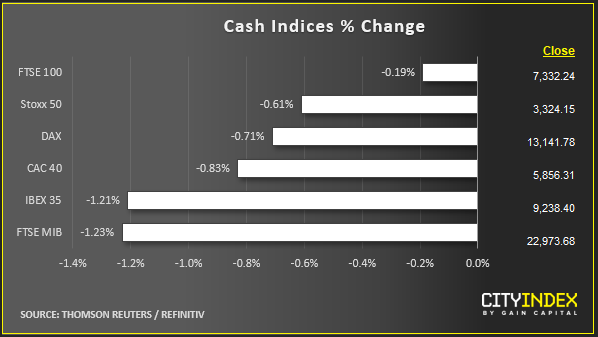

Stock market snapshot as of [2/12/2019 2:36 pm]

- Things were going quite well, then Trump tweeted. That’s a (somewhat facile) description of not just the first half of Monday’s global market proceedings, but apt for numerous sessions over the last 18 months or so. Monday may be a mild reminder that with global equities standing around cycle highs into the end of the year, whilst much remains inconclusive on trade, geopolitical and political fronts, tail risks may be higher than currently looks priced in

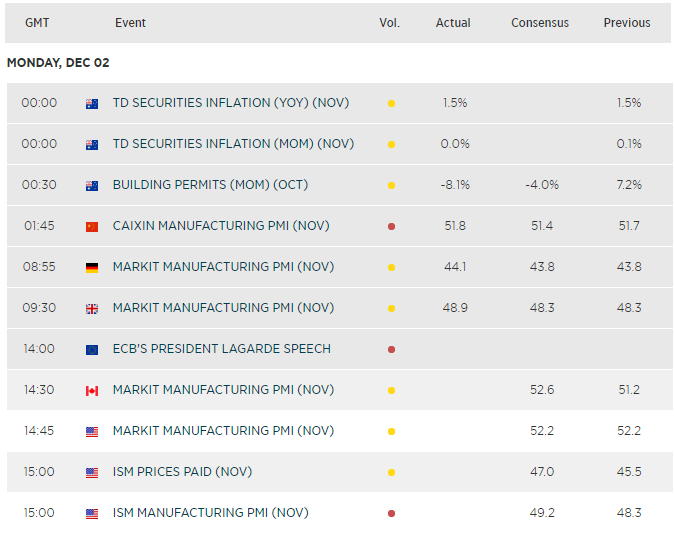

- Earlier, data from Caixin’s closely watched manufacturing PMI for China showed the sector growing for its first two-month stretch since the middle of 2018, and at the fastest rate of expansion for three years. Resilience in the world’s second-largest economy revives hopes of a base in its recent downturn. If corroborated it would have major implications for global markets into the New Year

- The official Chinese purchasing managers’ index, out over the weekend, also showed the sector returning to growth in November, boosted by a pick-up in production and new orders

- The DAX was among key European indices to benefit, albeit fleetingly

- After the U.S. President’s comments though, the German index slumped sharply, trading down 0.7% in the half hour before the U.S. cash open. Wall Street index futures retained a foothold in positive territory though were also markedly below the levels seen before the latest U.S. tariff news

Stocks/sectors on the move

- A mining and steel theme is inescapable and understandable after China's surprise manufacturing uptick and U.S. Presidential contributions. Hopes for a rebound in steel and base metal demand are being moderated after Trump tweeted that he would "restore the Tariffs on all Steel & Aluminum" from Brazil and Argentina

- BHP, Rio Tinto, Anglo American and Glencore were 0.7%-1% higher a short while ago, partly benefiting from positive brokerage commentary by RBC and Credit Suisse. These gains have been pared by Trump’s comments

- Fresnillo, the precious metals group, missed out on the day’s updraft entirely, dropping as much as 4% after lowering production guidance whilst raising capex expectations

- Newmont Gold Corp, the world's largest bullion producer by volume, also dropped production guidance whilst upping its 2020 cost outlook. It did however lower forecasts of its 2021/22 all-in sustaining costs. The trade slightly higher

- Ocado is a key UK standout. It slumps 7%-8% after surging higher by around double that rate on Friday. The online supermarket and technology platform has launched a convertible bond expiring in 2025. Institutions often hedge such bonds by shorting stock

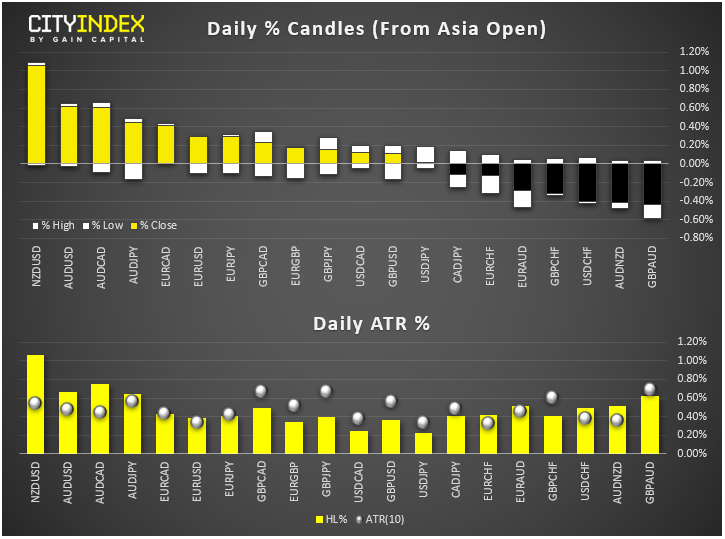

FX snapshot as of [2/12/2019 2:36 pm]

View our guide on how to interpret the FX Dashboard

FX markets including contributions from Senior Technical Analyst Fawad Razaqzada

- ‘Core’ fixed income markets have opted to discount some of Monday’s Trump factor, instead continuing to take their cue from promising global economic hints. Gold looks weak. As well as China’s manufacturing data, German factories posted a better than forecast showing in November, even if they still showed the sector was shrinking. Benchmark Eurozone bunds remain pressured as do U.S. Treasurys

- There’s little outright advantage for the dollar. DXY has slumped from 98.37 to 98.17 just now, as the quest for safety appears to ebb

- The Kiwi leads in the G10 amid a government spending pledge as commodity currencies see resilient flows in the wake of China’s indications

- The Canadian dollar is the weakest major on further signs that the BOC is preparing markets for a change of policy stance, if not outright rate policy changes, as early as its rate announcement scheduled for Wednesday

- The euro remains in familiar ranges albeit the single currency enjoys another positive session above $1.10. The move helps affirm last week’s 1.09812 intermediate low

- Elsewhere, the lira was steady as Turkey’s economy continued its gradual recovery from recession in the third quarter. GDP expanded by 0.9% following a contraction of 1.6% in the previous quarter, though the Q3 rise was lower than consensus

Upcoming economic highlights

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Bonds articles

July 1, 2024 11:04 PM

May 30, 2024 06:11 AM

May 3, 2024 01:00 AM