The start of the new week was positive for risk assets as stocks, foreign currencies and even gold all managing to bounce back after last week’s sell-off. But in the second half of the day, we started to see the dollar come off its lows, supported by even more positive news – this time from the housing market.

So, will the dollar resume its rally?

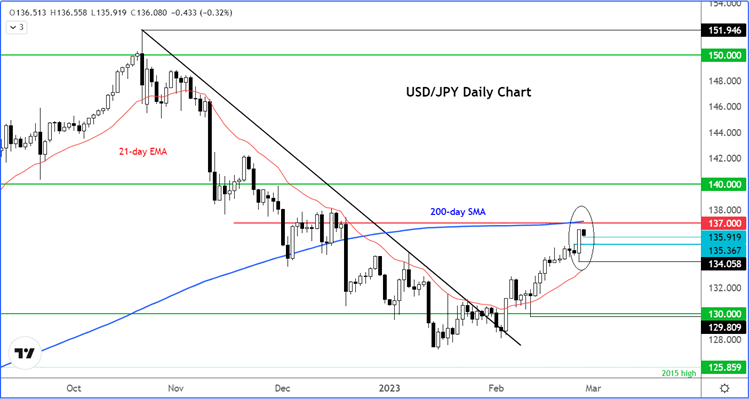

Before discussing the dollar further, let’s have a quick look at the chart of the USD/JPY which broke out above key resistance at 135.35 on Friday:

Source: TradingView and StoneX. See USD/JPY chart on TradingView.

Unless something changes fundamentally, the USD/JPY could be heading towards 137.00 next, where we have the 200-day average converging with a prior resistance level. But it could go on much higher in light of the recent developments and a new BoJ governor keen to maintain status quo. Still, the bulls must ensure to defend this breakout above 135.35 now to maintain control.

In recent weeks, we have seen quite a shift in market direction in favour of the dollar and yields, with most foreign currencies, gold, and US equities falling out of favour. Those moves were as a result of the market changing its expectations for interest rates outlook swiftly higher. Clearly, some traders must now be wondering whether those expectations have been priced in and are thus taking profit on those positions.

However, whether or not this will be the consensus view of the market remains to be seen.

Traders are now pricing US interest rates to peak at 5.4% this year, compared with about 5% a month ago. This is due to various reasons, including stronger US data and an acceleration in the Fed’s preferred inflation gauge (Core PCE Price Index) all helping to dash hopes for an imminent pause in policy tightening.

Unless we see a run of negative news now, the dollar dips could remain support.

In fact, we saw even more evidence of strength in the economy as pending home sales jumped 8.1% month-over-month, when a small rise of 1% was expected.

There’s plenty of macro data to look forward to in the week ahead. Among them, we have CB Consumer Confidence (Tuesday), ISM Manufacturing PMI (Wednesday) and ISM Services PMI (Friday).

Stronger US data has raised hawkish Fed bets, but manufacturing activity has remained weak, with the PMI consistently remaining below 50.0. So far, it has been the services sector where most of the growth has come from. But will we finally see evidence that the manufacturing sector is also beginning to recovery?

Last week saw the S&P Global’s services PMI come in much hotter than expected, albeit at 50.5 the sector barely grew. Nonetheless, it was about 3 points above expectations as the sector returned to growth for the first time since June. The ISM version of the PMI, which last month blew past expectations at 55.2, has historically been more impactful on the markets. If it shows a similar strong reading, then this will further fuel hawkish Fed bets.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM