Fed fund futures have certainly been all over the shop in the past two weeks, with expectations of a ‘sure given’ 50bp hike slashed to a pause and even a cut, before settling on a 25bp hike by yesterday’s close. We’re usually accustomed to is the Fed having guided market expectations ahead of the blackout period, but that has certainly not been the case this time around. So this meeting stands out as it is the first in a long time that opinions are so varied of how it could play out. But here are my thoughts.

The Fed are likely to hike by 25bp

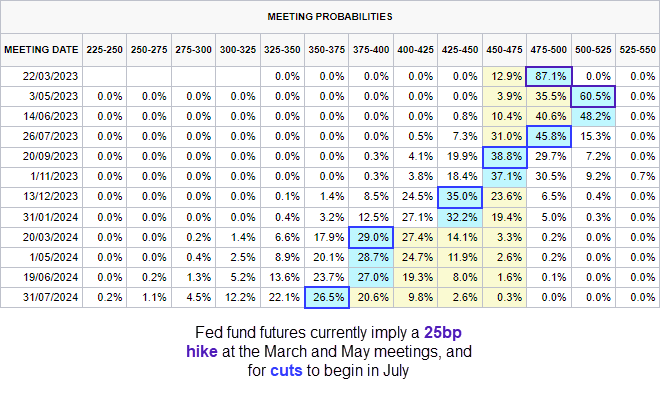

Fed fund futures (FFF) suggest an 87.1% chance of 25bp hike today - and I agree with that part. A pause could do more damage than good as it would imply the Fed have gone too far and lost control, whilst a 50bp hike is too aggressive given the recent market turbulence. And let’s not forget how hawkish Jerome Powell was before SVB imploded, so the 2x 25bp hikes and a terminal rate of 5.25% the FFF curve implies seems feasible.

But what if the Fed Funds Futures curve is too dovish?

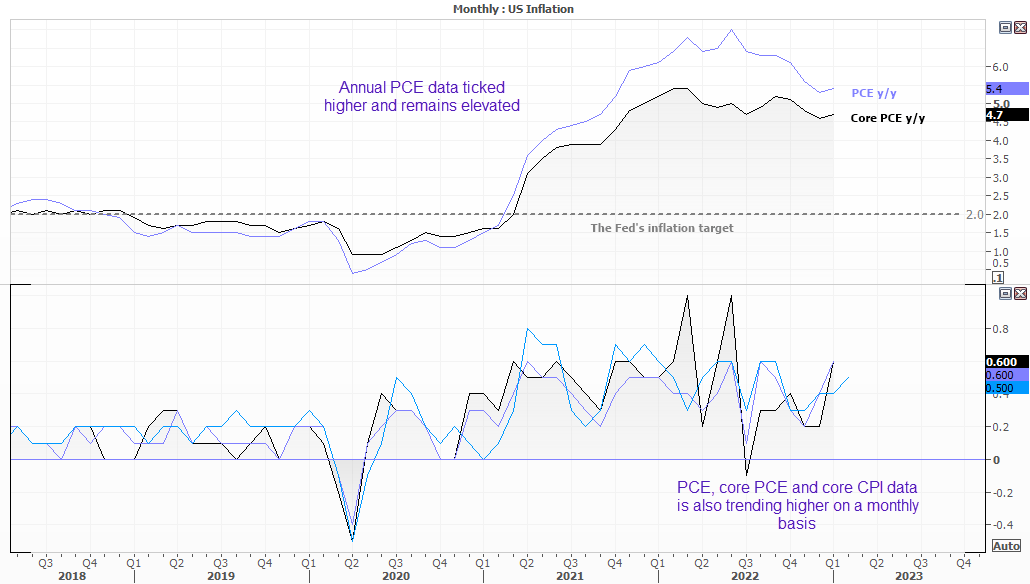

However, money markets are trying to price in four 25bp cuts beginning in July, and this is where I begin to doubt the curve. The Fed have coordinated with other central banks and government agencies to put out any fires, inflation remains 2-3x the Fed’s target, three measures of inflation are trending higher on the monthly basis and employment remains tight.

Even if market pricing is correct today, are the Fed seriously going to announce a dovish pivot or pause? I very much doubt it, which leads me to suspect the FFF curve is too dovish, in turn leaving the potential for a hawkish surprise relative to expectations.

And that could result with a steepening of the FFF curve and a higher US dollar. At best the Fed may switch to a ‘data dependent’ view on a per-meeting basis, but with data remaining ‘hike friendly’ this rings more hawkish to my hears than the current dovish market pricing suggests. And with the US dollar currently around 5-week lows, that could also make long USD the asymmetric trade for the rest of the week.

What we’re looking out for at the March FOMC meeting:

Unless the Fed surprise with a pause of 50bp hike, then the anticipated 25bp is not likely to move markets.

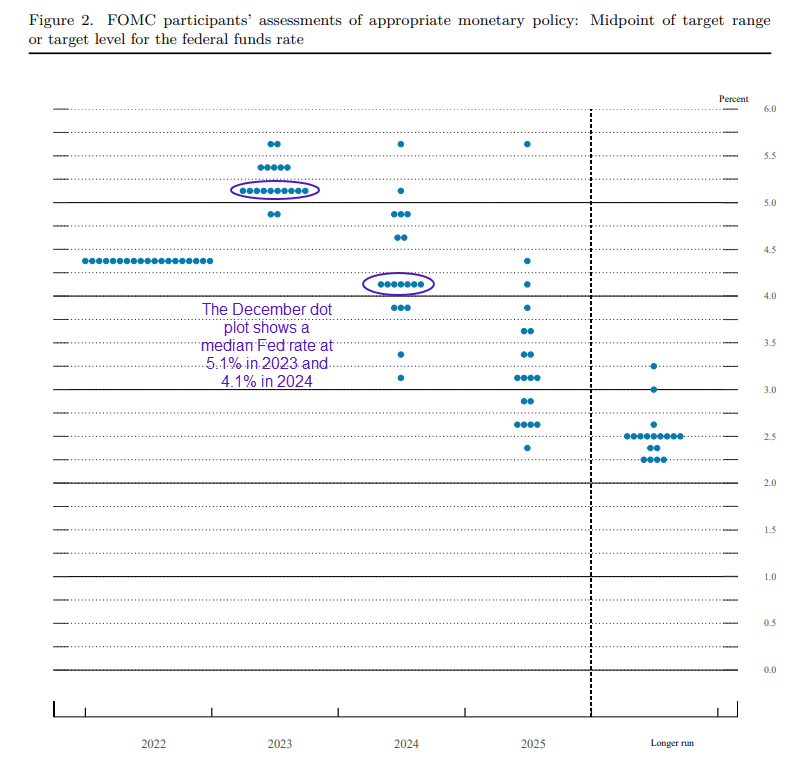

The dot plot will grab my immediate attention, because it needs to be revised lower to justify current market pricing. The December dot plot showed a median Fed rate at 5.1% in 2023 and 4.1% in 2024, and dollar bears need to see this revised lower to justify their current bets.

I’ll concede that the dot plot is less likely to be revised higher given the complicated backdrop, but I doubt it will reflect four cuts this year.

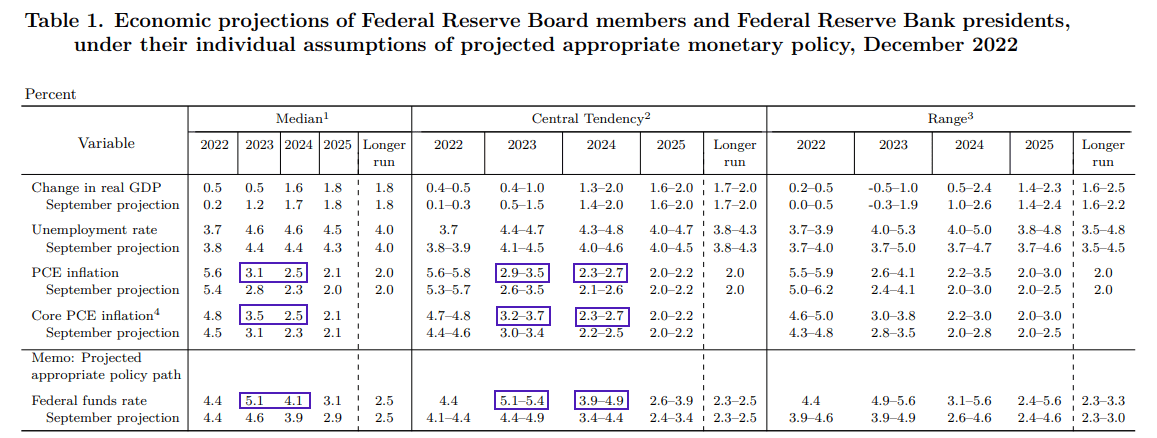

Any changes to the economic forecasts also have the potential to sway sentiment. There’s a reasonable chance we could see inflation revised lower, but again it depends by how much as to whether the dollar has further downside, or is nearing a inflection point. If the median or central tendency is not revised lower, a key argument for dollar bears is removed which leaves the dollar ripe for a short-covering rally.

The press conference could be the icing on the cake, as it is an opportunity for Jerome Powell to finetune the message and reshape market expectations. It is not uncommon to see markets reverse their direction at the press conference, and a key thing to look out for is how his tone compares to his recent testimony, which was very hawkish indeed. He will also field questions, which means he will be off script – and may even slip up along the way. But this part certainly has the potential for the most volatility, and for trends to develop into the back of the week.

Beyond that, don’t be surprised to see Fed members come out in force and read from the same script, if the overall market reaction to the meeting did not go down as the Fed desired. Either way, we could be in for quite a ride for the next few days.

How markets could react:

- If we are correct in out thinking, the US dollar is oversold and that leaves plenty of opportunities for currency traders. Aussie bears could pounce on the theme of dovish RBA minutes and a less-dovish than expected Fed and drive AUD/USD back to the March lows. USD/JPY may have seen its low of the month at 130.57, and make easy work of a break above 135.20.

- EUR/USD is sat at a 5-week high, but I’d expect it to be knocked off of its perch and break convincingly below 1.0700

- Gold could head for $1900, although with investors still on edge and looking our for the next bogeyman, its safe-haven appeal could see it support above this key level.

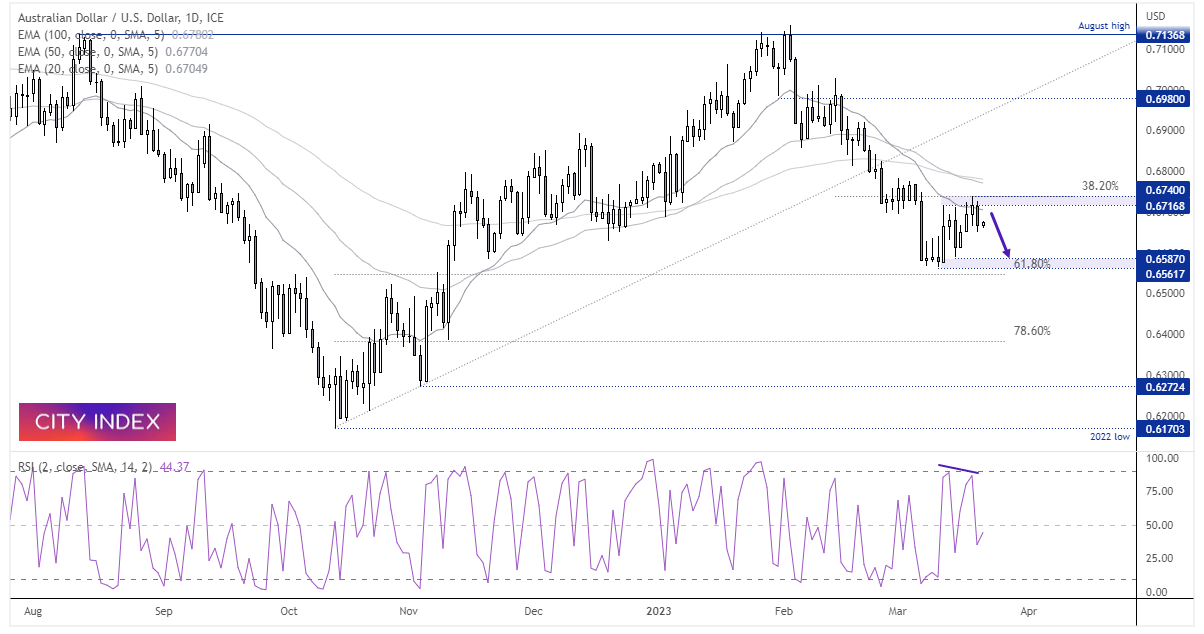

AUD/USD daily chart:

The Aussie has reverted higher in three waves as part of a potential ABC correction. A 38.2% Fibonacci ratio has capped as resistance, along with the 20-day EMA. A bearish engulfing candle also formed yesterday to suggest the swing high is in place. On the assumption that the Fed won’t be as dovish as many hope, we prefer to fade into rallies within yesterday’s range and benefit from the double whammy of dovish RBA minutes and a more-hawkish than expected Fed.

Of course, a clear risk is that the Fed are indeed dovish and the Aussie rips higher. In which case, the bias remains bearish beneath 0.6450 and for a move back to the March lows.

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Trade Ideas articles

Yesterday 09:35 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

July 25, 2024 05:30 PM