It could be an interesting week for the Australian dollar if caught between the crossfire of the RBNZ meeting, Fed talk and US inflation data. We also have an Australian inflation report to throw into the mix for good measure. On one hand the RBNZ may provide a more hawkish statement given the pickup of economic data and underlying inflationary forces, and on the other traders also have to keep an eye on a key US inflation report and several Fed members hitting the wires.

Economic events for AUD/USD traders

|

Date |

AEDT (GMT +11) |

Event |

|

Wednesday, Feb 28 |

11:30 |

Construction Work Done, Australia, Preliminary |

|

- |

11:30 |

Annual weight update of the CPI and Living Cost Indexes |

|

- |

11:30 |

Monthly Consumer Price Index indicator |

|

- |

12:00 |

RBNZ interest rate decision, monetary policy statement |

|

- |

13:00 |

RBNZ press conference |

|

Thursday, Feb 29 |

00:30 |

US GDP, PCE prices, consumer spending |

|

- |

11:30 |

Private New Capital Expenditure and Expected Expenditure |

|

- |

11:30 |

Retail Trade |

|

Friday, March 1 |

00:30 |

US PCE price index, jobless claims |

|

- |

02:50 |

FOMC member Bostic speaks |

|

- |

05:15 |

FOMC member Mester speaks |

|

- |

09:00 |

Fed Goolsbee speaks |

|

- |

09:00 |

Australian manufacturing PMI (final?) |

|

- |

11:05 |

RBNZ governor Orr speaks |

|

- |

12:10 |

FOMC member Williams speaks |

|

- |

12:30 |

Chinese PMIs (manufacturing, services, composite – NBS) |

|

- |

12:45 |

China manufacturing PMI (Caixin) |

|

Saturday, March 2 |

01:45 |

US manufacturing PMI (S&P Global) |

|

- |

02:00 |

US manufacturing PMI (ISM) |

When there are so many competing forces, the odds of choppy trading conditions, false moves and sharp reversals tend to increase. Unless the incoming headlines are stacked in such a way that favours a trend based on a divergent theme between those competing forces. Yet with expectations of the RBNZ upping their hawkish undertones, Fed members pushing back on rate cuts and the potential for a firmer US PCE inflation report, we likely require a soft set of CPI figures for Australia for it to provide a convincingly bearish as it limps towards the weekend.

Wednesday could be a volatility hotspot for AUD/USD

Australian inflation data and the RBNZ’s cash-rate decision will be released within 30 minutes of each other on Wednesday, with an RBNZ press conference one hour later.

What to look out for on Wednesday:

- Whether the monthly AU CPI prints will continue to soften (dovish implications for the RBA)

- If service-related components are given a greater weighing in the CPI basket (hawkish implications for the RBA)

- Whether the RBNZ reintroduce a tightening bias in their statement or press conference

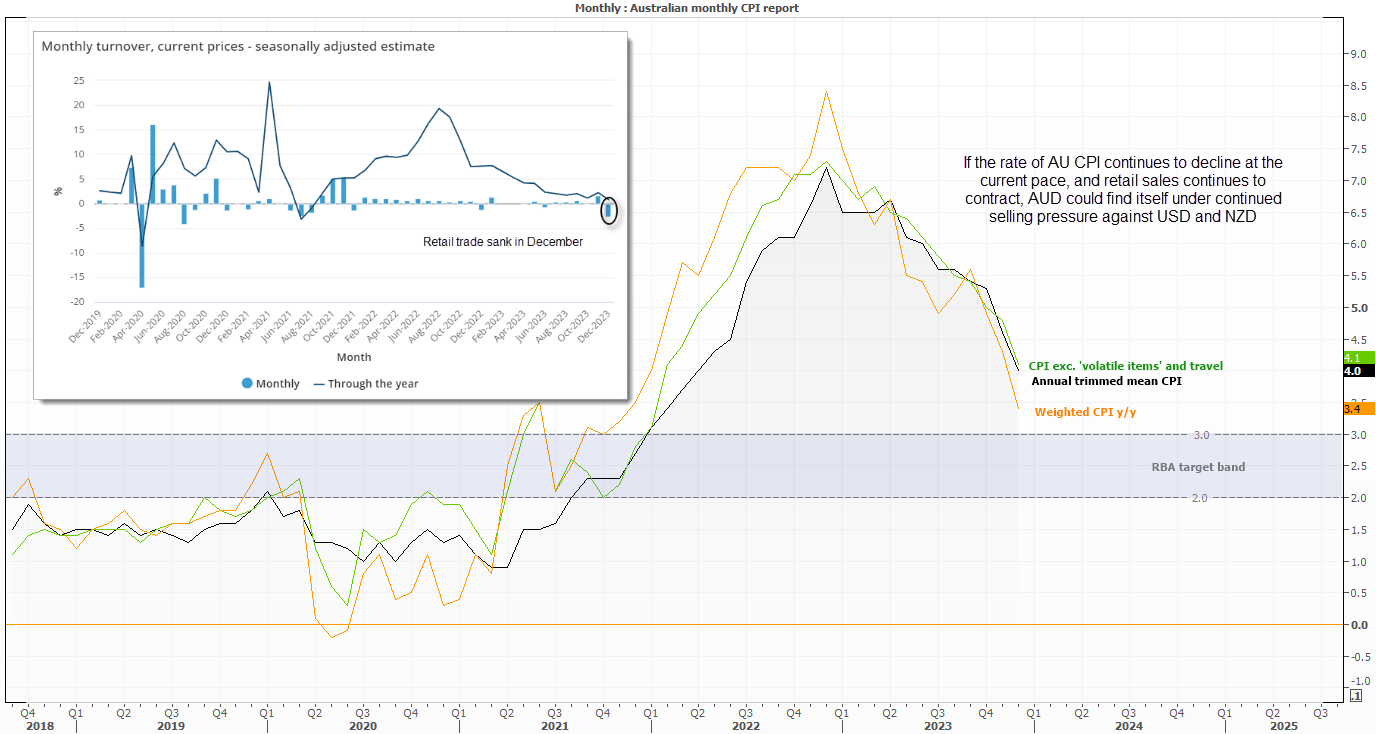

Australian inflation, CPI basket revised:

I expect that most would like to see AU inflation continue to soften next week. The weekly CPI numbers are heading towards the RBA’s 2-3% target band, and the faster it approaches it the better it becomes of RBA-cut bets (to the detriment of AUD bulls. Q4 inflation was softer than expected, and whilst wages reached a 15-year high of 4.2% y/y, the quarterly read slowed to 0.9% q/q to suggest peak wages may be near, if not here already.

However, note that the ABS (Australian Bureau of Statistic) will revise the weightings of their CPI basket, and as my colleague David Scutt pointed out, it “might make things slightly sticker as I gather there'll be more services weighting in this round given that's where spending was being directed. Less goods, more experiences”. If he is right, then CPI may well decline at a slower pace. It may not be enough to warrant further hikes, but it likely pushes back bets of cuts.

Source: Refinitiv

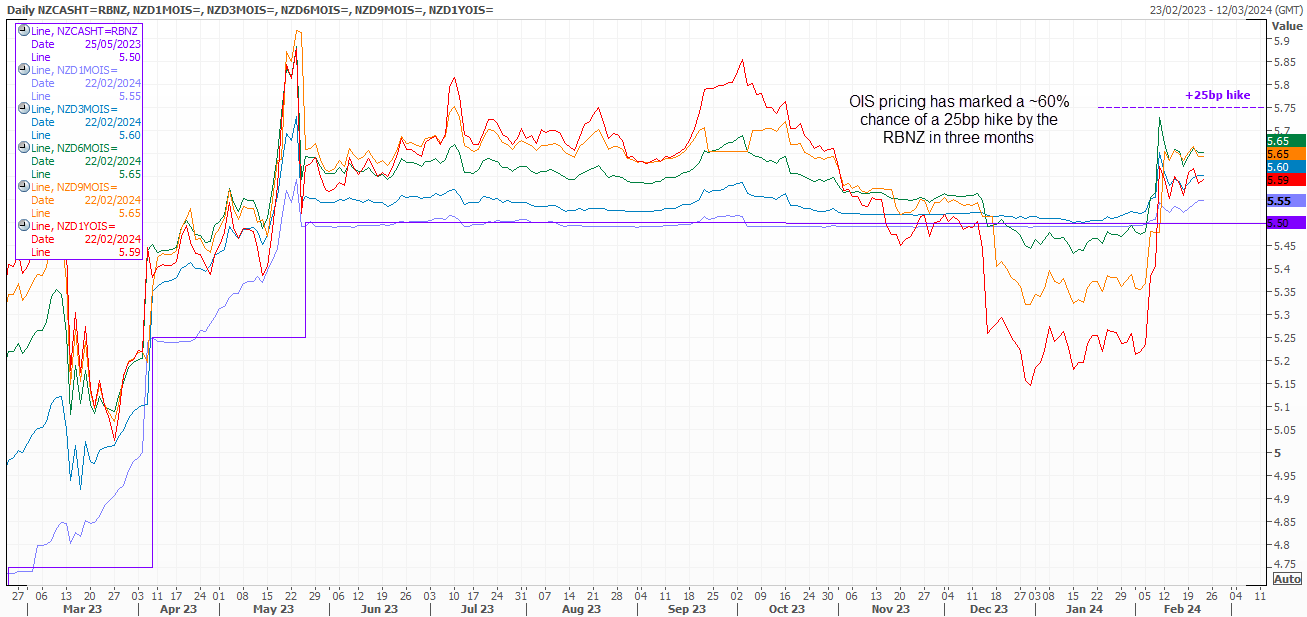

RBNZ meeting, press conference:

The RBNZ are almost certain to hold rate steady at 5.5%, but stronger economic data has seen the 3-month OIS price in a 25bp hike with a ~60% probability. So we may find that the RBNZ reintroduce a tightening bias, whether via their statement, press conference or revised economic forecasts. Their prior monetary policy statement forecast rates to remain at 5.5% this year, so that is an obvious place to look on Wednesday to see if it has been upwardly revised, or cuts have been pushed further back into 2025. Either way, a hawkish RBNZ has hawkish implications for the RBA, although AUD/NZD is likely to suffer given the -1.15bp RBA-RBNZ spread could widen in future.

Source: Refinitiv

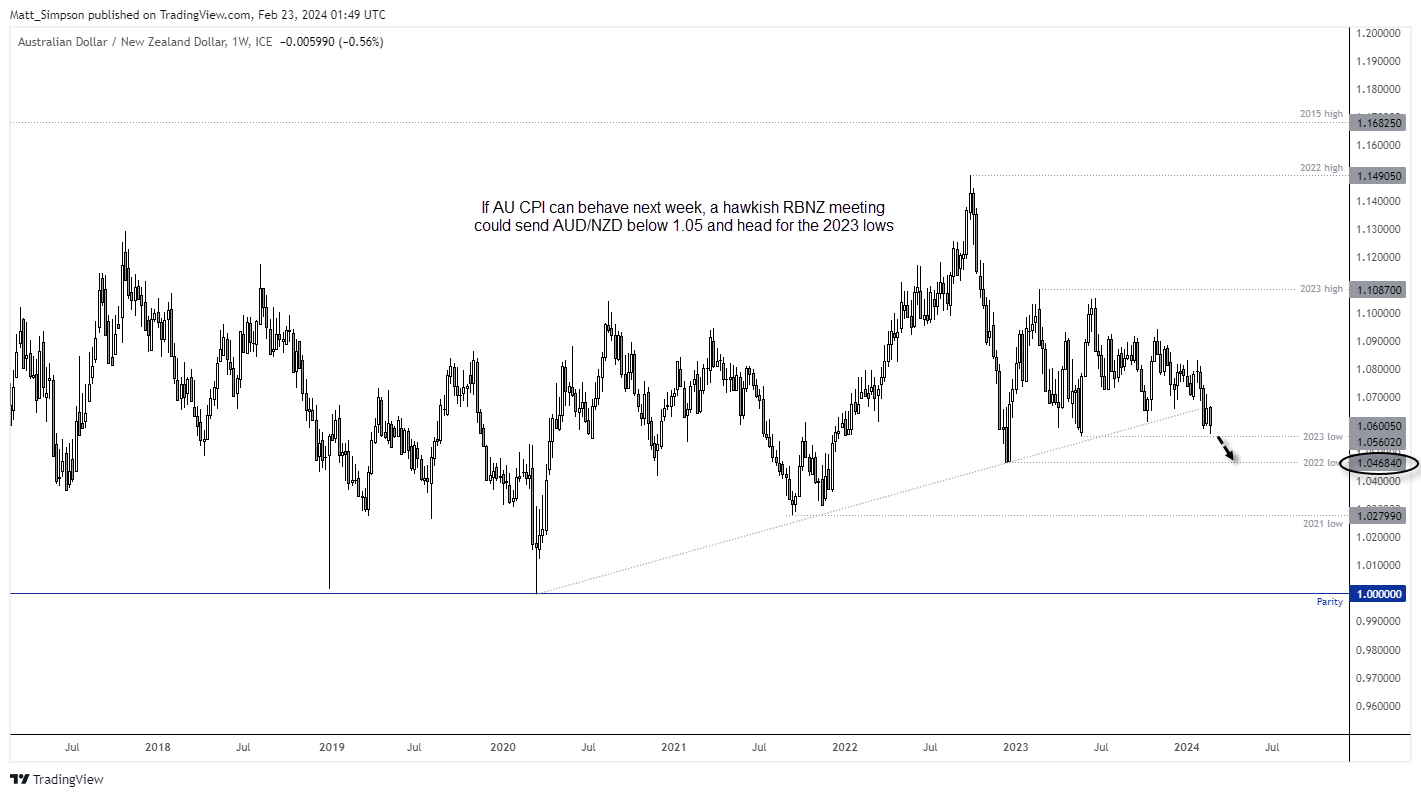

AUD/NZD technical analysis (weekly chart):

The yield differential between RBA-RBNZ cash rates continues to favour the New Zealand dollar. And that could widen next week and provide further pressure on the AUD/NZD cross. The weekly chart shows that the cross touched a 9-month low this week, and is on track for a bearish engulfing candle at the time of writing. A break of the 2023 low brings 1.05 into a focus, a break beneath which will being the 2022 low into focus for bears.

Source: TradingView

US PCE inflation

Inflation data – particularly from the US – remains the favoured data set for traders to decipher the Fed’s monetary policy. And that has a direct impact on AUD/USD, indices and global sentiment in general. We’re on guard for a firmer set of PCE figures, given headline CPI was hotter than expected last week. And if we have already seen a softer CPI report from Australia, a firmer PCE inflation report could surely spell trouble for the Australian dollar.

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest AUD USD articles

June 18, 2024 11:35 PM

June 17, 2024 10:58 PM

June 13, 2024 10:50 PM

June 12, 2024 10:39 PM