Asian Futures:

- Australia's ASX 200 futures are up 22 points (0.3%), the cash market is currently estimated to open at 7,274.20

- Japan's Nikkei 225 futures are up 330 points (1.2%), the cash market is currently estimated to open at 27,718.16

- Hong Kong's Hang Seng futures are up 57 points (0.21%), the cash market is currently estimated to open at 27,316.25

UK and Europe:

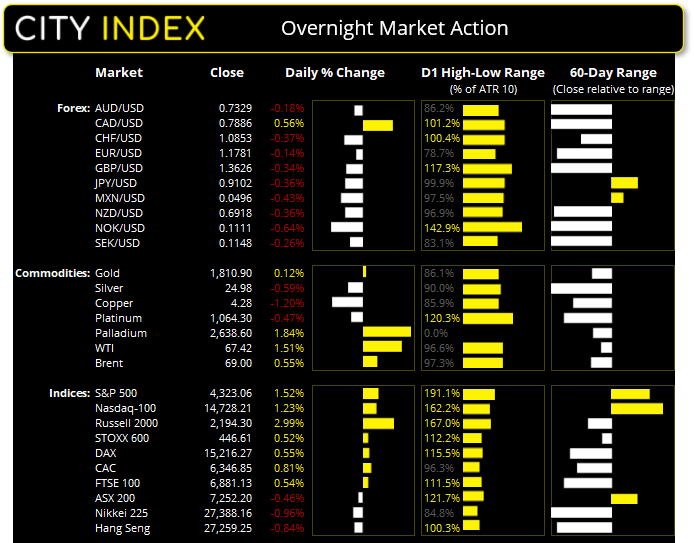

- UK's FTSE 100 index rose 36.74 points (0.54%) to close at 6,881.13

- Europe's Euro STOXX 50 index rose 27.81 points (0.71%) to close at 3,956.34

- Germany's DAX index rose 83.07 points (0.55%) to close at 15,216.27

- France's CAC 40 index rose 50.88 points (0.81%) to close at 6,346.85

Tuesday US Close:

- The Dow Jones Industrial rose 549.95 points (1.62%) to close at 34,511.99

- The S&P 500 index rose 64.57 points (1.52%) to close at 4,323.06

- The Nasdaq 100 index rose 179.116 points (1.23%) to close at 14,728.21

Indices:

Wall Street broke a 4-day losing street as better-than-expected earnings revived economic optimism, placing the spread of the delta variant on the back burner.

Small cap stocks were strong performers with the Russell 2000 recouping nearly 3% and the S&P SC 600 rising 3.03%. The Nasdaq banking index rose 2.65%, outperforming the Nasdaq 100 which rallied 1.23% to close above its 10-day eMA, the FAANG index was up 1.18%.

All S&P 500 sectors were in the green led by healthcare and financials, 5 sectors outperformed the S&P 500 which rose 1.43% and rallied from its 50-day eMA. Travel stocks outperformed to see Norwegian Cruise Line Holdings (NCLH) and American Airlines Group (AAL) rally around 8.3%. Netflix (NFLX) fell over 3% in afterhours trading on weaker earnings.

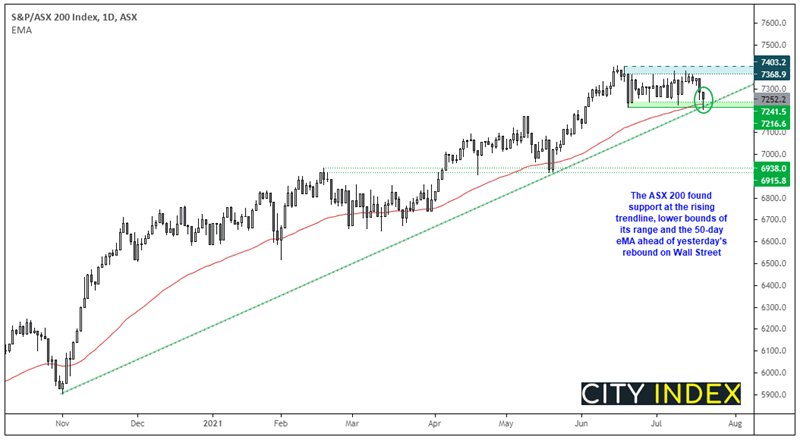

The ASX 200 found support yesterday above its bullish trendline, 50-day eMA and lower bounds of its sideways range. Given the rebound on Wall Street (and that SPI 200 futures are higher) then we fancy its odds of re-testing the upper bounds of that range over the coming session/s. Further out, a break to new highs assumes bullish continuation whereas any signs of weakness near the highs suggests the range is not ready to breakout. A break below the range potentially marks a top.

Learn how to trade indices

ASX 200 Market Internals:

ASX 200: 7252.2 (-0.46%), 20 July 2021

- Healthcare (0.91%) was the strongest sector and Materials (-1.82%) was the weakest

- 8 out of the 11 sectors closed lower

- 63 (31.50%) stocks advanced, 129 (64.50%) stocks declined

- 64% of stocks closed above their 200-day average

- 52.5% of stocks closed above their 50-day average

- 40% of stocks closed above their 20-day average

Outperformers:

- + 6.27% - Oil Search Ltd (OSH.AX)

- + 5.41% - Zip Co Ltd (Z1P.AX)

- + 3.73% - JB Hi-Fi Ltd (JBH.AX)

Underperformers:

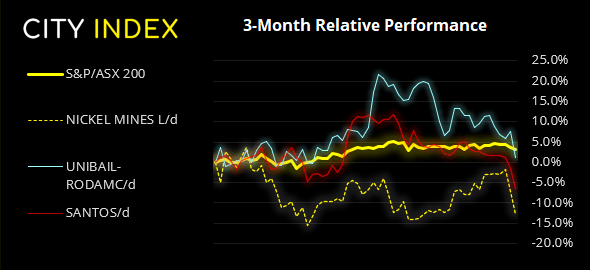

- -6.19% - Nickel Mines Ltd (NIC.AX)

- -6.10% - Unibail-Rodamco-Westfield SE (URW.AX)

- -4.98% - Santos Ltd (STO.AX)

Forex:

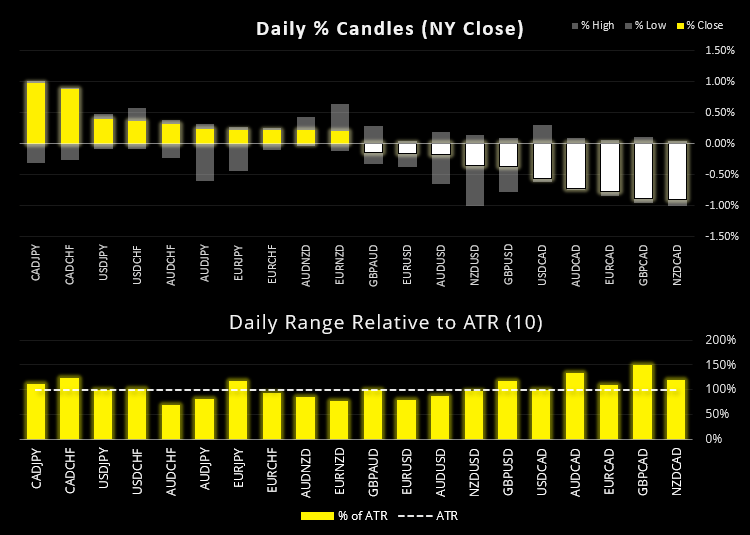

There were signs of a corrective bounce across currency markets too, although relative to US indices they appear relatively tame. The British pound failed to get recover as traders remain wary of the UK lifting lockdown restrictions.

The US dollar index (DXY) hit a new 3-month high yet gave back around 2/3rd of early gains to close with a bearish hammer at its highs.

The Canadian dollar was the strongest currency, supported by a rebound in oil prices and broad bounce across riskier assets. That said, volatility was low relative to Monday’s sell-off so we use the term ‘risk-on’ lightly, although we had questioned yesterday if a retracement could be on the cards given the dwindling bearish volatility seen during the prior Asian session.

EUR/CAD broke a four-day winning streak and is firmly back below its 200-day eMA. NZD/CAD also crossed back below its 200-day eMA to 3-day low after Monday’s bearish hammer. Should volatility subside we would reconsider longs above a part of our bullish wedge target around 0.9082 (with 0.9000) as an interim target.

EUR/USD continues to coil up into a potential bullish wedge above 1.1772 support ahead of tomorrow’s ECB meeting.

Both AUD/JPY and NZD/JPY bounced from their 200-day eMA’s after brief intraday dips beneath them yesterday.

AUD/USD fell to 0.7300 overnight following RBA’s dovish minutes, which prompted several banks to say they now expect the RBA to reverse their earlier tapering given the extended lockdowns in parts of Australia.

Learn how to trade forex

Commodities:

WTI futures held above trend support mentioned in yesterday’s video, although its bounce was underwhelming to say the least closing with a small Doji on the daily chart.

Gold remains choppy as ever and therefore a ‘stand aside’ until momentum tips its hand. Silver fell for a third session to a 3-month low. With no immediate signs of a bottom (although arguable overextended to the downside) it remains a market for bears to consider fading into minor rallies.

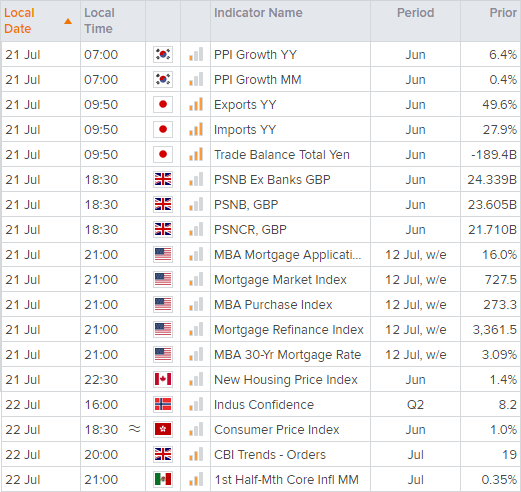

Up Next (Times in AEST)

- Japan’s exports are expected to rise around 65% in June.

- BOJ release their minutes although no fireworks are expected.

- Australian retail sales are forecast to contract by -0.6% (thanks to those pesky lockdowns). AUD is already on the back ropes but perhaps a larger-than-expected miss could further weigh on the currency as it feeds into weaker growth, and further cements the RBA’s dovish stance.

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

10.1.1

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM