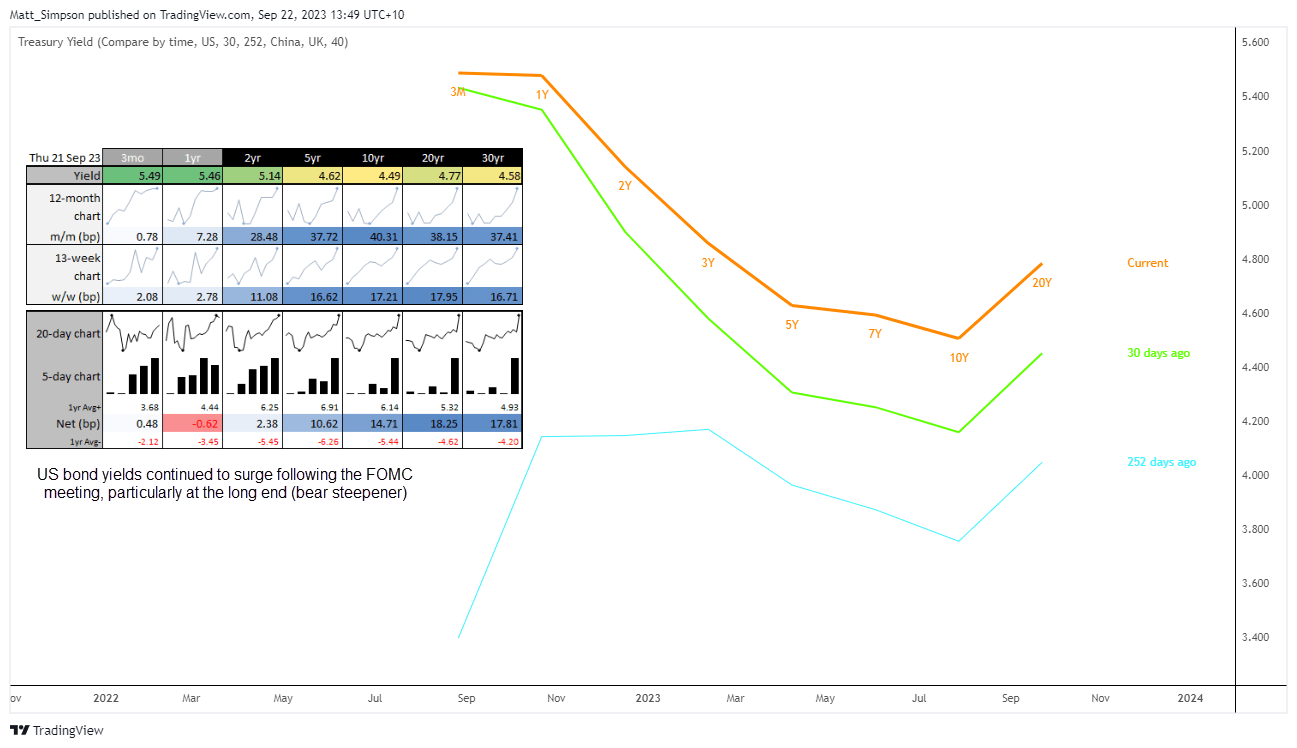

Can bondcano stay on the backburner? The Week Ahead

Bondcano, the phrase coined to described the sharp acceleration of bond yields to the detriment of equities, appears to be smouldering as yields have pulled back from their highs. It has certainly provided some relief for sentiment, given the well-based concerns that something was about to break in the financial system. But with the Fed members now striking a relatively dovish tone, it raises the question as to whether bond investors will now step back into the market to capitalise on attractive yields and take the sting out of bondcano’s tail.

The week that was:

- Gold and oil markets gapped higher at Monday’s open on news that Israel had declared war on Hamas, following a deadly attack over the weekend

- Several Fed members hinted that the surge in bond yields could prompt them to tread carefully and continue holding rates, prompting Fed Fund futures to drop expectations of a November hike from nearly 30% to around 13%

- The FOMC minutes emphasized the Fed’s ‘higher for longer’ stance which is not entirely new information, but in context of dovish comments on yields and the Middle East conflict it our cold water on the debate of another 25bp hike

- US producer prices came in hotter than expected, although Wall Street happily looked past it and focussed more on dovish comments from Fed members

- The Fed's preferred supercore inflation reading logged the fastest increase of 2023. Combined with a weak 30-year Treasury auction, that saw longer-dated yields lift back towards cyclical highs, boosting the US dollar

- Wall Street continued grinding higher, only interrupted briefly by the shock of the inflation report. Attention now turns to big bank earnings out Friday

- Chinese consumer and producer price inflation remained weak, emboldening calls for additional targeted stimulus measures.

- Oil prices failed to capitalise further on Monday’s rally, instead turning lower by mid-week and closing the weekend gap to suggest oil traders have less of a rosy outlook on the economy

- RBA’s deputy governor Kent said that the RBA was in its “third phase” of monetary policy tightening, meaning it is within an assessment mode to decide if further tightening is required

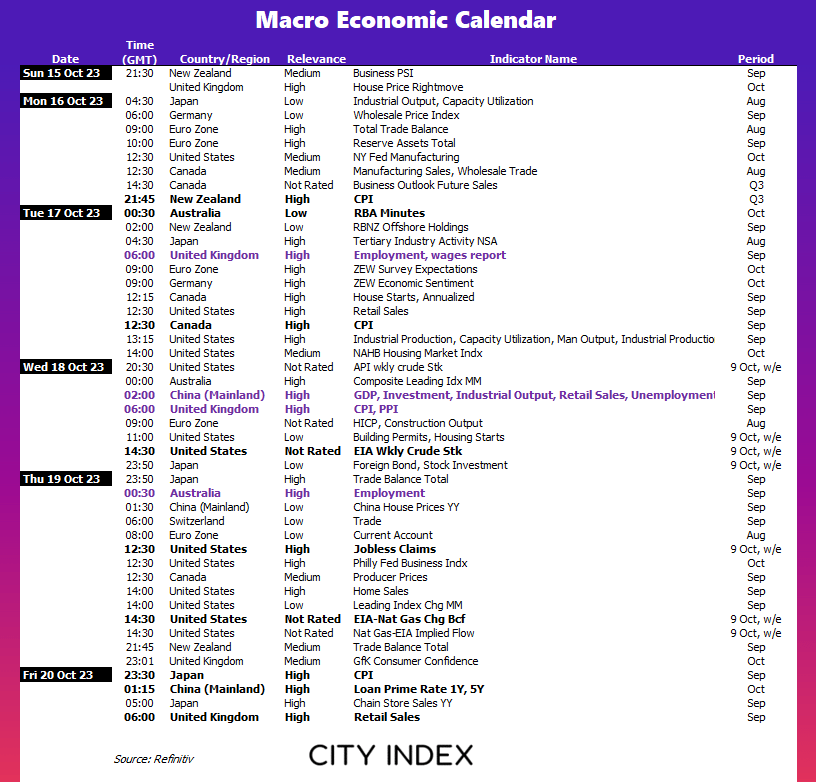

The week ahead (calendar):

This content will only appear on City Index websites!

Earnings This Week

Look at the corporate calendar and find out what stocks will be reporting results in Earnings This Week.

The week ahead (key events and themes):

- Can bondcano stay on the back burner?

- UK employment, wages and CPI

- China data dump

- Canada’s inflation report

- Australian employment

Can bondcano move to the back burner?

The rise in bond yields has certainly raised a few eyebrows and turned a few head s in recent weeks, with the rout of bond prices as yields at the long end of the US yield curve ‘normalise’ and try to close their gap with the shorter end. Yet we appear to have sort of a reprieve, thanks not only to relatively dovish comments from Fed members, but the likelihood that some bond bears have booked profits whilst some investors have come back to support the market. The question now is if these moves can be sustained and allow a relief rally for risk turn into a risk-on rally.

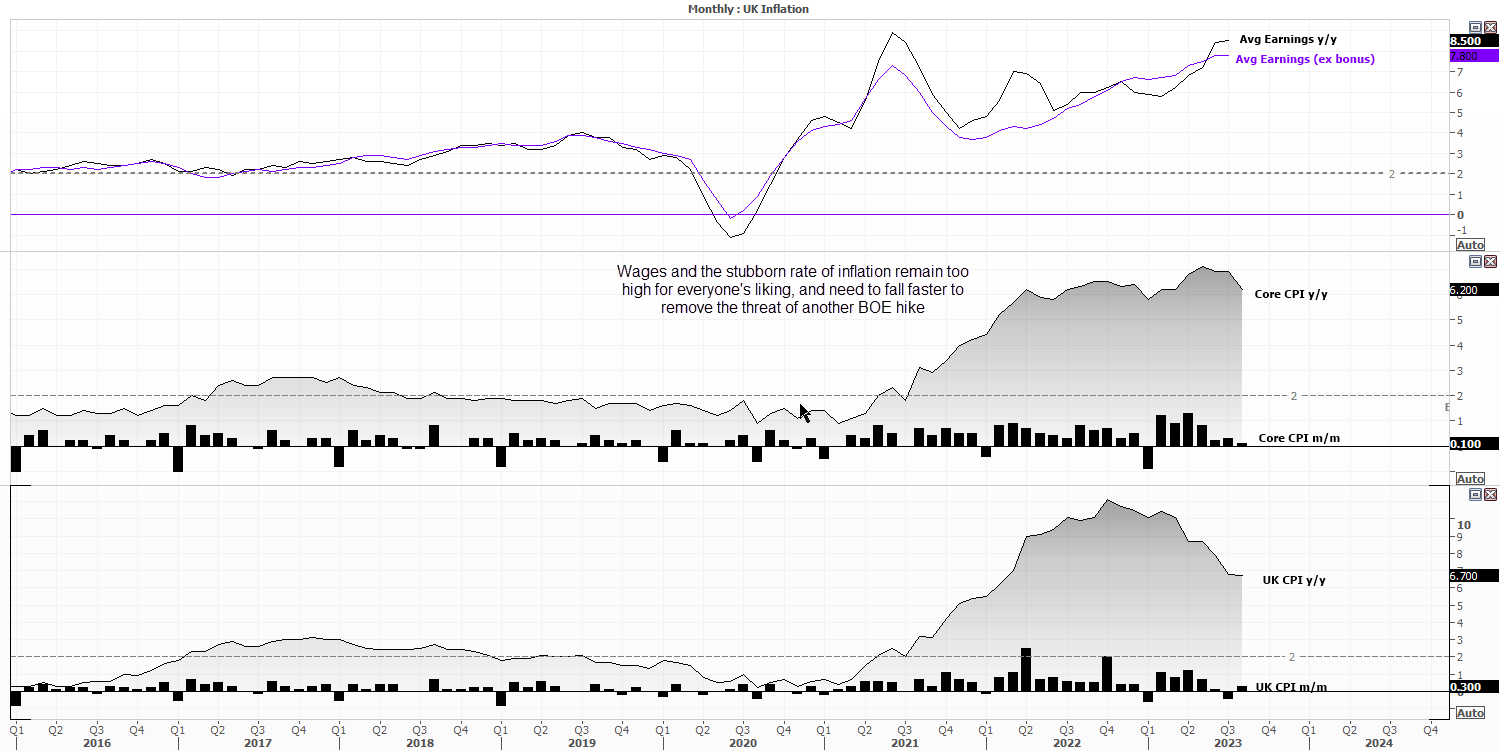

UK employment, wages and CPI

The Bank of England (BOE) have been feeling the political heat and public backlash of higher rates for some time, and you can tell from their wording of their statements and comments that they are more than aware the strain higher rates are having on the economy. But in all the time employment, wages and inflation remain strong, rates will either need to be hiked further or remain elevated for longer, at a bare minimum.

Once again, the BOE had seemingly reached a stage where they were laying the groundwork for a peak rate by actually holding interest rates at a meeting for once. Yet already they are cautiously backtracking, with one member saying that whether they hike again “remains an open question”.

Tuesday’s employment and wages report can set the expectations for Wednesday’s inflation report, with hotter pay and stronger employment likely raising bets of a hike. And if that is followed by stronger-than-liked inflation report, the British pound should be able to lift itself further up from its multi-month lows.

Market to watch: GBP/USD, GBP/JPY, EUR/GBP, FTSE 100

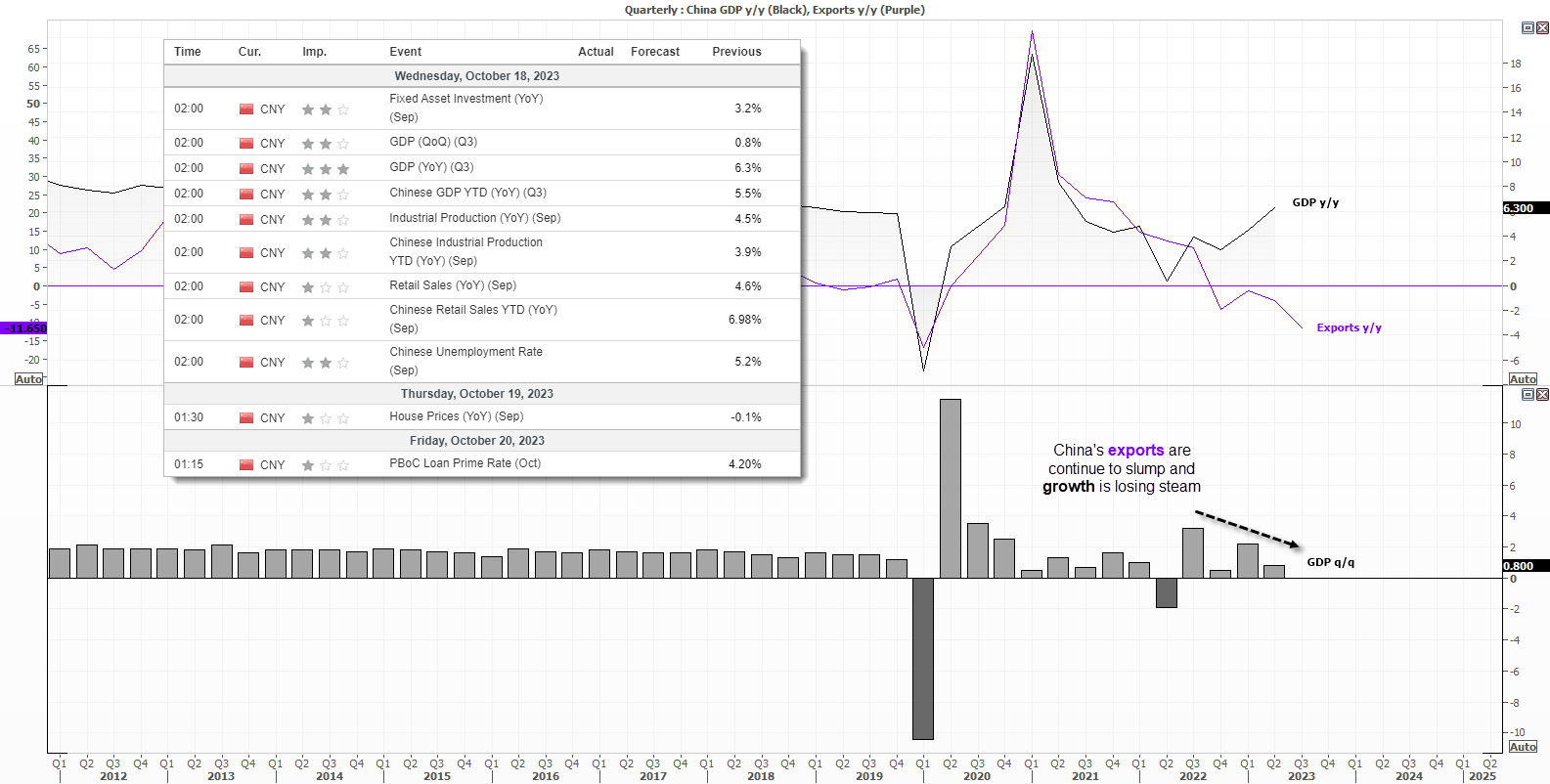

China data dump

The PBOC will likely hold their loan prime rates steady again. And that means all eyes will be on the host of economic data, which includes GDP, industrial output, retail sales, investment, employment data plus more. And Q3 GDP is the centre piece. Q2 data surprised to the downside with a growth rate of just 0.8% q/q and 6.3% y/y (7.3% was expected), and much of the data heading into Q3 was also lacklustre. The World Bank and IMF also cut their growth forecasts for 2023. And whilst PMIs are not as bad as they were, the property crisis is expected to worsen and that could weigh further on the ‘domestic demand’ China’s government seek. Ultimately, with so much disappointment with data overall, the only real surprise left is for data to far outperform expectations, which could boost appetite for risk on APAC equities and AUD/USD.

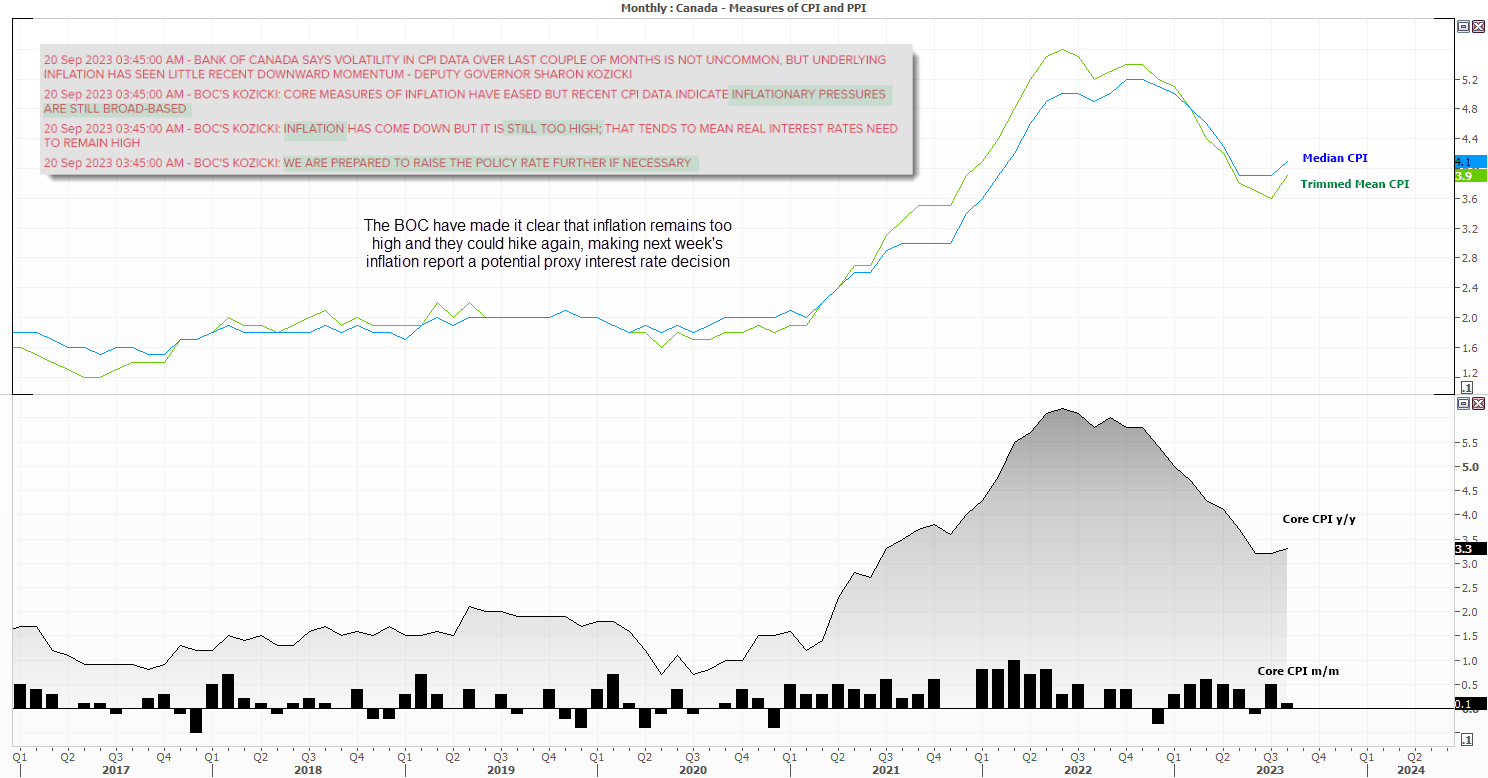

Canadian inflation

The Bank of Canada (BOC) were quick to point out that inflation is too high and that they’re prepared to hike further if necessary. And who can blame them, with the median and trimmed CPI measures turning higher form already elevated levels. And that means next week’s inflation report could in effect be a proxy interest rate decision, as another hot print likely means the central bank could be forced to hike by 25bp to 5.25% on October 25.

Market to watch: USD/CAD, CAD/JPY, AUD/CAD, EUR/CAD, GBP/CAD

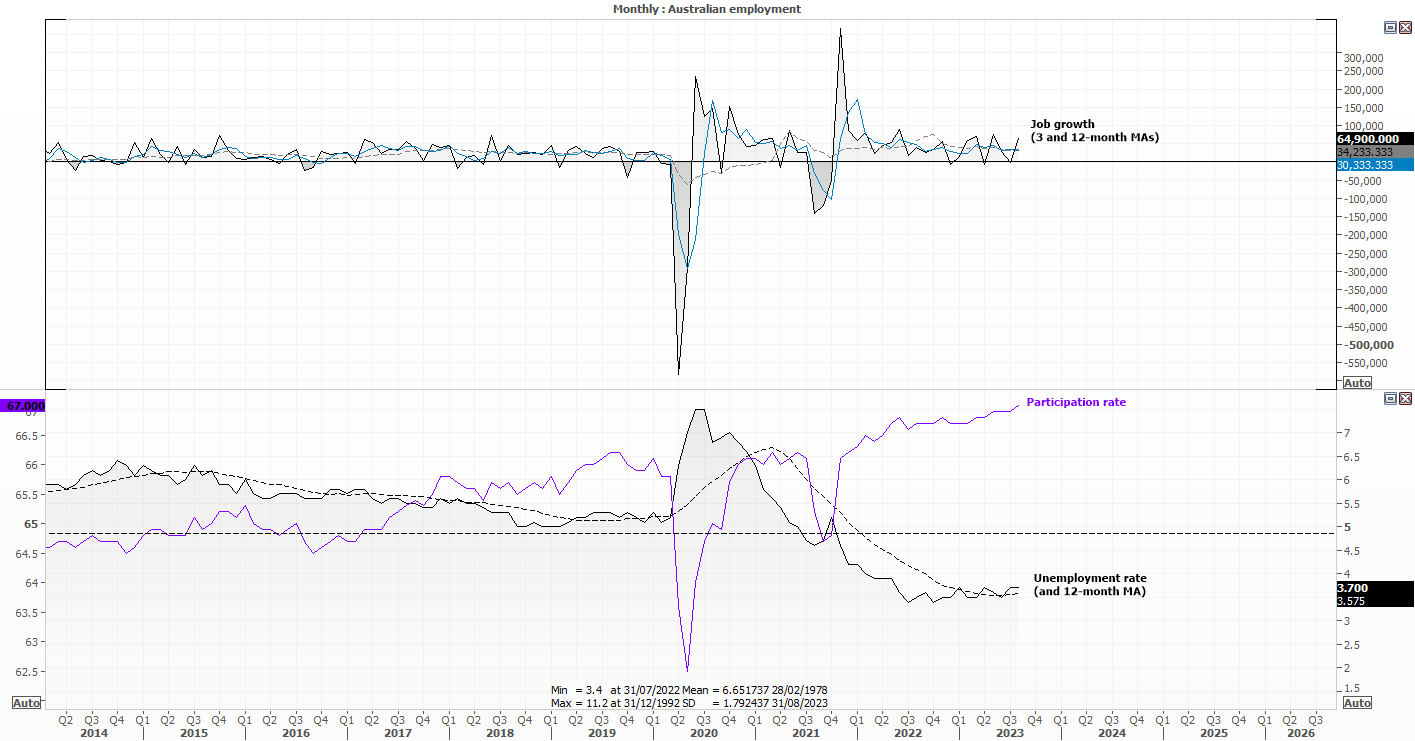

Australian employment

With the RBA remaining in data-dependant mode, employment remains a key metric for the central bank to monitor. And for those who do not want to see further rate hike, strong employment data remains an issue whilst inflation does not cool fast enough. 64.9k jobs were added last month, which nearly twice the 12-month average of 34.2k. And whilst the bulk of jobs added were part time, an unemployment rate of 3.7% and another record participation rate are hardly ringing the alarm bell for the employment situation.

And whilst we can point to other data sets such as falling household spending, cooling inflation inputs and lower job adverts to justify rates being held at 4.1%, we really need to see cracks appear in the employment situation before we can finally bury any expectations of another hike.

Perhaps we’ll see a surprise slump in jobs and rise in unemployment to appease the ‘rate cuts are next’ crowd. But the reality is that AUD/USD is in the hands of US bond yields, the dollar and the Fed until we see some large deviations from economic data.

Market to watch: AUD/USD, NZD/USD, AUD/NZD, NZD/JPY, AUD/JPY, ASX 200

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Week ahead articles

Yesterday 04:48 AM

July 19, 2024 06:20 AM

July 12, 2024 01:32 AM

July 12, 2024 01:32 AM