- EUR/USD analysis: Powell pushes back against dovish repricing

- GBP/USD analysis: Cable finds little love from slightly stronger UK data

- Week ahead: CPI and retail sales from both UK and US puts GBP/USD into focus

Welcome to another edition of Forex Friday.

Following Thursday’s bullish reversal in the dollar on the back of a soft 30-year Treasury auction and hawkish comments by Powell, the key question is whether those gains will last. I don’t think the Fed Chair said anything out of the ordinary, although that’s not to say the dollar won’t necessarily rise further. I mean, you wouldn’t expect him to turn decisively dovish just on the back of a couple of weaker data points. Equally, with inflation remaining above-forecast for the past couple of months, he has to address the risks of it remaining elevated for longer, and the central bank’s readiness to act if required. So far, bond yields have remained supported while US index futures have drifter a bit further lower after Thursday’s bearish reversal. The dollar was trading mixed at the time of writing. I think the market’s focus will turn back to data quickly. We have the UoM’s consumer sentiment and inflation expectations surveys coming up later in the afternoon, ahead of inflation and retail sales data next week.

Powell pushes back against dovish repricing

On Thursday we saw a rather soft 30-year Treasury auction while hawkish comments by Powell both helped to cause a rebound in US bond yields, which underpinned the dollar and undermined stocks. Volatility in the rates market will continue to drive markets on Friday, as we await fresh market-moving US data. A gauge of consumer sentiment from

Jerome Powell, the Chair of the Federal Reserve, expressed the intention to proceed cautiously while being ready to implement policy adjustments to curb inflation if necessary. He said: “If it becomes appropriate to tighten policy further, we will not hesitate to do so,” in remarks at an International Monetary Fund conference in Washington on Thursday. Powell added that the Fed will “continue to move carefully, however, allowing us to address both the risk of being misled by a few good months of data, and the risk of over-tightening.” Following his sterner remarks, we saw the dollar come back noticeably as stocks and bonds have turned lower, driving the two-year Treasury yields to above 5%.

Let’s see if those moves will be sustained during Friday’s session, before the focus turns to inflation and retail sales data in the week ahead. The UoM’s consumer sentiment survey is seen changing very little from the previous month’s reading of 63.8, while the 1-year inflation expectations is also expected to be around the same sort of level as previous month’s 4.2%, a five-month high.

Before we turn our focus on the GBP/USD pair which is likely to be in sharp focus next, let’s have a quick look at the EUR/USD first.

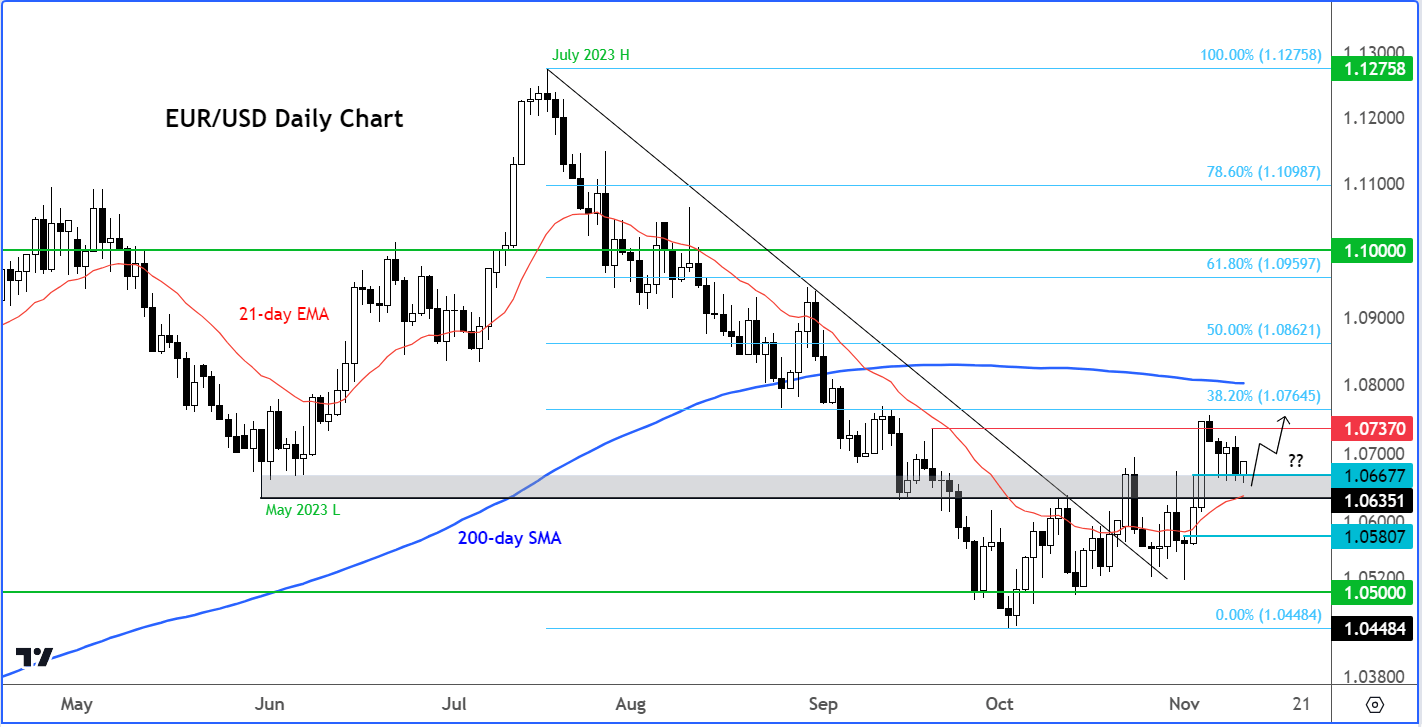

EUR/USD analysis: Euro defends key support

Despite the dollar recovery on Thursday, the euro was looking to bounce back Friday. It was holding key support around the shaded region on my chart of 1.0635 to 1.0667, the base of the previous breakout. The short-term outlook remains bullish given the interim higher highs and higher lows we have seen of late. The fact that price is also holding above the 21-day exponential means the short-term trend is no longer bearish.

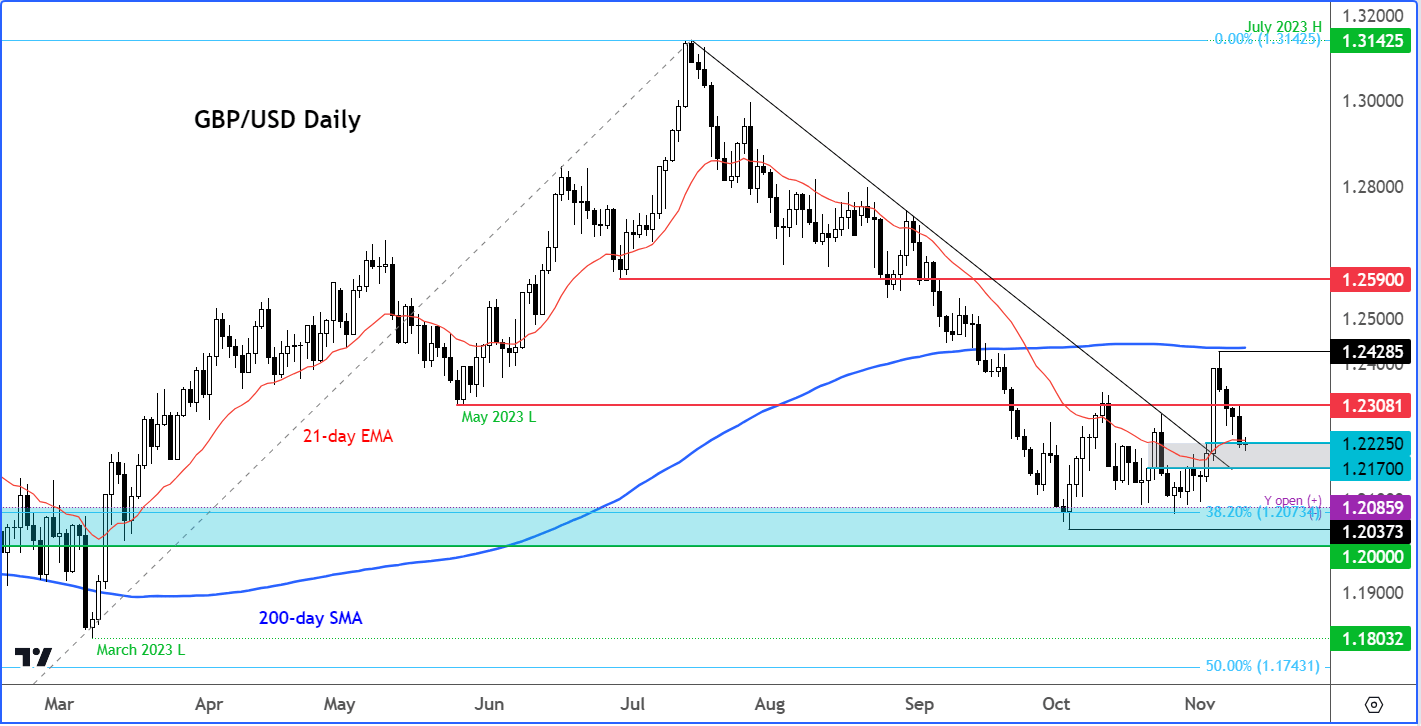

GBP/USD analysis: Cable finds little love from slightly stronger UK data

This morning’s mostly stronger UK data dump offered limited support for the GBP/USD, which was testing support around the 1.22 handle following its Powell-inspired sell-off on Thursday.

Official figures pointed to a stagnating economy, although one that performed better than hoped in the third quarter. While output failed to grow between July to September, this was still better than a drop of 0.1% economists had expected. A stronger performance in September meant the economy would avoid negative growth in Q3, with output rising by 0.2% on the month instead of zero expected. Construction output was a bright spot, which rose 0.4% month-on-month instead of falling by 0.5%, while industrial production was flat compared to a small fall expected.

Nevertheless, the Bank of England is not forecasting any speedy recovery in growth. High interest rates to tackle stubborn inflation means mortgage payments are going to remain high and for some unaffordable, unfortunately leading to many delinquencies. The BoE thinks that the UK’s economic growth will be zero until 2025, albeit it is expected to avoid falling into a technical recession of two consecutive quarters of negative output.

Week ahead: CPI and retail sales from both UK and US puts GBP/USD into focus

The week ahead is set to be a busier one, especially for the GBP/USD pair. The cable will remain in focus with key inflation and retail sales data from both sides of the pond to come in addition to UK wages figures.

US CPI

Tuesday, November 14

For two consecutive months, US inflation has surprised to the upside. In September, annual CPI remained unchanged at 3.7%, defying market expectations of a slight decrease following an even larger surprise the month before. Perhaps this is why the Fed Chair was more cautious when he warned of tightening monetary policy further if needed, with his comments providing the dollar and bond yields fresh bullish momentum. However, if we see a surprising weaker CPI print this time, then it will boost the “peak interest rates” narrative again and potentially hurt the dollar.

UK CPI

Wednesday, November 15

UK’s inflation rate has been very slow to come down, keeping policymakers at the BoE on their toes. While no further rate increases are likely, BoE Governor Andrew Bailey has said it is “too early to be talking about cutting rates”. Those talks could be pushed further out if CPI turns out to be stronger than expected.

Next week’s other key data highlights

These include UK wages and jobs data on Tuesday; US retail sales, PPI and Empire State Manufacturing Index all on Wednesday, and US industrial production; jobless claims and Philly Fed Manufacturing Index on Thursday, and UK retail sales on Friday.

We will also Australian employment data on Thursday, but more importantly a Chinese data dump on Wednesday. As well as industrial production, we will have retail sales data to look forward to in the early hours of Wednesday from the world’s second largest economy. Recent Chinese macro pointers have shown some improvement. We will need to see more evidence of a turnaround for yuan, local stocks and some base metals prices to recover more meaningfully.

Video: EUR/USD analysis

Source for charts used in this article: TradingView.com

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Forex Friday articles

July 19, 2024 01:00 PM

July 5, 2024 04:26 PM

June 21, 2024 12:02 PM

May 31, 2024 11:00 AM