It’s been nearly three months since the RBNZ last announced a cash rate decision, where they hiked interest rates by 75bp to take the cash rate to 4.25%. The tightening cycle has seen 400bp added, the November 75bp hike being the most aggressive increment of the cycle. The question now is whether they will add another 75bp to take rates to 5% or go with a mere 50 to take rates to 4.75%.

Looking through the notes of the November meeting, it was a hawkish 75bp hike – which left an a general assumption that another 75bp hike is due in February. In fact, they also discussed a potential 100bp hike, which shows they mean business. Yet since then, a few things have happened which may warrant a 50bp hike this week. Not only did inflation undershoot RBNZ’s own forecasts (7.2% compared with 7.5% expected), but a measure of business confidence has hit a record low and their business PSI is barely expanding at all, which suggests the economy is indeed slowing. Furthermore, their 2-year inflation expectation measure slipped to 3.3% from 3.6%, although the 1-year remains historically high at 5.1%.

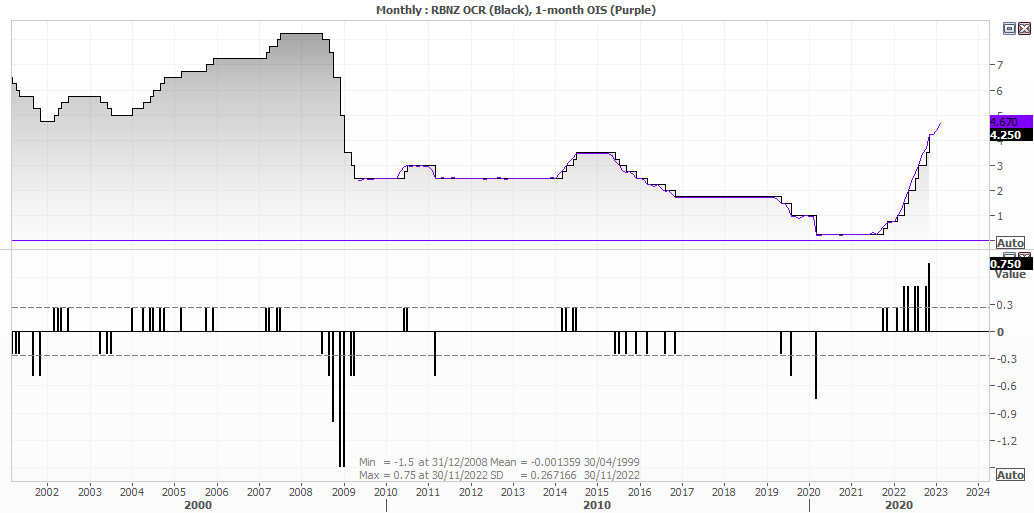

All in all, I suspect a 50bp hike is the more likely scenario, but it is no slam dunk – as a 75bp hike is not an impossible scenario. A Reuters poll shows 20 out of 25 economists back a 50bp hike, and for rates to peak at 5.25% by June. If correct, that could indicate a 50bp hike this week, and a final 25bp hike in April or May. Currently the 1-month OIS (overnight index swap) suggest an 84% probability of a 50bp hike, and I’m inclined to believe it. Therefore, the focal point will be down to how hawkish (or not) the statement is deemed to be, and whether they’ll indicate that they’re approaching the end of the tightening cycle. We will also look for any adjustments to the forecasts, as a lower CPI expectation could also signal less of a need to hike rates further.

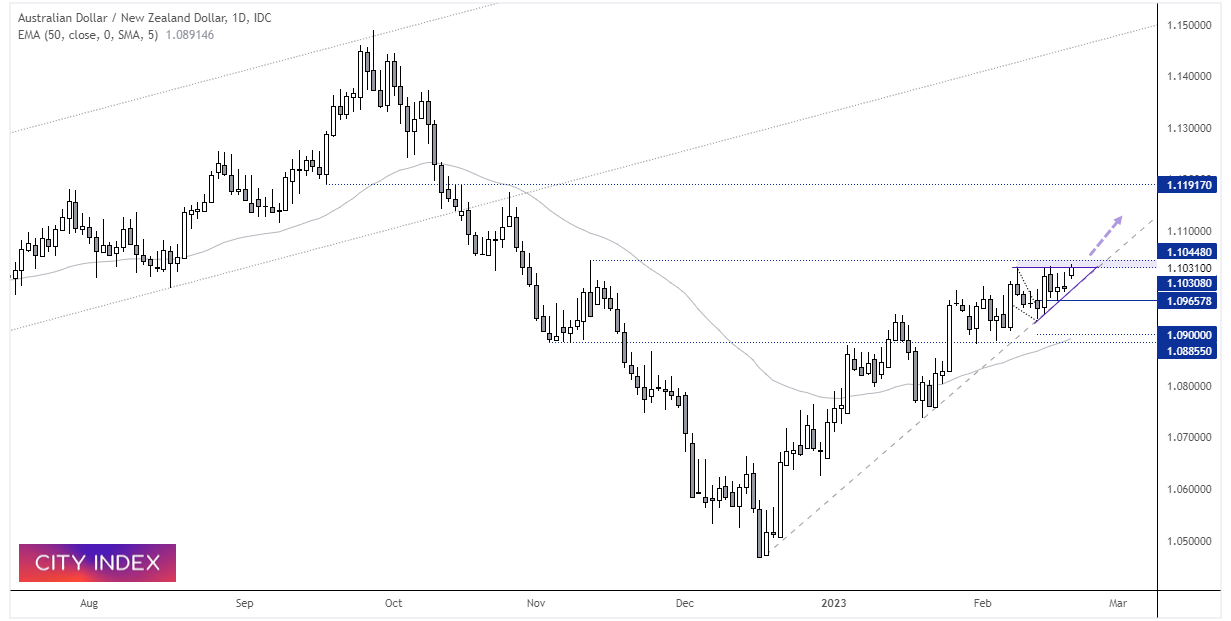

AUD/NZD daily chart:

The cross reached out bullish target outlined last week, and appears to be considering a bullish breakout. Indeed, a dovish hike could help the pair move higher and print a fresh YTD high. Price action remains above trend support and a small triangle formation is forming on the daily chart, which generally assumes a breakout in the direction of the underlying trend. Still, if RBNZ surprise with a hawkish hike (or go for 75bp) then we’d expect a momentum shift at these highs and for a break of the bullish trendline.

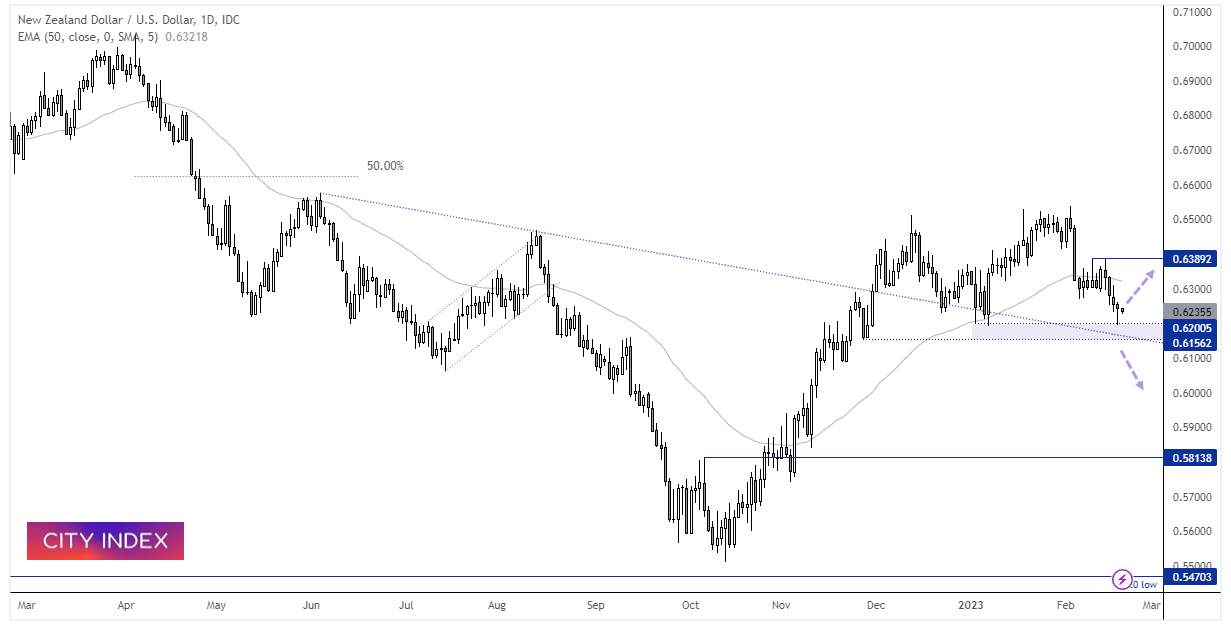

NZD/USD daily chart:

NZD/USD has reached out 62c target outlined last week and printed a bullish hammer, to hint at a swing low. For NZD to stand any chance of a decent bounce, we’ll likely need a dovish RBNZ hike and a soft US inflation print later this week. Otherwise, we’d consider fading into minor rallies towards 0.6300 and anticipated a break below 0.6156.

Upcoming meetings:

- February 22nd (Monetary Policy Statement)

- April 5th

- May 24th (Monetary Policy Statement)

- July 12th

- August 16th (Monetary Policy Statement)

- October 4th

- November 29th (Monetary Policy Statement)

RBNZ November meeting:

Summary of November’s statement

- Hiked by 75bp

- OCR needed to reach a higher level, sooner than previously indicated

- Core CPI is too high, employment too tight, and near-term inflation expectations have risen

- NZ household spending remains resilient (supported by savings)

- Rebound in tourism is also supporting domestic demands

- Wage pressures are evident

- A range of indicators continuing to signify broad-based inflation pressure

- Monetary conditions needed to continue to tighten further

Summary of November minutes:

- Actual and expected inflation need to declined considerably

- Tourism spending will make a strong economic contribution over the coming months

- Capacity constraints could inhibit tourism and add to inflation pressures

- Household savings and income growth may support consumption now and in the future

- Reduction of aggregate demand expected to cause GDP to temporarily contract mid-2023

- Dip in growth is necessary to return inflation to target

- Risks to inflation from fiscal policies are skewed to the upside

- Increments of 50, 75 and 100bp were considered

- 75 favoured due to resilience in domestic spending and higher and persistent actual and expected inflation

What’s happened since November?

- Retail sales rose 2.6% in Jan (-2.3% in December)

- Business PSI 50.6 (slowest expansion in nine months)

Business sentiment:

- QSBO shows business sentiment and activity taking a turn for the worse - Quarterly Survey of Business Opinion, January 2023.

- 73% of business expect general economic conditions to deteriorate over the coming months – the weakest over the survey’s history.

- The weaker demand is limiting the ability of retailers to increase prices in the face of intense cost pressures.

- almost half of mortgages due for repricing over the coming year.

Inflation:

- CPI 7.2% (3-decade high) but below RBNZ’s forecast of 7.5% (economists expected 7.1%)

- Non-tradables inflation, a closely watched indicator of domestic price pressures, held at 6.6%. The RBNZ projected 7%.

- Food price index 1.7% m/m (6-month high, driven by groceries)

- 1-year inflation expectations remains elevated at 5.1%

- 2-year expectation fell to 3.3% from 3.6%

- CitiFX inflation surprise index peaked in November, ahead of the RBNZ’s final meeting of 2022

- Producer prices (inputs and outputs) slumped in Q3

Opinions on Wednesday’s meeting:

- ANZ have downgraded their forecast for a ‘mere’ 50bp hike next week (down from 75bp) and the their terminal rate projection lowered to 5.5% from 4.25%

- ASB Bank in Auckland still expect a 75bp hike

- ING have called a 50bo hike, and terminal rate to ‘come soon’

- Reuters polls favours terminal rate of 5.25 by mid-June

- Reuters: 20 out of 25 expect a 50bo hike next week, 5 said 75bp

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM