Asian Indices:

- Australia's ASX 200 index fell by -20.1 points (-0.28%) and currently trades at 7,235.90

- Japan's Nikkei 225 index has risen by 210.82 points (0.76%) and currently trades at 28,034.53

- Hong Kong's Hang Seng index has risen by 364 points (1.55%) and currently trades at 23,839.26

- China's A50 Index has risen by 19.55 points (0.13%) and currently trades at 15,379.16

UK and Europe:

- UK's FTSE 100 futures are currently up 41 points (0.58%), the cash market is currently estimated to open at 7,100.45

- Euro STOXX 50 futures are currently up 23.5 points (0.58%), the cash market is currently estimated to open at 4,086.56

- Germany's DAX futures are currently up 93 points (0.61%), the cash market is currently estimated to open at 15,193.13

US Futures:

- DJI futures are currently down -652.22 points (-1.86%)

- S&P 500 futures are currently up 213.5 points (1.32%)

- Nasdaq 100 futures are currently up 37.5 points (0.82%)

Asian indices were higher overnight as traders repositioned following recent bearish moves and likely became fatigued of Covid headlines. The KOSPI 200 was a top performer following strong trade data, with export growth in South Korea rising 32.1% y/y and import growth up 43.6% to show strong demand locally and domestically. The Hang Seng also managed to recoup yesterday’s losses and trade back above the October low. Futures markets have also opened higher, seemingly ready to start the new day a fresh.

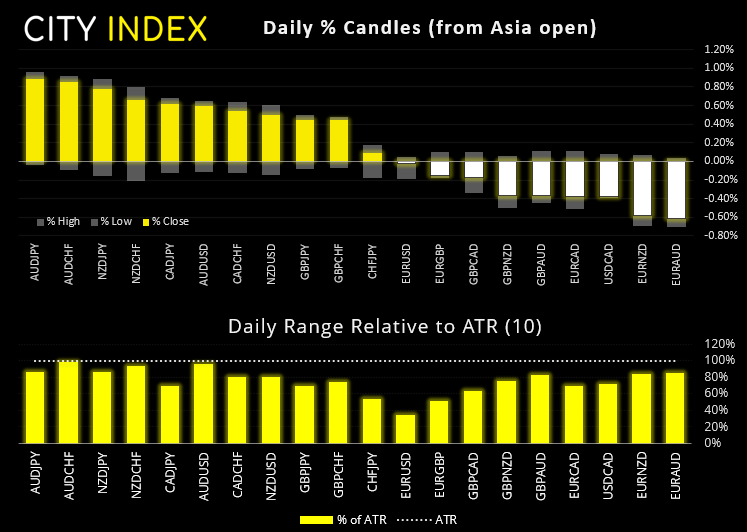

Commodity currencies lead the way

AUD and NZD are up around 0.5%, with the Kiwi being supported by RBNZ comments that Omicron won’t change the banks outlook. CAD is up around 0.3%, bolstered by higher oil prices ahead of today’s OPEC meeting, whilst safe haven currencies JPY and CHF are softer.

The Australian economy contracted in Q3

It would have been really quite amazing if they had not, considering the lockdowns in New South Wales and Victoria, but at -1.9% q/q it beats expectations for a -2.7% slump. Manufacturing PMI data released earlier showed the sector expanded at 54.8% (up from 50.4) according to AiG, whilst the Markit Economics came in higher at 59.2 (up from 58.5).

Given the ‘not bad as feared’ GDP report, and cautious lift in sentiment we see the potential for a countertrend move on AUD. We do not expect this to be popular, given the strength of the bearish move, yet we would also argue that very few inflection points are popular to begin with. Besides, Yesterday’s volatile bearish day failed to hold beneath the August low which hinted at a beartrap. Furthermore, prices have now reached yesterday’s high and the weekly pivot point – so should we see a clear break of these levels it could trigger larger bearish stops and potentially send it higher, at least over the near-term.

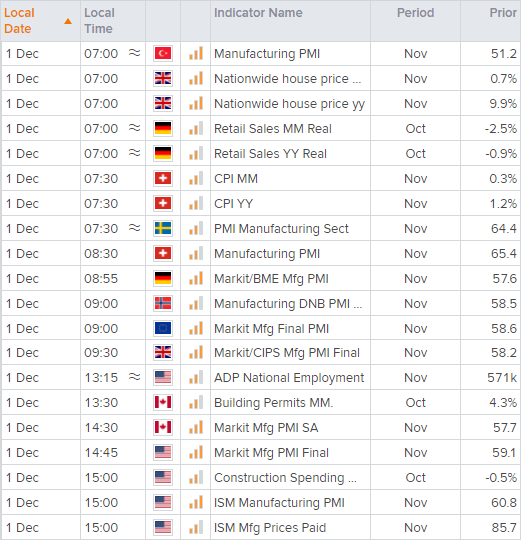

China’s manufacturing contracts, according to Markit Economics

Earlier this week we noted that China’s ‘official’ PMI had crawled into expansion territory, so was not setting the world alight. Today Markit Economics, an independent research house, released their own manufacturing PMI which revealed the sector had in fact slipped back into contraction. Subdued demand with high prices and lower employment weighed on the headline figure, which does not bode well for growth in H1.

Prices paid and backlogs in focus for ISM

The ISM manufacturing report is scheduled today for the US. And, like most PMI’s at the moment, the key measures to watch are prices and backlog of orders to ascertain inflationary forces and bottlenecks. Last month we saw backlog of orders remain elevated yet slow slightly (good) yet prices were rising at a faster rate (bad). We noted in this week’s China PMI report that raw material prices had dropped and that would be a welcome surprise for the Fed if repeated, especially having only jus conceded that inflationary is not transitory. As for the bigger picture, the headline PMI topped in March and is just another reason traders expect growth to diminish whilst prices remain high.

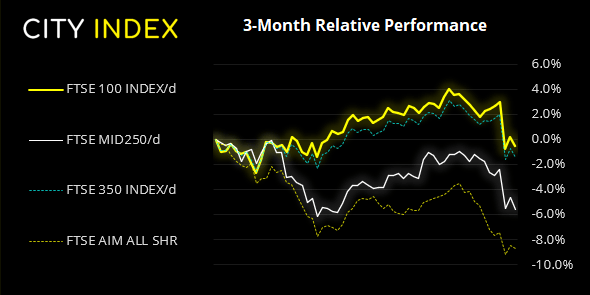

FTSE 350: Market Internals

FTSE 350: 4044.89 (-0.71%) 30 December 2021

- 58 (16.52%) stocks advanced and 283 (80.63%) declined

- 4 stocks rose to a new 52-week high, 29 fell to new lows

- 45.01% of stocks closed above their 200-day average

- 31.91% of stocks closed above their 50-day average

- 8.83% of stocks closed above their 20-day average

Outperformers:

- + 12.28%-Future PLC(FUTR.L)

- + 3.30%-Anglo American PLC(AAL.L)

- + 2.76%-Discoverie Group PLC(DSCV.L)

Underperformers:

- -9.72%-AO World PLC(AO.L)

- -8.29%-Micro Focus International PLC(MCRO.L)

- -7.05%-Bridgepoint Group PLC(BPTB.L)

Up Next (Times in GMT)

How to trade with City Index

You can easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Forex articles

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 03:59 PM

July 25, 2024 04:37 AM