best, we could see only a modest further recovery in the event of a few earnings beats. But do remember that the bar is set quite low already. The devil will be in the detail. Any short-term spikes in stock prices as a result of a beat or two could get sold into, if the earnings are accompanied by warnings about sales.

Read my colleague Joshua Warner’s earnings preview for this week, HERE.

US PMIs plunge into contraction

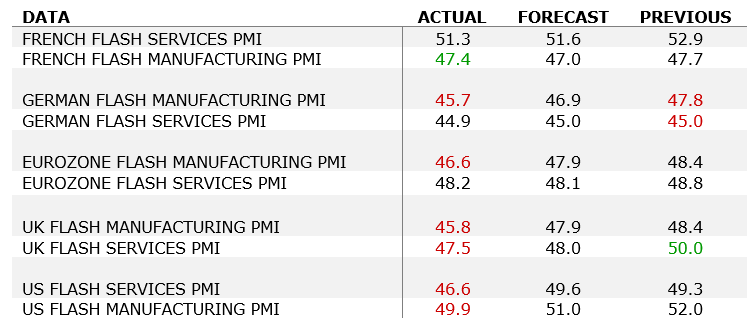

On a more macro level, the US economy has weathered the global stagflation storm slightly better than some of the other regions of the world, such as the Eurozone. But even here, cracks are starting to appear. The manufacturing PMI plunged into contraction in early October, while the services PMI also fell deeper below 50.0, as new orders were the weakest since Covid lockdowns.

It looks like the dollar strength is doing a lot of the damage. The report says that “total new orders were dampened by challenging economic conditions in key export destinations and dollar strength, as new export orders fell steeply."

What’s more, “firms’ optimism about the outlook meanwhile deteriorated markedly in October. The resulting degree of confidence was among the lowest in the survey history and the weakest for just over two years.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence commented: “The US economic downturn gathered significant momentum in October, while confidence in the outlook also deteriorated sharply. The decline was led by a downward lurch in services activity, fuelled by the rising cost of living and tightening financial conditions…. October saw a steep drop in demand for goods, meaning current output is only being maintained by firms eating into backlogs of previously placed orders. Clearly this is unsustainable absent of a revival in demand…The surveys therefore present a picture of the economy at increased risk of contracting in the fourth quarter at the same time that inflationary pressures remain stubbornly high.”

US not alone in producing poor PMI data…

Earlier in the day, the latest PMI data from the Eurozone and UK all remained in the contraction territory except France’s services industry. Here’s a summary of the PMI data:

Overnight we also had the Chinese retail sales data, which disappointed but GDP and industrial production were better than expected.

Busy week of central bank action

It is going to be a very busy week for central bank meetings with bank of Canada on Wednesday, European Central Bank on Thursday and Bank of Japan on Friday. Today we had PMI data out of Europe intensifying concerns over a recession.

Bank of Canada (Wednesday, October 26)

Although Canadian CPI eased for the third consecutive month in September, at 6.9% y/y it remains very high, why core CPI increased to 6% from 5.8% previously, beating expectations. Analysts are split about whether the BoE will hike by 50- or deliver another 75-basis point increase. Governor Macklem remains quite hawkish.

European Central Bank (Thursday, October 27)

The European Central Bank hiked the benchmark deposit rate to 0.75% from zero at its last policy setting, which pushed interest rates to their highest since 2011. Inflation has since continued to rise. Annual CPI accelerated to 9.9% in September from 9.1% previously, rather than 10%. That means prepare for more hikes. Another 75-basis point increase is expected.

Bank of Japan (Friday, October 28)

The USD/JPY went well above 150.00, which some had predicted might be the line in the sand for the Japanese authorities, before another suspected intervention sent rates sharply lower Friday. the USD/JPY has since bounced back. In recent times, the yen has sold off so much that it has seen the Japanese government try to intervene by selling its huge dollar reserves to help shore up the currency. But its efforts have been futile. Will the government now force BoJ’s hand to change it stance? If BoJ maintains status quo, expect further yen depreciation.

What does it all mean when it comes to trading?

So, the bigger moves are likely to occur in the second half of the week. As such, we will go easy with our trade ideas at the start of the week. Patience is key in this business. Knowing when to trade is great but knowing when not to is even better. Capital perseveration is the number one priory. Defence is the best form of attack.

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM