US futures

Dow futures +0.25% at 33642

S&P futures +0.16% at 4344

Nasdaq futures +0.09% at 15125

In Europe

FTSE -0.5% at 7610

Dax +1.06% at 15263

- US Q3 banks earnings are encouraging

- Caution after stronger US inflation data

- Microsoft-Activision deal approved by UK authorities

- Oil jumps 4% and set for strong weekly gains

Banks beat earnings estimates

US stocks are pointing to a higher open as investors mull over better-than-expected bank earnings and look ahead to Michigan consumer sentiment data later in the day.

Banks' results have started the earning season off on the front foot, However, there are still signs of caution amongst the investors. The three major indices fell for the first time in five days on Thursday after US inflation data came in stronger than expected and following weak demand in an auction of 30-year US bonds.

Still, treasury yields are easing on Friday after a spike on Thursday, which could offer some support to the equity market.

Attention will be on U.S. consumer sentiment, which is expected to tick lower 67.2 in October, down from 68.1. Strong consumer sentiment tends to go hand in hand with higher consumer spending, adding to inflationary pressures and supporting a hawkish Fed. A weaker report, therefore, could be considered a positive for U.S. stocks.

Attention will also remain on the conflict in the Middle East as Israel has called for civilians of Gaza City, which is over a million people, to relocate within 24 hours ahead of an expected ground invasion. Oil prices have jumped almost 4% lifting oil majors.

Corporate news

JP Morgan is rising after posting Q3 profits thanks to higher interest rates boosting income from loans. EPS was $4.33, up from $3.12 a year earlier.

Wells Fargo is also heading higher after Q3 profits beat estimates, and the lender raised interest income forecasts. Wells Fargo now expects 2023 NII to be 16% higher than a year earlier, up from a 14% increase. NII rose 8% to $13.1 billion in Q3.

Microsoft's $69 billion deal to buy Activision Blizzard has finally been approved by the UK's competition and markets authority. The deal, first proposed in January 2022, has faced regulatory challenges in the US, Europe on the UK. However, this was the last major hurdle for the deals to close.

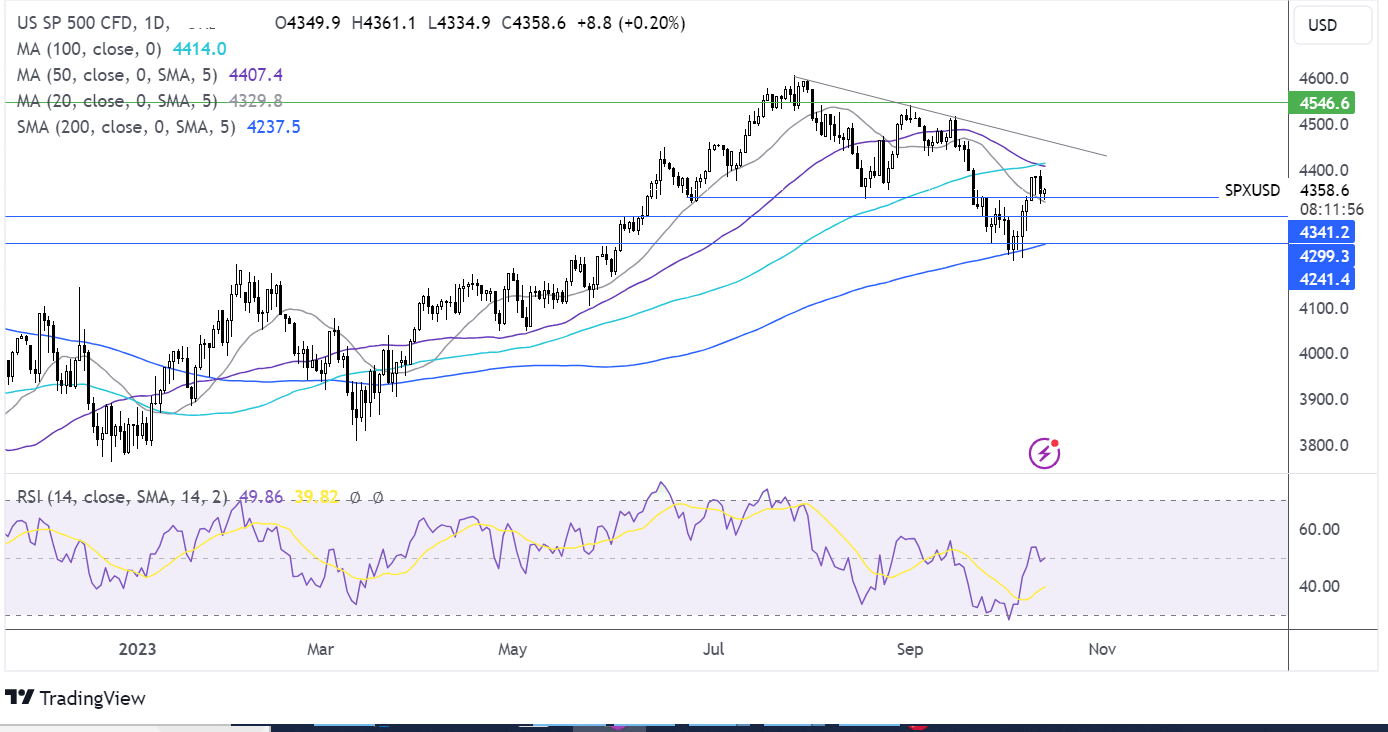

S&P500 forecast – technical analysis.

The S&P500 ran into resistance at 4400 the 50 sma yesterday and has dropped to test support at 4335, the August low and the 20 sma. Sellers would need to take out this level to extend losses towards the 4300 round number and the 200 sma at 4240, the September low. Should buyers defend 4335 successfully, bulls would need to rise above 4400 the weekly high, to extend gains.

FX markets –USD rises, EUR falls

The USD is inching higher, adding the gains in the previous session after the hotter-than-expected US inflation data supported the view that the Federal Reserve could hike rates again. The greenback is on track to rise against the box code of currencies for the 12th time in 13 weeks.

EUR/USD is Inching lower after losses yesterday and is on track to book a loss across the week. Eurozone industrial production fell 5.1%YoY in August, well below the 3.5% forecast. Meanwhile, inflation in the region ticked higher with French inflation at 4.9% and Spanish inflation rising to 3.3%. ECB president Christine Lagarde is due to speak this afternoon.

GBP/USD is edging lower after steep losses yesterday and is set to fall across the week after lackluster UK GDP data and hotter-than-forecast US inflation. The risk-off mood is also hurting demand for sterling. Looking ahead, next week sees plenty of UK data, which could provide further clues over the Bank of England's next move. UK unemployment inflation and retail sales figures are due in the coming week.

EUR/USD -0.07% at 1.0524

GBP/USD -0.02% at 1.2180

Oil jumps 4% and is set to rise across the week

Oil prices are trading over 4% higher at the end of a volatile week as the US ramped up its sanctions against Russian crude exports, raising concerns over supply in an already tight market.

The US imposed sanctions on owners of tankers carrying Russian oil priced above the G7 price cap of $60 a barrel. Russia is a major oil producer and exporter and tighter scrutiny of its shipments could impact supply.

Concerns over supply are putting Brent on track for gains of around 5% and 4% for WTI, with a large part of those gains being driven by concerns over potential disruption to Middle Eastern exports after Hamas attacked Israel last weekend. There has been no sign of leading oil-producing countries becoming directly involved in the military conflict. However, a geopolitical risk premium is keeping oil prices supported well ahead of an expected ground attack in the coming 24 hours.

Reports from OPEC that crude stockpiles are expected to rise by three million barrels per day this quarter are also keeping the price of oil elevated. OPEC kept its forecast for growth in global oil demand unchanged citing a resilient global economy and further demand gains expected in China.

WTI crude trades +4% at $84.90

Brent trades +4.06% at $88.40

Looking ahead

15:00 Michigan Consumer Sentiment

Latest market news

Today 12:16 PM

Today 08:17 AM

Latest US Open articles

Yesterday 01:18 PM

April 30, 2024 01:24 PM

April 29, 2024 01:39 PM