King Dollar set for a rebound

The dollar staged a broad-based rally on Thursday to make back some of the losses it had suffered earlier in the week which had been […]

The dollar staged a broad-based rally on Thursday to make back some of the losses it had suffered earlier in the week which had been […]

The dollar staged a broad-based rally on Thursday to make back some of the losses it had suffered earlier in the week which had been on the back of a poor ISM services PMI reading and last week’s disappointing jobs report. Some improvement in US data was observed in the second half of the week however as job openings surged to a record high in July and the weekly applications for unemployment claims dropped more sharply than had been expected.

But I think that the main reason for the dollar’s bounce on Thursday is this: the inaction by the European Central Bank and their refusal to discuss the prospects of extending the bond purchasing programme beyond March 2017. Although this sounds counterintuitive as it should be EUR/USD positive – and indeed the initial reaction was – I think that the bank’s slightly hawkish tone has raised the odds for a US rate rise before the end of the year as the Fed’s concerns about a significant appreciation of the dollar versus the euro should now ease slightly in the view that the ECB will probably not loosen its policy again (unless the economic situation in the Eurozone turns sour once more). And let’s not forget, the Fed still remains the only major central bank looking to tighten its policy, while with regards to the ECB, no one should have been surprised by their decision since the Eurozone economy did not really deteriorate since the central bank’s last meeting on 21st July. The fundamental view of a depreciating EUR/USD exchange rate has therefore not changed, in my view.

Consequently, I wouldn’t be surprised to see the EUR/USD ease back once again, which should apply some upward pressure on the Dollar Index, especially since there is no significant data from either the Eurozone or US scheduled until mid-next week.

Next week’s key Eurozone data is the German ZEW Economic Sentiment which will be released on Tuesday. From the US, Thursday is going to be a very busy day as we will have retail sales, jobless claims, producer price index, industrial production, capacity utilization rate and Philly Fed and Empire State manufacturing indices. But perhaps more important for the markets will be Friday when the latest Consumer Price Index (CPI) measure of inflation and a closely-watched consumer sentiment survey are released.

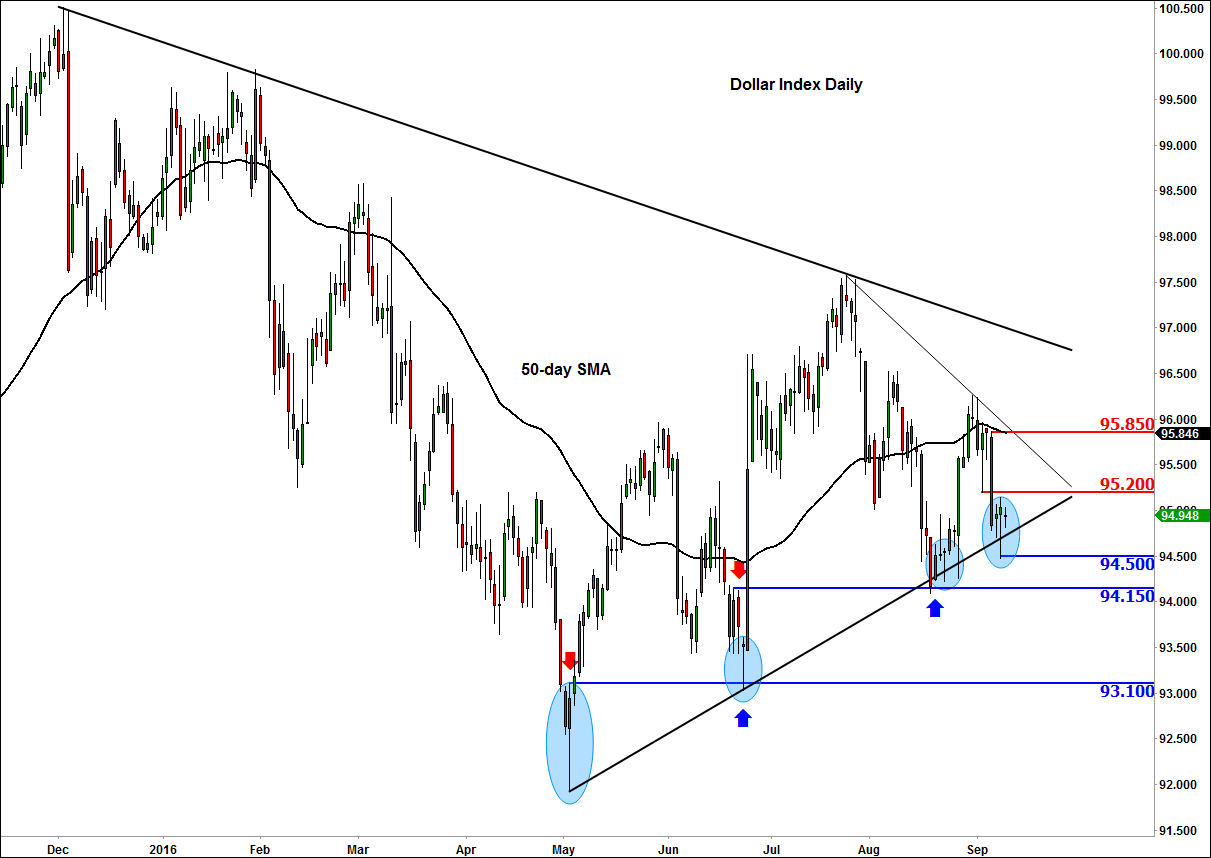

Technical outlook: Dollar Index

From a technical perspective, the Dollar Index’s rebound on Thursday should not have come as a major surprise. As we have previously indicated, the DXY has been finding support repeatedly from its rising trend line. And Thursday was no different: another breakout attempt failed miserably here, resulting in the creation of another hammer-like candlestick pattern on the daily chart. If the past price action is anything to go by, the dollar should now extend its gains. The index faces intermediate resistance at 95.20, a level which was previously support. If it breaks above this level then the next stop could well be at around 95.85 which corresponds with the 50-day moving average and a short-term bearish trend line. The more significant bearish trend line is further higher at around 96.75.

All that being said however, a potential break of the bullish trend line and all bets will be off. In this potential scenario, the dollar could fall significantly as not only will it prove the dollar bulls wrong, it will probably also encourage the bears to express their views more boldly.