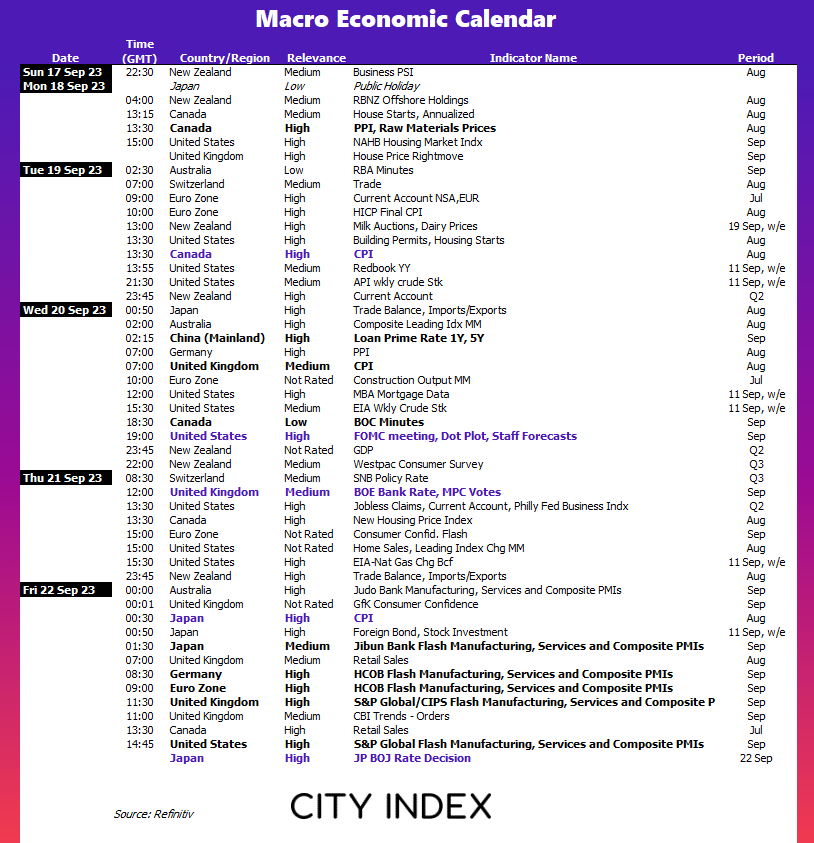

FOMC, BOE, BOJ meetings, CPIs and flash PMIs: The Week Ahead

Whilst the Fed are expected to hold rates steady in September, next week’s FOMC meeting also includes the quarterly staff projections. And changes to dot plot or CPI estimates can be as good as a hike where market reactions are concerned. The odds of another BOE are next week are not as high as they were, which makes the preceding inflation report paramount to expectations for their next decision. And whilst the BOJ are unlikely to act, that is no reason to drop your guard given their tendency to surprise once in a while. We also have flash PMIs for major regions and inflation data to mull over.

The week that was:

- ECB hiked their interest rate by 25bp, and their statement hinted that it could be the last hike of the cycle (although Lagarde denied this at the press conference

- US CPI came in hotter than expected, although the initial market response was muted as higher prices were largely expected anyway

- Yet when the US delivered strong retail sales data producer prices and lower jobless claims data, the US dollar regained its strength and sent EUR/USD below 1.0700

- US yields have paused around historical cycle highs yet again, despite US inflation picking up

- WTI crude oil broke to a YTD high and above $90 as tight supply concerns outstripped concerns of a global slowdown

- USD/JPY produced a relatively large weekend opening gap on Monday after BOJ Ueda discussed the potential of the central bank hiking interest rates, although made it clear it would not likely be this year

The week ahead (calendar):

This content will only appear on City Index websites!

Earnings This Week

Look at the corporate calendar and find out what stocks will be reporting results in Earnings This Week.

The week ahead (key events and themes):

- FOMC interest rate decision, staff projections

- BOE interest rate decision

- BOJ interest rate decision

- Inflation data for the UK, Canada, Europe and Japan

- Flash PMIs

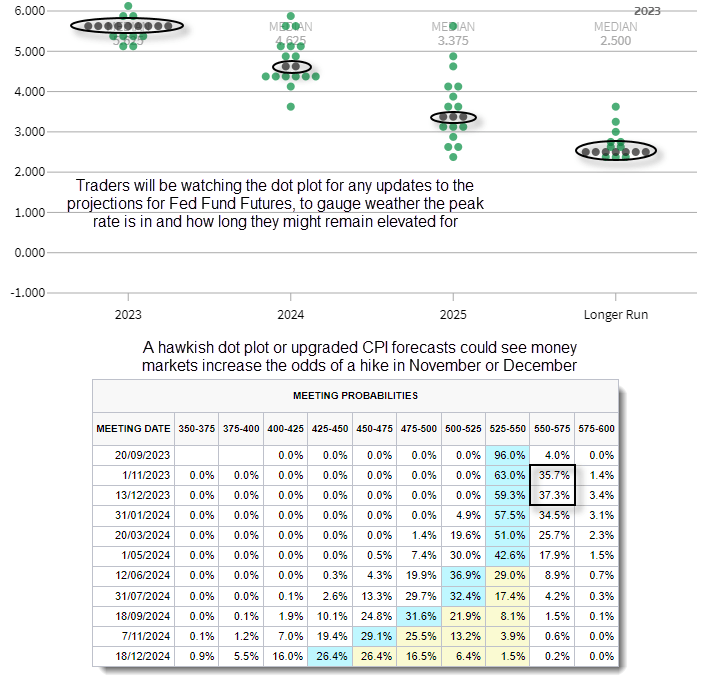

FOMC interest rate decision, staff projections

With Fed fund futures implying a 96% chance of the Fed holding interest rates next week, it would be an understatement to say that it would come as a surprise to markets if they hiked. Even though CPI, PPI, and retail sales all beat estimates this week, the FED Funds curve still favours the current target band of 5.25-5.5% as the terminal rate. However, they still imply a ~36% chance of a hike in November or December. Therefore, next week's FOMC meeting is really about how it will shape expectations for meetings from November and beyond.

This meeting will also include an update to the quarterly staff forecasts. In Q2, the median Fed rate was upgraded from 5.125% to 5.625%, implying that two more hikes were expected. The median forecasts for 2024 and 2025 were also upgraded, fuelling the "higher for longer" narrative. Given that we have already seen one of the two expected hikes implied in the Q2 projections, traders really want to know if the median has been lowered to signal that the current rate is the terminal rate. However, if it remains elevated, it suggests that there is one more hike to follow in November or December (assuming they don't stun markets with a hike next week).

It is also important to keep an eye on the updated forecasts for inflation. This will give a fuller picture of how hawkish the Fed is likely to be. If growth is updated, it will also feed back into the theme of a soft landing. However, if inflation is upgraded alongside growth, it would be deemed a more hawkish meeting and likely support the US dollar to the detriment of Wall Street indices.

Market to watch: EURUSD, USD/JPY, WTI Crude Oil, Gold, S&P 500, Nasdaq 100, Dow Jones

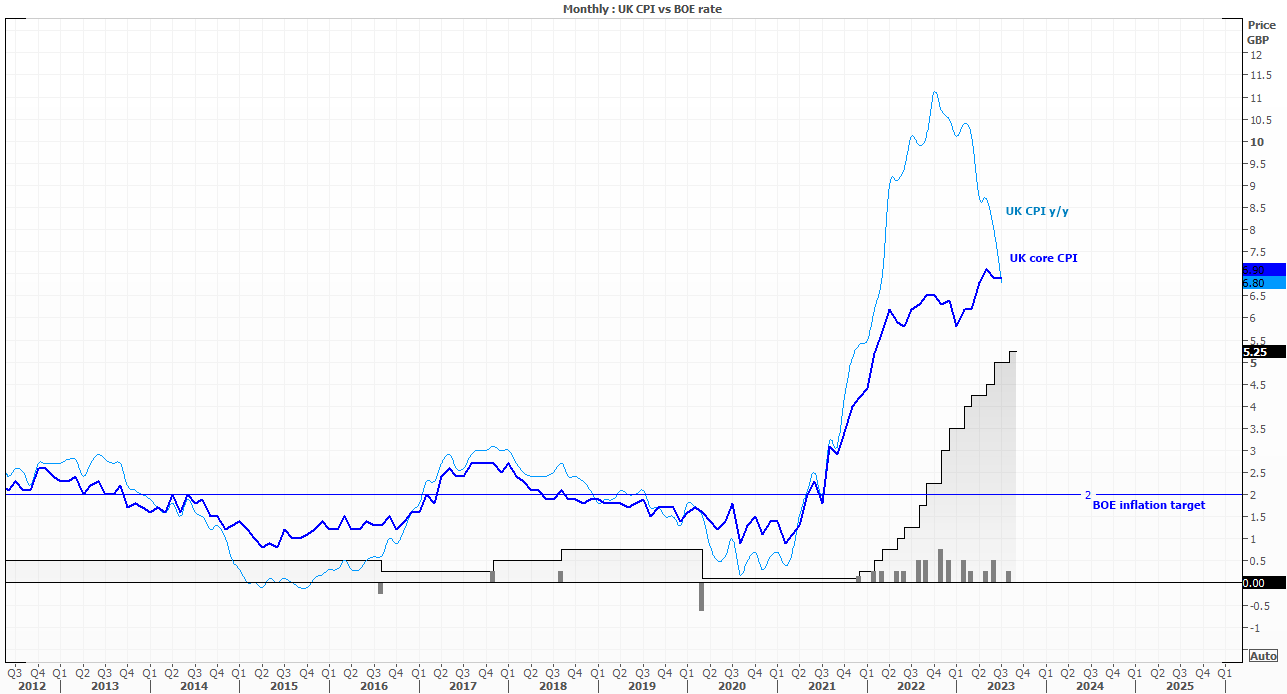

UK inflation and Bank of England (BOE) interest rate decision

Headline wage figures rose a staggering 7.8% y/y, or 8.5% including bonuses. Given the BOE have been concerned with a wage spiral and its forces on inflation, the initial assumption is that the central bank is not as close to their terminal rate as recent comments from certain members suggested. Yet these figures may not actually be as hawkish for the BOS, if the Office of National Statistics (ONS) is correct in saying they were bumped higher by “the NHS and Civil Service one-off payments made in June and July 2023”. And ING analysts suspect pay may have actually fallen recently by if using alternative wage measures based on payrolls.

Furthermore, employment growth fell at its fastest pace since August 2020 at -220k, GDP was estimated at -0.5% m/m versus -0.2% expected, construction output and industrial production also missed estimates and mortgage applications are falling. So, if next week’s inflation data comes in soft, perhaps the BOE are indeed close to the end of their tightening cycle.

The BOE’s interest rate currently sits at 5.25% and the 1-month OIS implies a 44% chance of a hike next week. The 3-month OIS has fully priced in one more hike, so it seems markets expect on more hike this cycle although the timing remains unclear. And that may leave’s next week’s CPI report to decide if the hike is next week or later in the year.

Market to watch: GBP/USD, GBP/JPY, EUR/GBP, FTSE 100

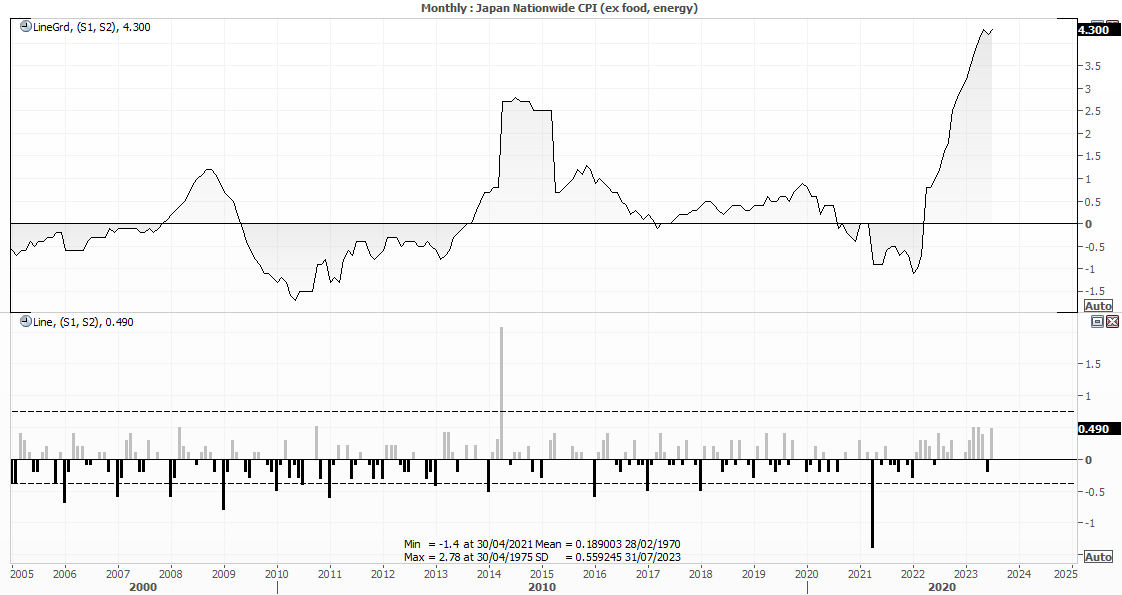

Bank of Japan (BOJ) interest rate decision, Japan’s inflation and trade data

It is the usual drill with BOJ meetings; it is unlikely that we will see a policy change, but you need to keep your guard up for a surprise, just in case. If anything makes this one different, it is that BOJ governor Ueda is now vocal about the potential for the central bank to hike rates, even if it is not likely to happen this year. However, this has fuelled speculation that they may now opt to hike rates before abandoning their yield curve control (YCC). Besides, they widened their YCC band at their last meeting, so I do not personally think they will abandon it so soon. A Reuters poll also shows that 73% of economists expect the central bank to abandon YCC next year, although only 41% expect it to end negative interest rates next year.

While there was some excitement generated in the money markets for an increase in hikes recently, we have to go out to the 9-month overnight index swap (OIS) before it prices out negative interest rates. And even then, that is pulling back towards zero.

Inflation and trade data is also released. The CPI metric to keep an eye on is core excluding fresh food and energy, as it builds a case for a more hawkish BOJ if it continue to rise. It rose 4.3% in June and August which was 42-year highs. And with the monthly read rising another 0.5% (and increasing 6 of the past 7 months) then a print of 0.6% or higher could bring forward expectations of a BOJ hike and weigh on USD/JPY.

Market to watch: USD/JPY, AUD/JPY, GBP/JPY, EUR/JPY, Nikkei 225

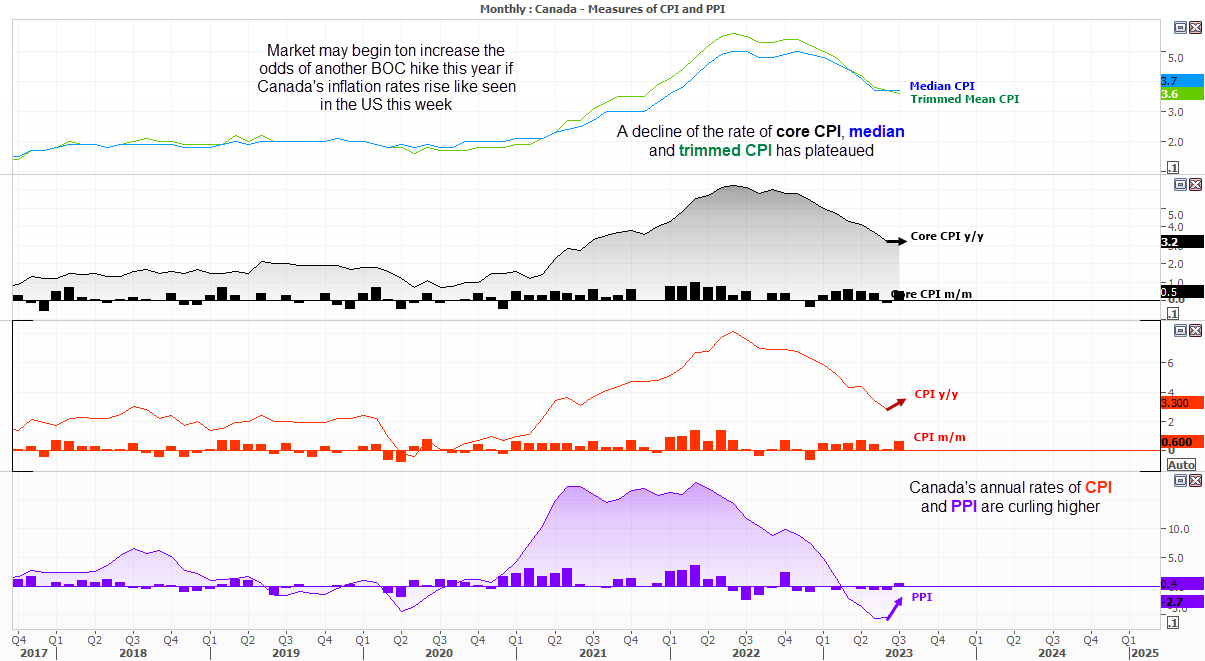

Canada’s inflation report

The Bank of Canada (BOC) held interest rates at 5% last week, although Governor Macklem warned that rates may still not be restrictive enough to bring CPI back to target. However, a recent Reuters poll suggests a 44% chance of another hike this year, the OIS curve has flattened and even the 6-month OIS implies less than a 50% chance of a hike. And that makes Canada’s inflation report next week quite important for traders to assess the probabilities of another hike, because if rises like we saw in the US this week it will increase hawkish expectations of the BOC with it.

S&P global flash PMIs

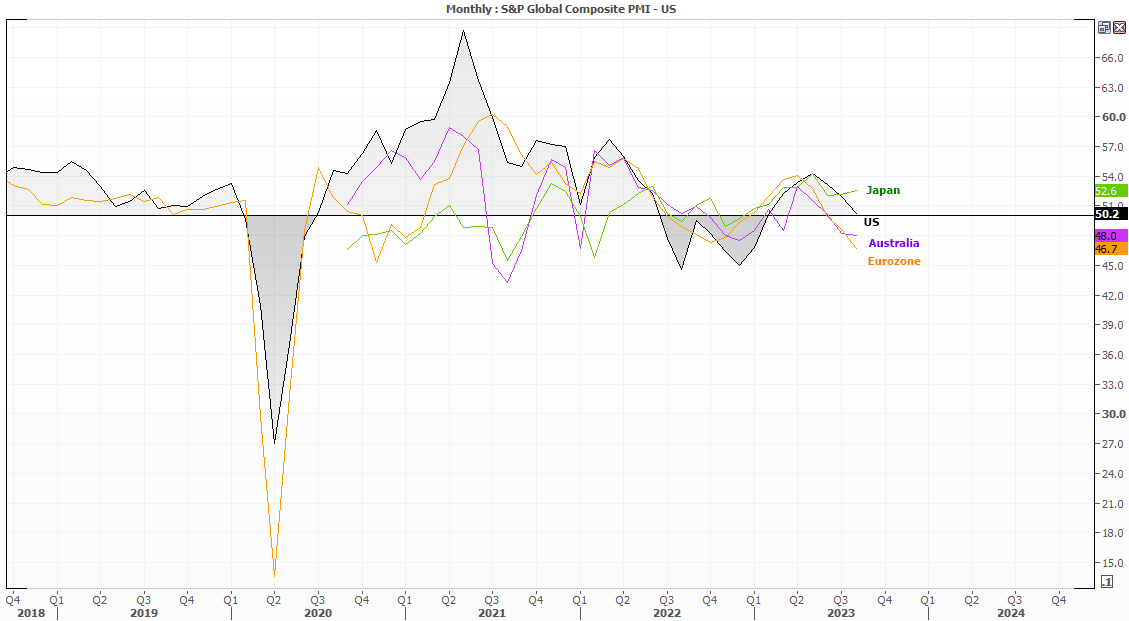

Flash PMIs are released for major economies including the US, Europe, UK and Japan next week. I’m curious to see what if the S&P global composite survey suggests that the US economy has entered a contraction, as it rose to a mere 50.2 last month (above 50 is expansion, below is contraction). Admittedly it may be more exciting if it happened ahead of the FOMC meeting, but it could dampen some hawkish expectations of the Fed if it dips below 50 for the first tie this year. We can see the general trend for Europe and Australia is pointing lower and that Japan is the exception. But traders will also keep an eye on the ‘prices paid’ indices to see if inflationary pressures continue to pick up.

Market to watch: EURUSD, GBP/USD, AUD/USD, USD/JPY, WTI Crude Oil, Gold, S&P 500, Nasdaq 100, Dow Jones

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Week ahead articles

Yesterday 04:48 AM

July 19, 2024 06:20 AM

July 12, 2024 01:32 AM

July 12, 2024 01:32 AM