Asian Futures:

- Australia's ASX 200 futures are up 7 points (0.1%), the cash market is currently estimated to open at 7,406.40

- Japan's Nikkei 225 futures are up 90 points (0.31%), the cash market is currently estimated to open at 29,392.66

- Hong Kong's Hang Seng futures are down -103 points (-0.42%), the cash market is currently estimated to open at 24,582.50

- China's A50 Index futures are up 1 points (0.01%), the cash market is currently estimated to open at 15,720.85

UK and Europe:

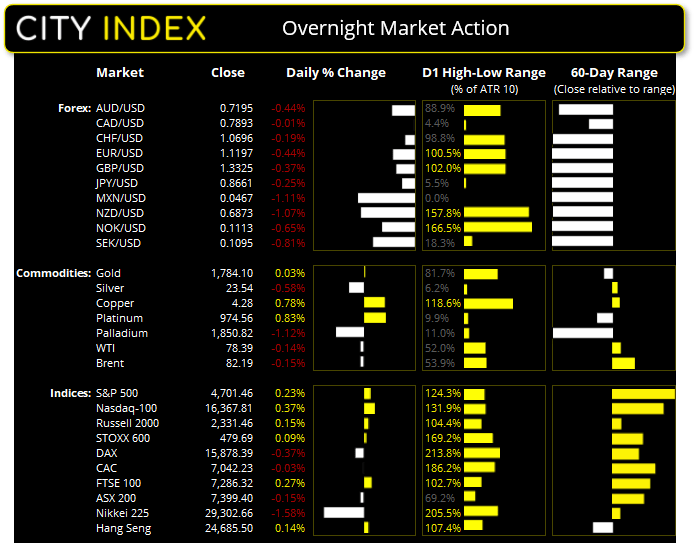

- UK's FTSE 100 index rose 19.63 points (0.27%) to close at 7,286.32

- Europe's Euro STOXX 50 index fell -7.57 points (-0.18%) to close at 4,276.25

- Germany's DAX index fell -58.61 points (-0.37%) to close at 15,878.39

- France's CAC 40 index fell -2.39 points (-0.03%) to close at 7,042.23

Wednesday US Close:

- The Dow Jones Industrial fell -9.42 points (-0.03%) to close at 35,804.38

- The S&P 500 index rose 10.76 points (0.23%) to close at 4,701.46

- The Nasdaq 100 index rose 61.098 points (0.37%) to close at 16,367.81

Inflation is hot, consumers are still pessimistic and growth isn’t what it once was.

That pretty much sums up US data released overnight. Oh, and the FOMC minutes were slightly more hawkish than expected. The Fed’s preferred inflationary gauge rose to its’ highest level since the early 90’s, taking Core PCE to 4.1% and PCE to 5%. Although not sure why we’d expect anything less, given it is simply tracking all other inflationary measures in tandem. GDP was revised slightly higher to 2.1% but below 2.2% expected. And the University of Michigan Consumer Sentiment Survey confirms that consumers are their most gloomy in 10 years, quite simply because inflation is so high.

Under normal circumstances the Fed would raise rates, but they cannot (or dare not) until they have finished tapering, so in all likelihood they need to accelerate the taper to get on with hikes. And that is being reflected in the bond markets as investors flocked to the long-end of the curve to send yields lower, as they fled the short end to send yields higher.

USD extends it rally

The US dollar was the strongest major overnight as bets are on for a more responsive Federal Reserve. The Australian dollar fell back below 72c to a 7-week low as investors expect the positive yield differential for the Aussie to diminish. But as the US is now effectively on a long weekend thanks to Thanksgiving, and we haven’t really learned anything new surrounding inflation, perhaps AUD can hold above the September low before the weekend.

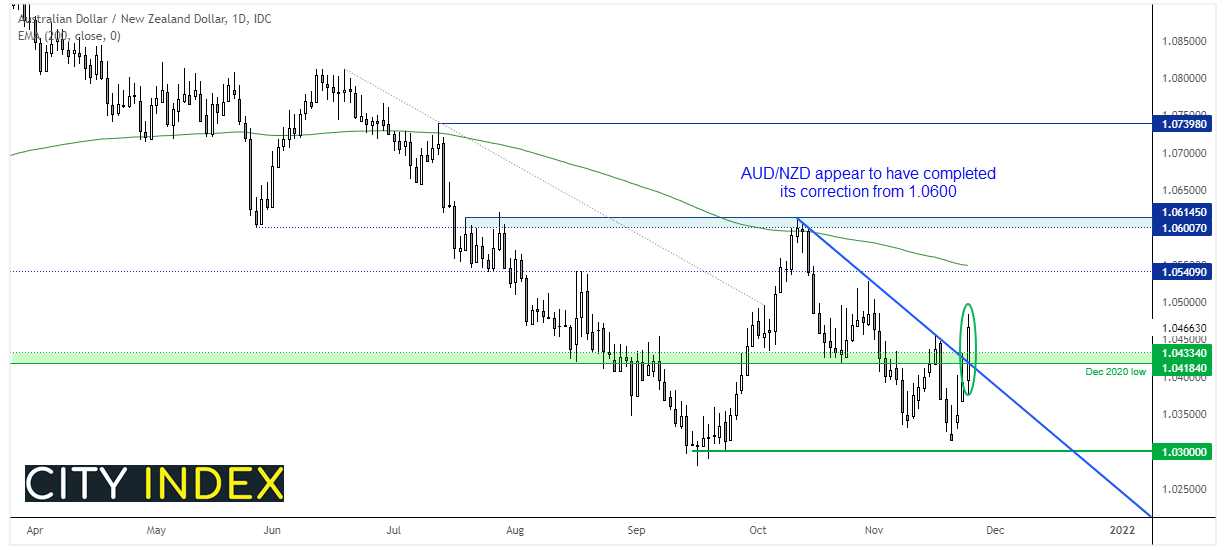

AUD/NZD breaks out – correction complete?

AUD is performing much better against the Kiwi dollar since RBNZ were not as hawkish as some were positioned for yesterday. AUD/NZD hit a 3-week high and we think it has seen an important swing low on 19th November. Traders had been anticipating a hike from RBNZ for the past several weeks, so those traders have cashed out and now mean reversion is underway. AUD/NZD broke above trend resistance and the 1.0418/33 resistance zone, which we’re hoping can now turn into support. Our bias remains bullish above yesterday’s low.

Gold down around $100 in just over a week

Gold prices spent another day below $1800 and have now fallen close to $100 in the past six session. It has found support at the September trendline so perhaps we’ll see a small bounce, but take note that the 200-day eMA sits at $1800 making it a likely resistance level.

ASX 200 Market Internals:

ASX 200: 7399.4 (-0.15%), 24 November 2021

- Energy (1.22%) was the strongest sector and Information Technology (-0.56%) was the weakest

- 4 out of the 11 sectors closed higher

- 7 out of the 11 sectors closed lower

- 5 out of the 11 sectors outperformed the index

- 67 (33.50%) stocks advanced, 117 (58.50%) stocks declined

- 60.5% of stocks closed above their 200-day average

- 52% of stocks closed above their 50-day average

- 48% of stocks closed above their 20-day average

Outperformers:

- + 3.52%-Polynovo Ltd(PNV.AX)

- + 3.23%-LendLease Group(LLC.AX)

- + 2.4%-Beach Energy Ltd(BPT.AX)

Underperformers:

- -8.61%-TechnologyOne Ltd(TNE.AX)

- -5.6%-Pinnacle Investment Management Group Ltd(PNI.AX)

- -5.56%-Netwealth Group Ltd(NWL.AX)

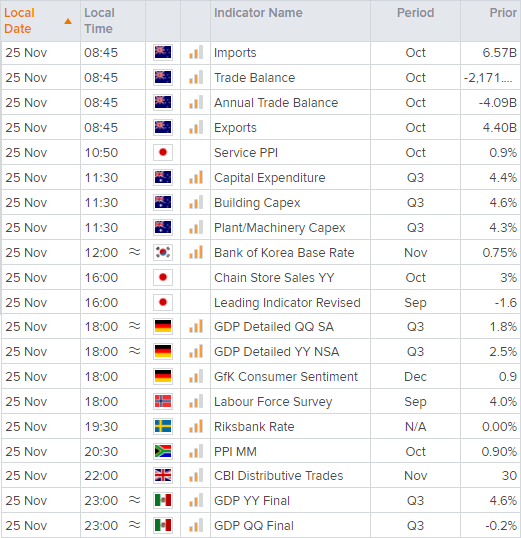

Bank of Korea – the most hawkish of them all?

RBNZ claimed to be the most hawkish, but then BOK pipped them to the post and were in fact the first to raise rates. And they’re expected to do it again today 12:00. According to a Reuters poll, 29 out of 30 economists expect them to raise to 1% from 0.75% (and the ‘one’ expecting a 50 bps hike). More hikes are also expected next year, so if you want a sneak peak of where policy is headed in Asia, keep an eye on BOK.

But first, Australia released Q4 capex data which gives a sneak peak into potential GDP figures. Q1 peaked at 6.3% and fell to 4.4% in Q2, and it is expected to fall to -2% given the lockdown seen in Victoria and New South Wales.

How to trade with City Index

You can easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM