The following report is a guest contribution from Vincent Deluard, CFA, and was originally published on October 26th.

Vincent is the Director of Global Macro Strategy at StoneX Group, and we are grateful for his blessing to share an example of the type of deep-dive, institutional-level research that he is creating on a weekly basis. If you find this report interesting, please consider subscribing to Vincent’s research directly to receive all of his insights directly and review past reports.

A Brief History of the 2% Target and a Better Framework for Inflation

The 1913 Federal Reserve Act of 1913 established the Federal Reserve System as the central bank of the United States to provide the nation with “a safer, more flexible, and more stable monetary and financial system”. It mandates that the Federal Reserve “conduct monetary policy so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates”.

The Federal Reserve’s mandates do not have a numerical definition – although one could argue that “stable prices” means no inflation at all. Inflation was not properly tracked or measured until World War 1 caused rapid increases in prices, particularly in shipbuilding centers. The Bureau of Labor Statistics began the publication of price indices for 32 cities in 1919.

The notion that central banks should target a certain price level is very new. For most of its history, central banks’ goals were to finance the government, increase reserves of precious metals, and maintain the value of the currency. In the 70s, monetarism focused on controlling the supply of money to stabilize the economy. It was only after monetarist policies defeated inflation that economists turned their focus on the growth of prices, rather than the money supply.

The 2% target itself has a purely anecdotal origin. The governor of the Reserve Bank of New Zealand, Don Brash, casually mentioned it on a TV interview in 1988 as a target which seemed neither too high nor too low. This target spread first to the Bank of Canada and the Bank of England in 2003. The 2% target only became the explicit target for the Federal Reserve in January 2012.

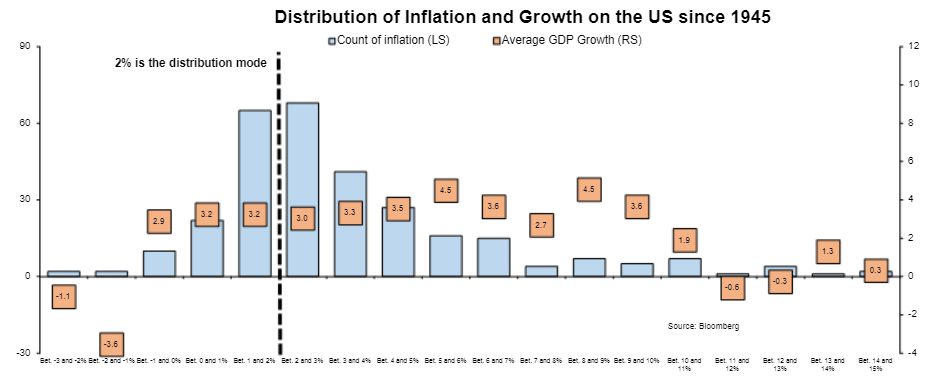

Looking at quarterly US inflation since 1945, 2% is indeed the mode of the mode of the distribution, but inflation has shown considerable variation and there is no evidence that a 2% inflation rate leads to superior economic growth.

On the contrary, real growth averaged 3.8% when inflation has been between 4 and 10%, versus 3.1% when it has been between 1 and 3%. The only clear link between inflation and growth is that growth tends to be lower when inflation is deeply negative or when it is above 10%.

Source: Bloomberg, StoneX

Why 2% is No Longer an Appropriate Inflation Target

“R-star” is the real interest rate that is neither expansionary nor contractionary when the economy is at full employment. Since R-star cannot be observed or calculated ex ante, it can be the object of endless arguments between economists, and it can be used by central bank mandarins as a code word to silence their uninitiate critics.

I would prefer economists spend more time on “I-star”, the optimal level of inflation which allows the economy to grow, the government to finance itself, and achieves generational fairness.

I would argue that a low I-star was probably justified from 1990 to the 2010s. The global economy experienced three massive deflationary shocks, and it would have been vain for policymakers to swim against these strong currents.

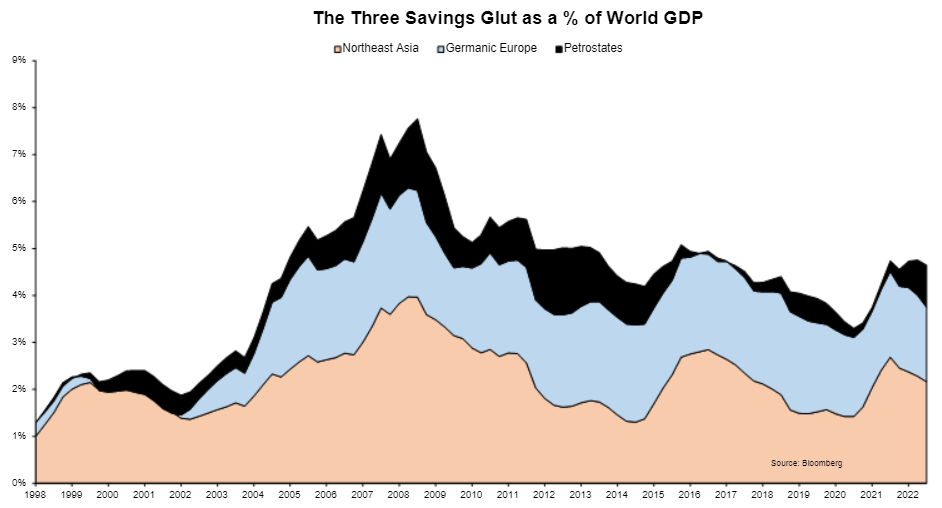

First, the world experienced a savings glut. At the global level, current accounts match the supply of savings with the demand for consumption and investment. In the late 90s, three groups of countries simultaneously desired a much higher level of savings, which reduced the global cost of capital.

Northeast Asia in general and China in particular adopted mercantilism, domestic demand repression, and reserve accumulation policies. The reasons for these policies are complex (demography, Confucian values, and fear of the International Monetary Fund come to mind) and exceed the scope of this paper, but the results were clear: the current account surpluses of China, Japan, and South Korea rose to 4% of global GDP in 2008 from 1% in 1998.

The launch of the Euro in 1999 gave Germany and Europe’s hyper-productive North a cheap currency for the first time in a generation. A surge in exports ensued. Germany’s massive surpluses were initially recycled into the Club Med countries. After the sovereign debt crisis destroyed Mediterranean countries’ consumption and public spending, Germany’s savings were dumped onto the rest of the world. The current account surpluses of Germany, the Netherlands, and Switzerland rose to 2.5% of global GDP in 2007 from 0% in 1999.

The explosion in commodities prices and the exhaustion of conventional oil fields in the US and the North Sea made a few dictatorial, sparsely-populated countries fabulously rich. These countries did not have the economic capacity to invest this windfall domestically and there were few checks on their leaders’ egos. The petrodollar glut flowed into sovereign wealth funds, central banks’ reserves, secret bank accounts in Switzerland and Singapore, prestige properties in Mayfair, condos in Miami, and European football clubs. The current account surpluses of Russia and Saudi Arabia rose to 1.5% of global GDP in 2009 from 0% in 1998.

Source: Bloomberg, StoneX

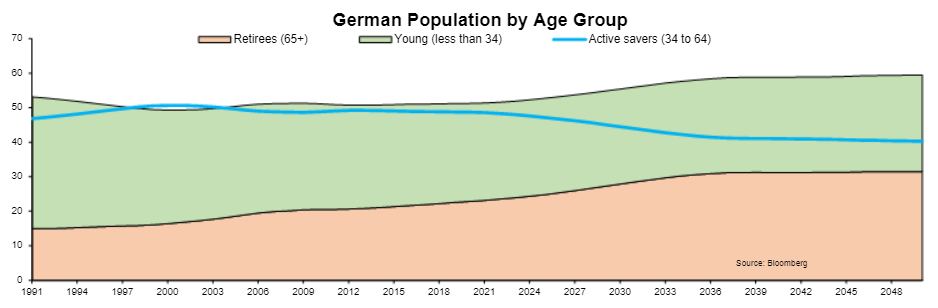

Second, Western economies collected an unprecedented demographic savings dividend. The median boomer was born in 1955 (the mid-point for the 1946-1964 generation and the period with the highest live births in US history), turned 40 in 1995, 50 in 2005 and 60 in 2015. Following the lifecycle theory, households become net savers at about 40 as the big household formation expenses are completed. Savings rise with wages and peak when workers become empty nesters in their late 50s. This demographic savings dividend was especially large in post-War Europe because mortality spiked during the War, births exploded during the baby boom, and collapsed after the oral contraceptive pill was popularized in the 70s. The boomer generation was abnormally large and had few parents or children to take care of. In Germany, the ratio of prime savers (ages 34 to 64) to net consumers (retirees or young) peaked in 2002.

Source: Bloomberg, StoneX

Third, Mexico also experienced a baby boom in the 50s and the 60s. Unfortunately, the milagro mexicano (Mexico’s high-growth period between 1940 and 1970) ended just as this large generation entered the labor force when the Mexican economy and much of its middle-class were destroyed by the Tequila crisis. Fortunately, the US was experiencing a prolonged expansion and a historical bubble in the late 90s. Millions crossed the Southern border in search of a better life. The population of Mexican immigrants in the US rose to almost 12 million in 2010 from 2 million in 1995. These 10 million Mexicans were mostly of working age, had no trouble integrating in the historically-Hispanic southwestern states, and provided the US agriculture and service sectors with an endless supply of cheap and industrious workers.

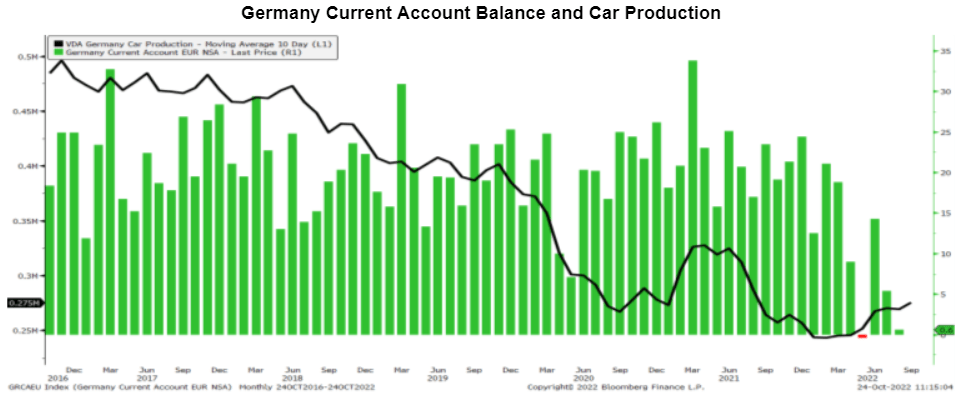

These three deflationary tailwinds have stopped or reversed. First, the global savings glut is quickly deflating. Because of soaring producer prices, the Japanese current account posted its first monthly deficit in 50 years in January. So did Germany’s in May. The global chip shortage, soaring gas prices, and Chinese lockdowns are a deadly three- hit combo for Germany’s most prized exports: Germany’s car production has halved since its pre-Covid peak.

Source: Bloomberg, StoneX

Russia’s savings are obviously not flowing into Western government bonds and luxury real estate anymore, and the seizure of Russia’s foreign exchange reserves sent a powerful signal to commodity-producing countries with a tense relation with the West – a list which could soon include Saudi Arabia given the personal hostility between Joe Biden and Mohammed Bin Salman.

Third, Mexico is ageing rapidly. The total fertility rate has fallen from 6.7 children per woman in 1968 (¡Ay, Dios!) to 2.1 in 2019. The median age rose from 18 in 1980 to 31 now and should reach 40 in 2050, when Mexico will be older than the US. As a result, the population of Mexicans living in the US has decreased steadily since 2007.

Due to the backlash against immigration and the fact that no country is as large, as close, and as integrated to the US as Mexico, there will never be another similar influx of cheap, hard-working migrants into the US labor force.

Last, inflation targeting is inherently political and the dis-inflation of the past two decades resulted in the enrichment of the old at the expense of the young. The consumer price index is an average, but generations have different consumption baskets. For example, Medicare covers medical expenses for Americans above 65 so they are not exposed to healthcare inflation. Older folks typically own their homes, so they do not pay rent - and sometimes collect it. They do not go to college either, so they are not impacted by tuition inflation, which has outpaced the CPI-U index by 287 percentage points since 1990.

On the other hand, rents, college tuition, and health insurance typically account for more than half of the young’s consumption expenses.

More broadly, dis-inflation leads to positive real rates at first, and eventually very low rates. Both favor the old and penalize the young. Positive real rates mean that capital compounds faster than wages grow. If you do not feel like reading the 816 pages of T. Piketty’s “Capital in the 21st Century”, you can just remember its fundamental insight: when ‘r’ is greater than ‘g’, capital grows faster than wages, wealth concentrates in the top 1%, and inequalities explode over time.

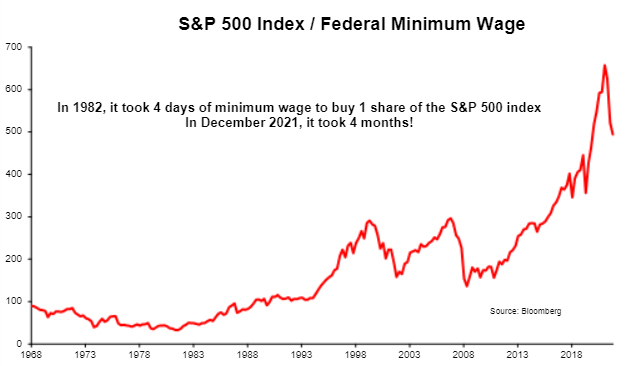

Second, financial assets are worth their future cash flows, discounted to the present. The lower this discount rate, the higher the value of stocks, bonds, and homes. Wages rise slowly when inflation is low so that the cost of financial assets in terms of labor rises: four days at the minimum wage bought one share of the S&P 500 index when boomers came of age in 1982. Forty years of falling rates inflated the price of this same share of the index to four months at the minimum wage. Low inflation and low rates advantage those who own a lot of assets (the old) at the expense of those whose main resource is their labor (the young).

Source: Bloomberg, StoneX

This section showed that the level of inflation is not a God-given constant, but a flexible target which can be adjusted to better fit the economic environment and social goals. By imposing an artificial 2% target, politicians have lost a policy tool. This did not matter in the past three decades because the natural rate of inflation (I-star) was low and falling anyway, but the next decade of secular inflation will require politicians to renounce the golden calf of the 2% target. How this might happen is the object of this last section.

To read about the investing implications of a decade of secular inflation, please consider subscribing to Vincent’s research directly to receive all of his insights and review past reports.

Disclaimer

This commentary is intended for Institutional and Investment Professional Use Only and may not be distributed to the investing public. The views expressed are those of the author and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and StoneX Group Inc. disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, should be construed as market commentary, merely observing economic, political and/or market conditions, and not intended to refer to any particular trading strategy, promotional element or quality of service provided by StoneX Group Inc. or its affiliates. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results StoneX Financial Inc. a registered broker dealer, member FINRA, SIPC, MSRB, is a wholly owned subsidiary of StoneX Group Inc.

This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Past performance does not guarantee future results.

Investments in commodities may have greater volatility than investments in traditional securities, particularly if the instruments involve leverage. The value of commodity-linked derivative instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Use of leveraged commodity-linked derivatives creates an opportunity for increased return but, at the same time, creates the possibility for greater loss.

Indices are unmanaged and investors cannot invest directly in an index. Unless otherwise noted, performance of indices do not account for any fees, commissions or other expenses that would be incurred. Returns do not include reinvested dividends.

The Consumer Price Index (CPI) is a measure of inflation compiled by the US Bureau of Labor Studies. The Consumer Price Index for All Urban Consumers (CPI-U) is a monthly measure of the average change over time in the prices paid by consumers for a market basket of consumer goods and services. The CPI-U is based on the spending patterns of urban consumers.

The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is a market value weighted index with each stock's weight in the index proportionate to its market value.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Inflation articles

July 15, 2024 04:21 PM

July 12, 2024 01:32 AM

July 12, 2024 01:32 AM

July 9, 2024 04:52 PM