US futures

Dow futures -0.15% at 36000

S&P futures -0.09% at 4628

Nasdaq futures +0.11% at 15992

In Europe

FTSE -0.43% at 7243

Dax +0.42% at 15961

Euro Stoxx +0.20% at 4303

Learn more about trading indices

It’s all about the Fed

US stocks are pointing to a broadly flat open, hovering near record highs with all eyes towards the Fed. The Fed is widely expected to begin tapering bond purchases from November. The markets have been focused on this announcement for many months. However, given the forward looking nature of the markets this announcement is not likely to be a catalyst for future direction. Instead, commentary surrounding inflation expectations and any clues on the timing of the first rate hike will be key.

Prior to the Fed there is plenty of data for investors to wade through including ISM services PM and factory orders.

US jobless claims surprised to the upside with 571k jobs added in the private sector which bodes well to Friday’s non farm payroll report, which is playing second fiddle to the Fed this month. The upbeat numbers suggest that the labour market recovery is on track. However, let’s not forget that we have several months recently when the ADP has beaten forecasts only for the non farm payroll to disappoint.

Corporate earnings will continue to pour in with Marriott International, Esty, Qualcomm and MGM Resorts all in focus.

Lyft will also be under the spotlight after reporting better than expected Q3 numbers.

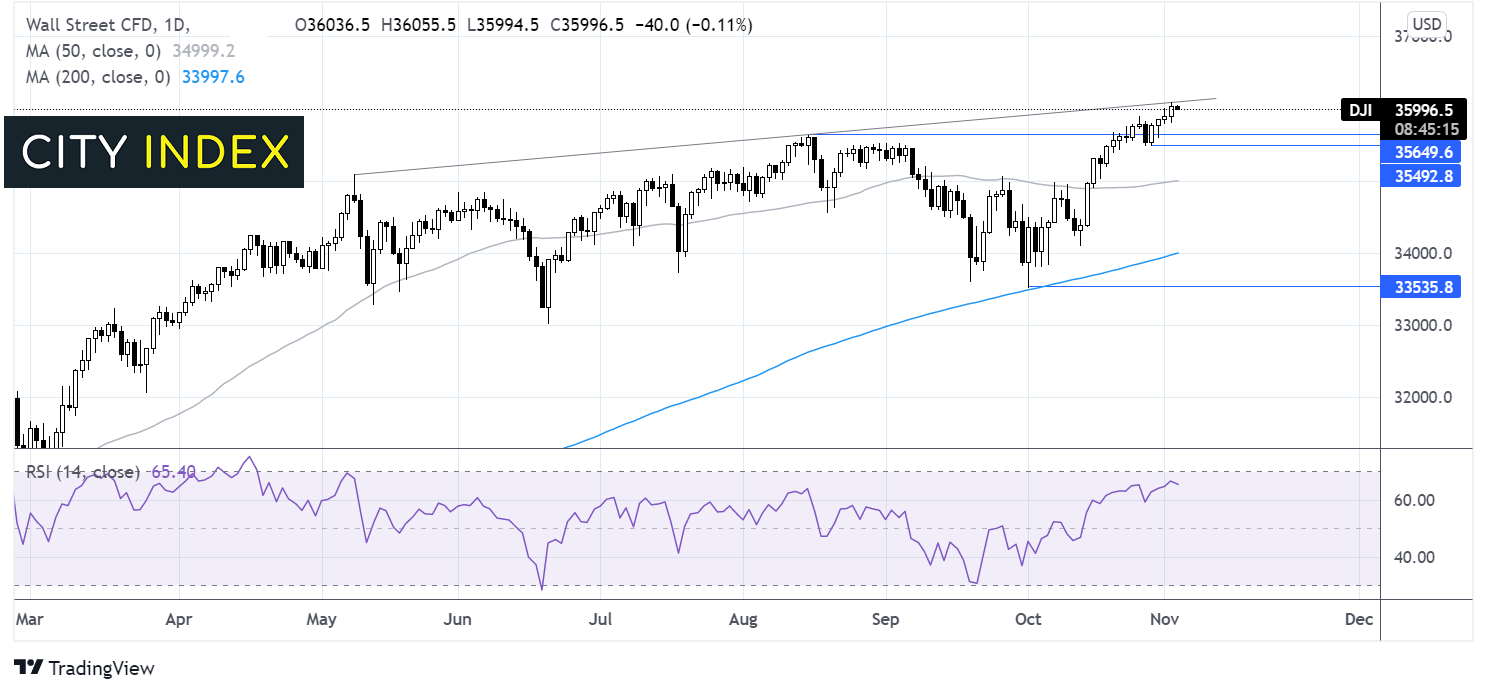

Where next for Dow Jones?

The Dow Jones reached a fresh all time high in the previous session of 36087 the rising trend line resistance. The price is still hovering around key 36000 level, whilst the RSI is supportive of further upside. Even if the price did dip lower it could be a buy the dip scenario. It would take a move below 35650 and 35500 to negate the near term uptrend and for sellers to pick up the pace towards the 50 sma at 35000. Meanwhile buyers are looking for a move above 36087 for fresh all time highs.

FX – USD edges lower, GBP rebounds on strong PMIs

The US Dollar is ticking a few pips lower as investors await the latest Fed monetary policy decision. Prior to that there is plenty of data for USD traders to digest including ISM services PMI.

GBP/USD is rebounding firmly after three straight days of declines. UK services sector activity grew by more than expected in October. The PMI came in 59.1, well up from 55.4 in September and beating forecasts of 58. Given the dominance of the service sector in the UK economy the data bodes well for economic growth. It’s worth noting that the faster growth came despite a record growth in operating costs, which the BoE could fear will be passed on to the consumer lifting inflation.

GBP/USD +0.32% at 1.3654

EUR/USD +0.07% at 1.1587

Oil looks to API data as supply remains tight

Oil prices are falling lower for a second straight session following a larger than expected build in oil inventories. According to the API industry report US crude stock piles grew by 3.6 million barrels, following a build of 2.3 million in the previous week. Expectations had been for a build of 1.6 million barrels. Meanwhile gasoline inventories fell by 552,000 barrels. This marked the sixth straight week crude oil inventory build.

Attention will now turn to the EIA inventory report due shortly and the OPEC meeting tomorrow. OPEC are widely expected to stick to the output plan that was agreed in July.

WTI crude trades -2.15% at $81.33

Brent trades -2% at $82.82

Learn more about trading oil here.

Looking ahead

13:45 Markit Services PMI

14:00 ISM Services PMI

14:00 Factory Orders

14:30 EIA Crude Oil Stocks

18:00 Fed Rate Decision

18:30 Fed Press Conference

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Indices articles

July 25, 2024 01:30 PM

July 25, 2024 01:01 AM

July 25, 2024 12:41 AM

July 24, 2024 07:26 PM