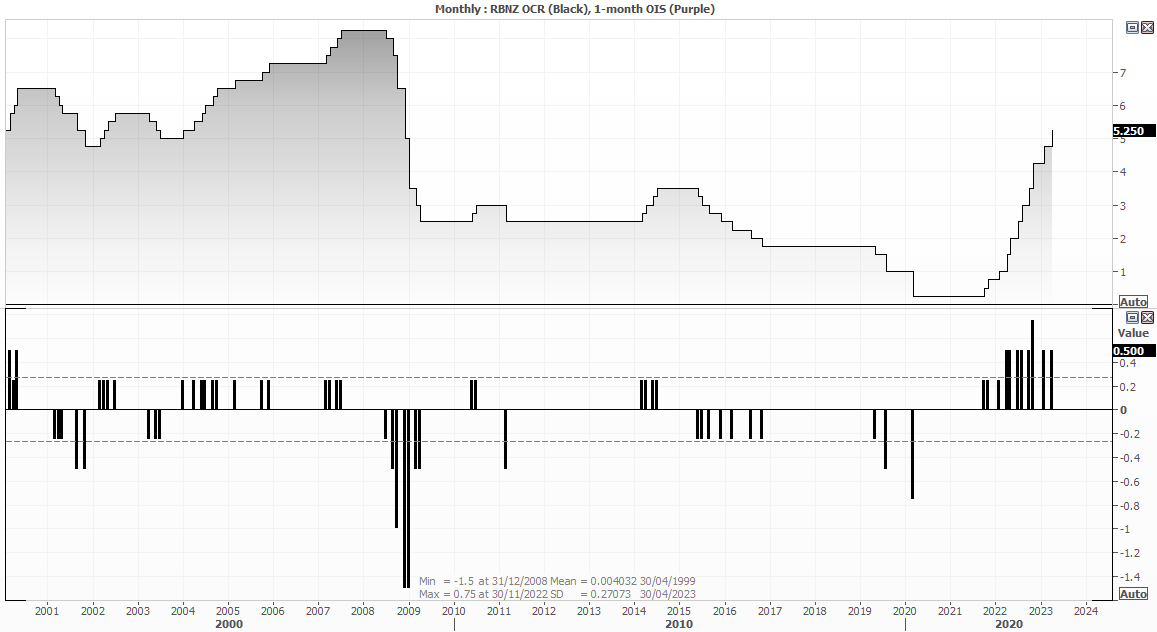

- The RBNZ hiked interest rates 50bp to 5.25%

- Economists and money markets expected a 25bp hike

- Their OCR is at its highest level since October 2008

- Their statement and minutes leans towards a hawkish hike

- Incoming data to guide future path of policy

The debate was never whether the RBNZ would pause or hike today, as the consensus was overwhelmingly for a 25bp hike. And perhaps a traditional 25bp increment could have been justified, given dire business sentiment reports , negative growth and comments from the RBNZ’s chief economist that the OCR was ‘comfortably above neutral’ since the February meeting. Clearly it was not meant to be.

Their April statement certainly leans to the hawkish side, citing ‘too high and persistent’ inflation, employment ‘beyond it maximum sustainable level’, ‘rapidly rising’ immigration, rising near-term inflation pressures alongside low mortgage arrears and debt. It’s also plausible to believe they decided to maintain the 50bp increment as they did not meet in March, which means the 100bp of hikes this year averages 25bp over the past four calendar months.

Are RBNZ at or near a terminal rate?

Given the RBNZ’s ability to dodge political pressure, focus on data and not be told what to do by markets, we cannot say with any confidence that the RBNZ are done with their tightening. We also have to wait another seven weeks until their next meeting on May 24th, which leaves plenty of data points for the RBNZ to mull over. Whilst inflation, labour costs and employment are key data sets to watch, migrant arrivals (inflationary input) an retail trade (domestic demand) are also key metrics to watch to assess their tightening trajectory.

- April 14th: Migrant arrivals

- April 20th: Consumer prices

- April 27th: NBNZ business outlook

- May 3rd: Labour costs

- May 4th: Employment

- May 10th: Retail trade

- May 12th: Migrant arrivals

- May 12th: Monetary conditions, inflation forecasts

- May 18th: Producer prices

The RBA pause their tightening cycle yesterday by holding rates at 3.6% and leaving it down to incoming data as to whether there’s more hikes coming or we’ve reached the terminal rate.

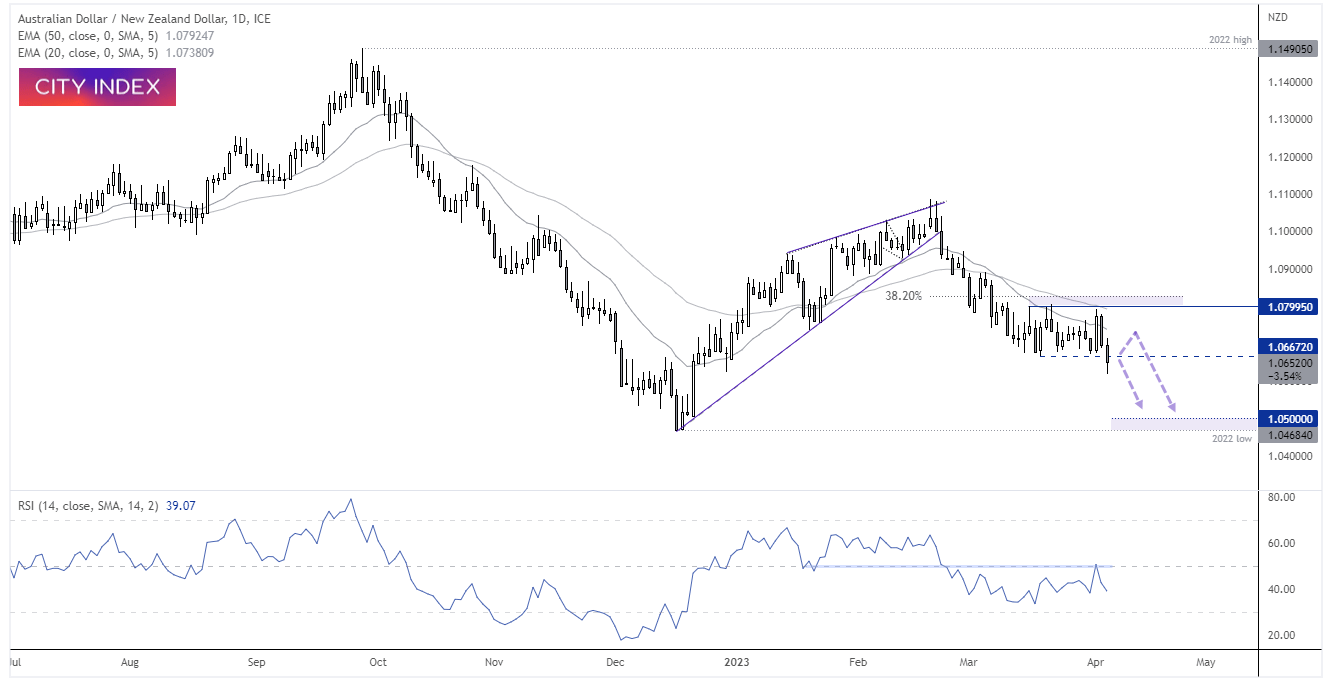

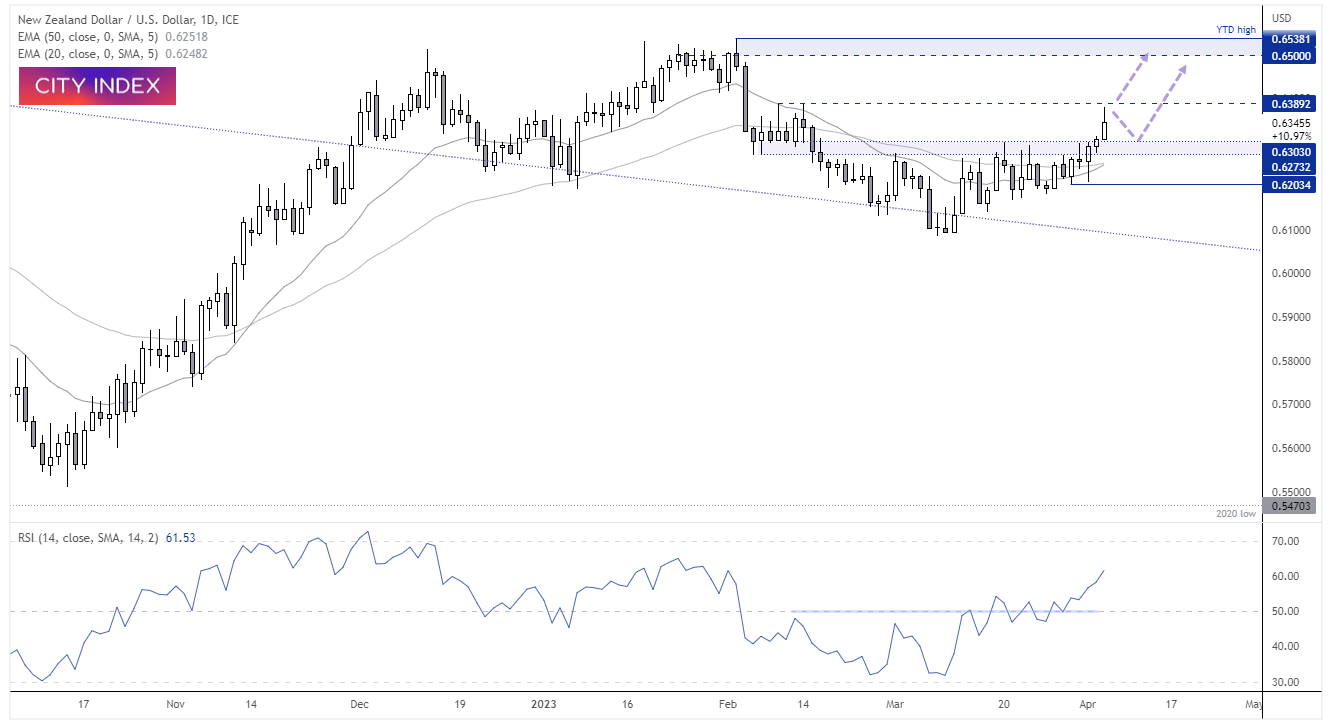

NZD pairs rallied upon the RBNZ’s announcement:

NZ pairs responded immediately by rising higher against their FX major peers, which is a classic sigh of algo-driven trading as they’re responding to the differential of the data without considering tone of the statement. Given the statement leans hawkish, NZD pairs have held on to most of their reactive gains.

AUD/NZD broke out of a bearish consolidation as momentum realigned with its bearish trend on the daily chart. The 20-and 50-day EMA’s capped as resistance during the consolidation, and prices now show the potential to move down to 1.0500 over the coming weeks, given the RBA held rates at 3.6% yesterday and are either at or very close to their terminal rate. From here, bears could seek to fade into minor rallies beneath yesterday’s high or 1.0667 resistance.

NZD/USD reached a 69-day high, although met resistance at the 0.6390 high. For its trend to continue materially higher, weak US data should feed back into the ‘US recession’ and ‘potential Fed cuts’ theme. Key data points to look out for this week include ISM services PMI, ADP employment and of course NFP data (and inflation next week). For now, bulls could seek bullish setups above or around the 0.6300 support zone with 0.6400 being an initial target, a break above which brings the 0.6500 resistance zone into focus.

Summary of the RBNZ’s April statement and minutes:

- Inflation is still too high and persistent, and employment is beyond its maximum sustainable level

- …demand continues to significantly outpace the economy’s supply capacity

- The recent severe weather events in the North Island have led to higher prices for some goods and services

- New Zealand’s economic growth is expected to slow through 2023

- This slowdown in spending growth is necessary to return inflation to target over the medium-term

- the OCR needs to be at a level that will reduce inflation and inflation expectations

- there is no material conflict between lowering inflation and maintaining financial stability in New Zealand

- Credit conditions have not tightened substantially

- Arrears on mortgages and other debts remain at low levels

- Tightening monetary policy now to reduce inflation improves the outlook for financial stability by limiting the need for even higher interest rates in future

- Near-term inflationary pressures have increased, boosted by short-term price pressures resulting from recent severe weather events and reflected in business survey indicators of costs and pricing intentions.

- Net inward migration is rising rapidly from low levels last year

- The Committee discussed 25 and 50 basis point increases at this meeting

- The Committee is expecting to see a continued slowing in domestic demand and a moderation in core inflation and inflation expectations

- The extent that domestic demand slows and core inflation and inflation expectations moderate will determine the direction of future monetary policy.

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM