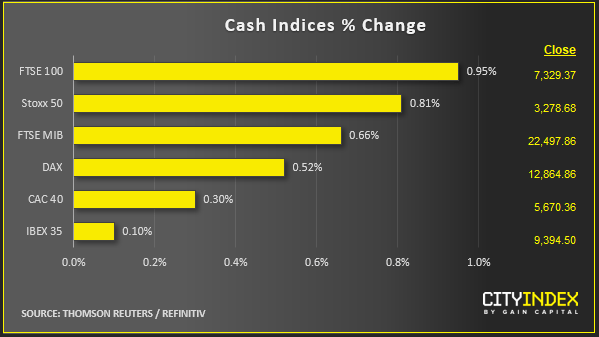

Stock market snapshot as of [24/10/2019 3:43 PM]

- Europe’s automobile sector drives an extension of the region’s equity market advance as stock indices trade close not far off session highs. Daimler looks to have powered through Q3 on the back of Mercedes volumes.

- Sentiment is bolstered despite mixed PMI readings. Periphery bonds spreads tighten marginally versus core, backing the view that we’re looking at a risk-on phase, though not giving much steer as to its strength. Gilts trade sideways within previous session’s range, in step with an increasingly rangebound pound

- Sterling traders are trying to square an opposition Labour Party that says it will be "pragmatic" on Brexit and signs that Prime Minister Boris Johnson hasn’t given up on the chance of getting his deal through the House quickly. Meanwhile, there is no doubt that the EU is keeping Boris Johnson waiting. He’s still waiting for a response to his letter seeking a Brexit delay till 31st January. The EU’s Parliament recommends accepting the request, so perhaps official acceptance is now a formality, that may be concluded as early as Thursday. Note however, that the forum doesn’t have a formal say. It’s emerged that the neither the Withdrawal agreement, nor a debate over a proposed election, were included in Parliamentary business announced for next week

- Elsewhere, SEK spiked higher as the Riksbank held rates and indicated a December move higher

- The euro dipped ahead of Mario Draghi’s final press conference as ECB president. It then stabilised as he began to speak. Draghi’s impact on the single market’s currency is remaining consistent, in a fashion, right up till his exit from the top chair. As expected, both the Q&A and governing council meeting were short of policy action or guidance. Instead they were heavy on implied imperatives for the new chief, Christine Lagarde. One repeat question was whether the central bank would soon run into self-imposed limits. ‘The ECB doesn't foresee hitting them anytime soon.’

Stocks/sectors on the move

- High profile U.S. earnings are sharply in focus. Twitter opened around 20% lower after missing revenue and EPS estimates though it posted higher than forecast active user growth. TWTR euphemistically referred to a new "revenue product" problem that cut sales by 3 percentage points or more. The issues relate to a ‘bug’ that allowed access to certain user data without permission. Ceasing to utilise the data is forecast to keep dragging ad sales into next year

- Tesla’s surge in the other direction by a similar magnitude (about +17% just now) helps anchor Nasdaq indices. TSLA brought positive drama to Q3 earnings when none was expected given the EV leader pre-reported deliveries weeks ago. A surprise profit of $1.86/share when a $0.24 loss was expected was key. Though this came with the group’s first revenue fall in 7 years, gross margin expansion on GAAP basis also crushed estimates, rising to 18.9% vs. Wall Street’s 15.1% view

- Microsoft brought less drama despite a stonking first 2020 quarter. The flagship cloud business grew at a 59% pace year-to-year, lifting the broader Intelligent Cloud segment 22%, yet the shares barely moved in Wednesday’s after-hours market. MSFT rises about 2% on Thursday, to account for top and bottom-line beats, and a strong outlook. What was missing was an element of surprise. Plus, Azure, the centre piece enterprise cloud brand actually missed the most optimistic forecasts

- Europe’s day in earnings has been as frenetic as Wall Street’s last 24 hours, with Nokia, Daimler (DAI), AstraZeneca (AZN), BASF, among the largest firms reporting. Shares in the telecom equipment maker (NOKIA) stand out with a 23% collapse after a sharp outlook cut. DAI is rewarded for years of investment in Mercedes, which drove volume growth and higher guidance; lifting the shares 3%. AZN was up 5% as emerging market growth turned cash generation up a gear. BASF shares added 2.6%, shrugging off trade-war cautions with guidance intact

- Earnings success stories offer an actual and sentiment-based lift to indices, keeping the STOXX 600 gauge on its path back to year highs

- The global earnings frenzy will continue later with Intel, PayPal, Amazon and others starring

- A speech on China by U.S. Vice President Mike Pence will also be watched, amid expectations that it could reignite trade tensions

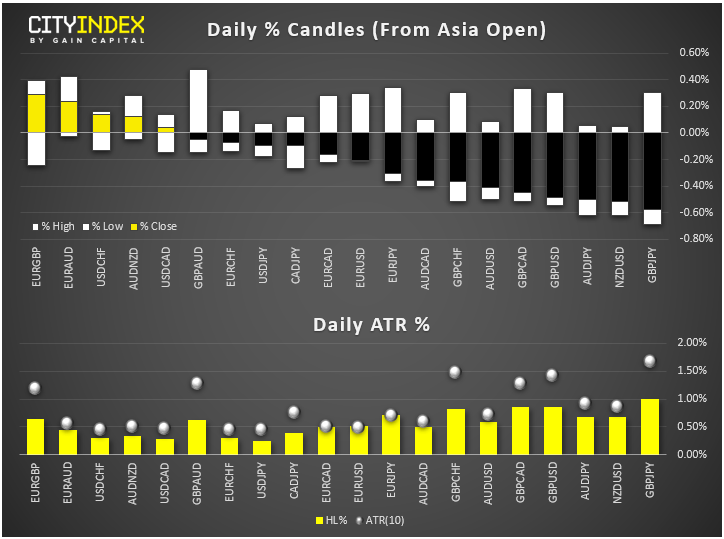

FX snapshot as of [24/10/2019 3:25 PM]

FX markets

- Uncertainty and has finally called a halt to sterling’s Brexit deal-hopes rally, with a definitive looking break below $1.288 support gathering pace

- The euro also fails to sustain an earlier advance on pleasantly surprising French data, after getting its typical short-lived fillip from ECB noise. Having peaked early at $1.162, it was last at $1.114

- Sweden’s Krona was an earlier G-10 leader as the Riksbank stood pat, leaving EUR/SEK at a one-month low of 10.656

- Weakening regional manufacturing weighs both Aussie and Kiwi

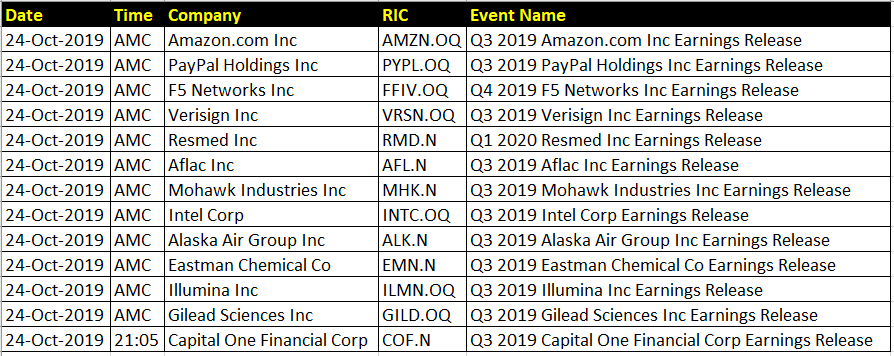

Upcoming corporate highlights

AMC: after market close

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Bonds articles

July 1, 2024 11:04 PM

May 30, 2024 06:11 AM

May 3, 2024 01:00 AM