Last week was not for the feint heated as investors grappled with headlines surrounding the implosion of SVB, Signature Bank and of course Credit Suisse. And that was particularly the case for bond markets, with the MOVE index (a measure of implied volatility for treasuries) rising to its highest level since 2007, jut shy of 200. Trading ranges for commodity markets were more than twice their usual ATR, and some currencies and indices were in excess of 150% their usual ATR. Now we’re curious to see whether sentiment can be restored this week, in light of recent headlines surrounding UBS and Credit Suisse.

UBS to acquire Credit Suisse

Following tense weekend talks, UBS has agreed to purchase Credit Suisse by the end of the year for Fr 3 billion ($4.5 billion). To the bemusement of Credit Suisse investors, ~$14 billion worth of CS bonds have evaporated into thin air. As for the workforce, the estimated 9,000 job cuts which were expected is now likely to increase. The move is estimated to boost UBS customer deposits to Fr 333 billion from 167 billion, and increase its loan book to 307billion from 143 billion.

SNB (Swiss National Bank) to the rescue (again)

Ahead of the talks on Friday, the SNB had agreed to provide Credit Suisse a $54 billion liquidity gap. This was in response to Saudi National Bank – their main backer – refusing to send across any more money following Credit Suisse’s own admission that their financial reporting had ‘material weakness’.

The UBS deal is reported to include Fr 100 billion in liquidity assistance from the SNB. Furthermore, the federal government is to provide a loss guarantee of up to 9 billion for their portfolio, beyond which UBS then assumes responsibility. However, they have to sustain up to Fr 5 billion in losses initially before the government funding arrives.

Six major central banks announced coordinated action to boost liquidity

The Fed and five other central banks announced a coordinated move to increase liquidity in US dollar swap arrangements. Other central banks include the ECB, BOJ, BOE, BOC and SNB. Central Bank heads were quick to endorse the UBS deal, as they continue to put out fires and a maintain s stance of confidence front that all is fine. RBA’s assistant governor Kent also gave a speech on the lags of monetary policy, and stating that despite the volatility, Australian Banks are ‘unquestionably strong’.

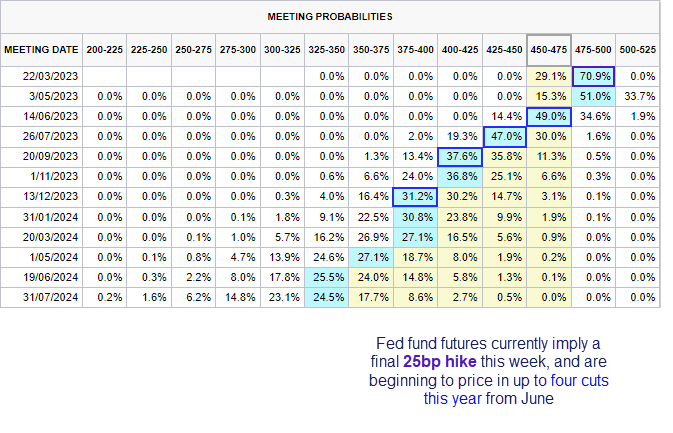

As legend has it, the Fed keep on raising rates until something breaks. And we seem to have reached that point. And that is why Fed fund futures are beginning to price in four Fed cuts this year, after a final 25bp hike on Wednesday to 5%. On a sidenote, I suspect the Fed’s message will not be as dovish as the fed funds curve currently implies, given the defensive (and coordinated) steps they have taken to control any damage, and inflation is still three times higher than their mandate.

How will markets react to these latest developments?

And that leads us to an important question; is everything now fine, and will it lead to a risk-on tone? There’s a slight feeling of relief during early Asian trade with JPY, CHF and USD currently the weakest FX majors and commodity FX (AUD, CAD) leading the pack with EUR coming in third place. Oil prices have also stabilised above Friday’s 15-month low, although there seems to be no immediate appetite to bid it higher. USD/JPY is hold above 132 despite intraday attempts to breach it over the past three days, and if sentiment ‘behaves’ it may be able reclaim some of last week’s losses heading into Wednesday’s FOMC meeting.

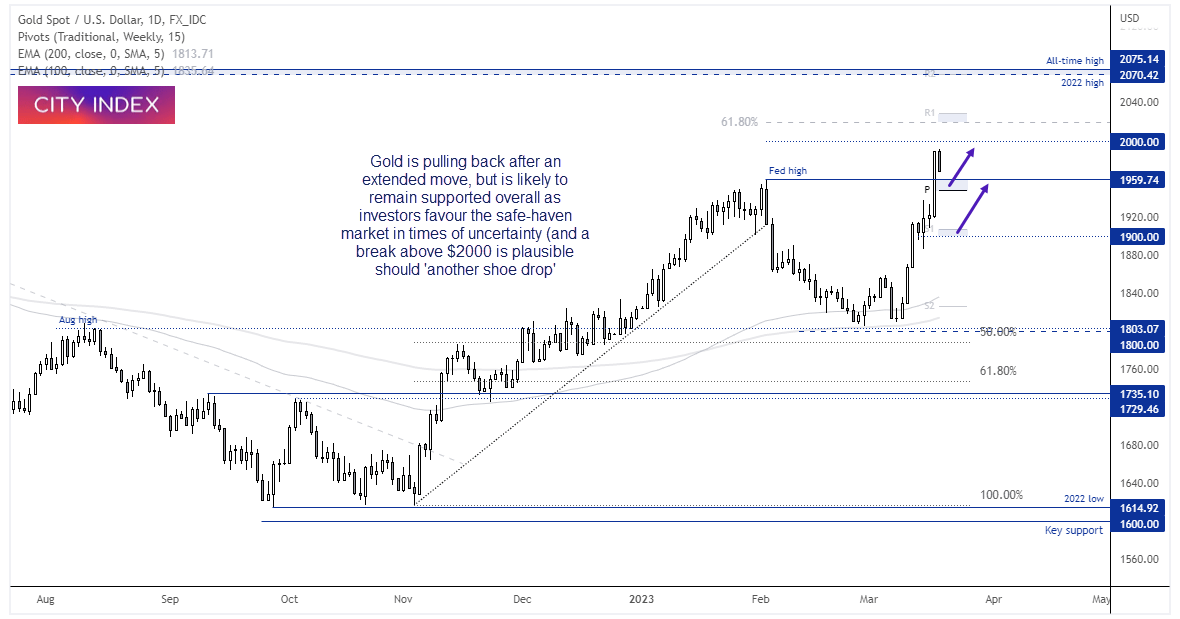

Gold has also pulled back from Friday’s high – which stopped just $11.50 shy of $2000 – and shows the potential to retest $1960 today as mean reversion kicks in. It had its best day and week on Friday since March 2020 as the yellow metal regains its safe-haven status. And if it pulls back further than the weekly pivot, I suspect bulls would be tempted to bid it higher above 1900 anyway.

Overall, these are hardly the signs of a ‘risk-on’ session and more akin to a sigh of relief with a large dose of suspicion and paranoia. We saw a similar response in Asia last Monday, only to see European markets and Wall Street continue to slide. Investors are likely keeping a look over their shoulder for the next disaster in a high-interest rate (and inflationary) environment, so at best we might see markets recover some of last week’s losses. But it is hard to see a ‘China is reoponing’ style rally any time soon. If so, it’s also a good reason to expect gold prices to remain supported as it has clearly regained its safe-haven status. And it could easily break above the $2000 milestone if or when the next show drops.

Where from here for UBS?

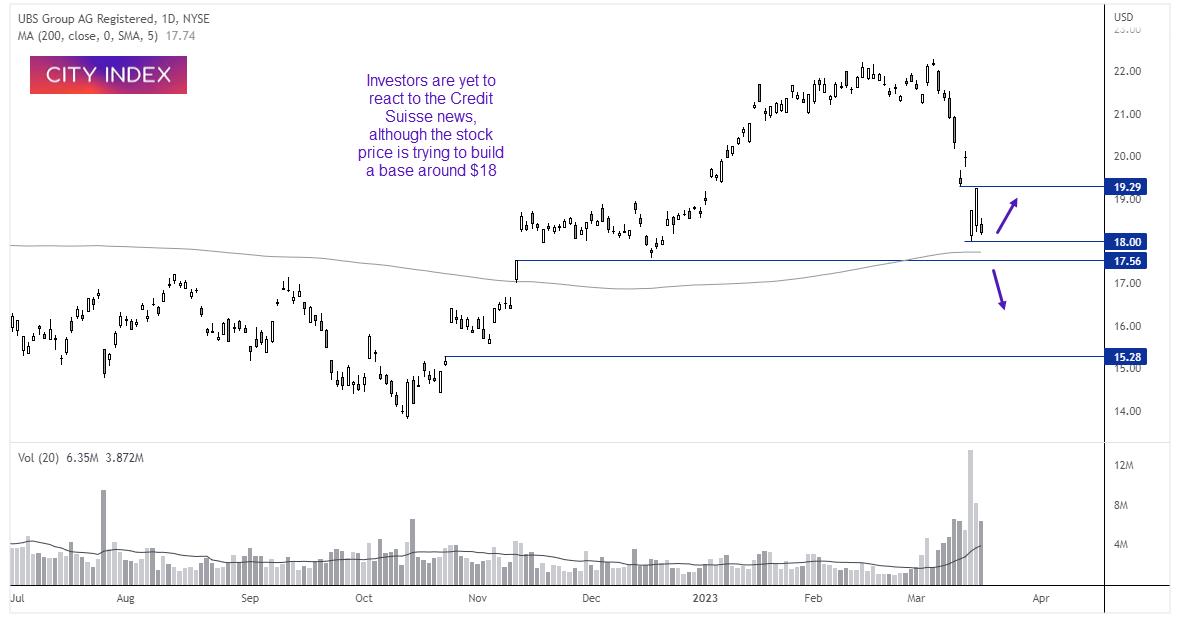

The stock price for UBS has fallen -19.3% since the March high in just seven trading sessions. With investors fixated on the completely made up ‘20% bear market’ threshold, I often find that markets turn around at that magic 20% level. $18 has provides a level of support, with its 200-day MA and $17.56 gap support just below. Of course, none of these levels will matter if we find bank runs continue to increase and institutions fail, in which case a break below $17.56 assumes all is not well globally, and / or investors are not happy with the purchase of Credit Suisse. Either way, the key levels are easily defined.

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM