2024 Market Outlook Key Points

- After two years of aggressive interest rate hikes, traders think 2024 will bring a “pivot” to interest rate cuts from major central banks.

- Scenarios for interest rate cuts run the gamut from benign “immaculate disinflation” to a dire synchronized global recession.

- The US dollar could benefit from fewer rate cuts than expected following a relatively quiet 2023.

2024 Market Outlook: Central Banks to Start Cutting Interest Rates…But When?

For most traders, the dominant storyline of the last two years has been the most aggressive interest rate hiking cycle in decades.

In response to stubbornly high inflation, the Federal Reserve belatedly started raising interest rates in Q1 2022, and the central bank has now delivered more than 500bps (5%) of interest rate increases in less than two years, in addition to reducing the size of its balance sheet by $1.2 trillion over the same period.

Outside of the US, we’ve seen similar degrees of monetary policy tightening across most of the developed world. The Bank of England actually began raising its interest rate at the end of 2021, a couple months before the Fed, and after 14 consecutive rate hikes, interest rates in the UK sit at the same 5.25% as in the US. The European Central Bank had a later start, only getting off 0% rates in mid-2022, but ECB President Lagarde and Company have since brought their target rate up to a comparable 4.5%.

Central banks in Australia, Canada, and elsewhere have followed similar trajectories. In fact, among the major central banks, only the Bank of Japan remains near the extremely accommodative, “zero interest rate policy” (ZIRP) that dominated the globe in the year or two after the outbreak of the COVID pandemic.

One of the most important themes to watch in 2024 will be the reversal of these trends in monetary policy. Based on recent comments from the likes of the Fed, Bank of England, and European Central Bank, we’ve likely hit peak interest rates for this cycle, though central bankers are adamant that they won’t start cutting interest rates imminently.

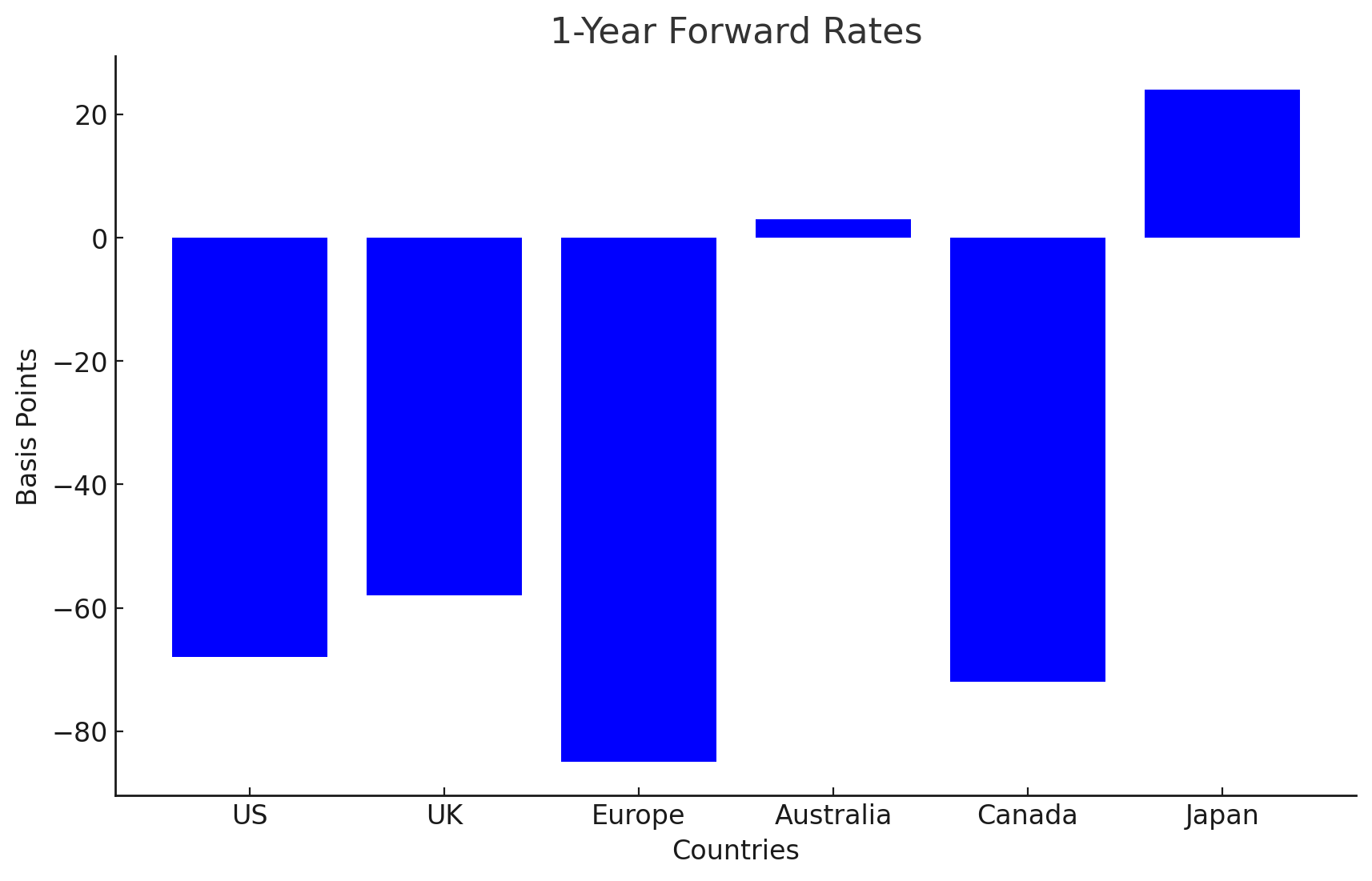

As the chart below shows, traders disagree, with multiple 25bps interest rate cuts priced in over the next year for the Fed, BOE, ECB, and Bank of Canada, with only the RBA and BOJ expected to see (slightly) higher interest rates this time next year:

Source: Bloomberg, StoneX. Data as of November 21, 2023.

To put a more precise timeframe on these market-based measures, traders currently believe that the ECB will be the first to kick off interest rate cuts as soon as April, with the BOC and Fed following in May and the Bank of England currently priced at around a coinflip to cut rates in June.

2024 Market Outlook: What Could Cause Central Banks to Cut Interest Rates?

Amidst this backdrop, a key question for readers to ask is, “what will cause central banks to cut interest rates, despite their current assertions that interest rates will remain higher for longer?”

Possible explanations run the gamut from benign to the dire, but we see three main possibilities:

1. Benign Disinflation

One historically rare but increasingly likely scenario is that inflation continues to moderate toward central bank targets without a dramatic slowdown in the underlying global economy. If central bankers gain confidence that their inflation goals will soon be met, there is a case for a proactively cutting interest rates from the current “restrictive” levels to more neutral rates, especially if labor markets show signs of slowing.

2. Deep Recession

A more worrying scenario is that the global economy rolls over and sees a sharp contraction in 2024. In that case, central bankers will have to skip right through so-called “neutral” levels of interest rates to outright accommodative levels to try to stimulate the economy and support the labor market.

3. Negative Shock

The final possibility is the one that always exists is the chance of a proverbial “black swan,” as we saw with COVID, that changes the entire economic paradigm and requires immediate interest rate cuts across the globe. These scenarios are hard to handicap but always worth keeping in the back of our minds.

2024 Market Outlook: What if Central Banks Don’t Cut as Much or as Soon as Expected?

In our view, there’s at least a chance that markets are “hearing what they want to hear” when it comes to the Federal Reserve and other major central banks pivoting to interest rate cuts in the first half of 2024. As long as economic conditions continue to show modest growth, central banks are likely to keep interest rates higher than they’ve been in recent history to ensure that inflation absolutely does not become entrenched.

If the market is overestimating the amount (or at least the immediacy) of interest rate cuts, it could serve as a headwind for stock and bond markets that are banking on interest rates declining in the near future. The forex market impact may be more nuanced, but generally speaking, the countries and central banks seeing unexpectedly strong growth could benefit, especially if there are significant rate cuts priced in already, as there are with the euro and US dollar.

It’s rarely a good idea to argue with the market, but traders have consistently underestimated the resolve of global central banks over the last couple of years, and we wouldn’t be surprised to see it happen again in 2024.

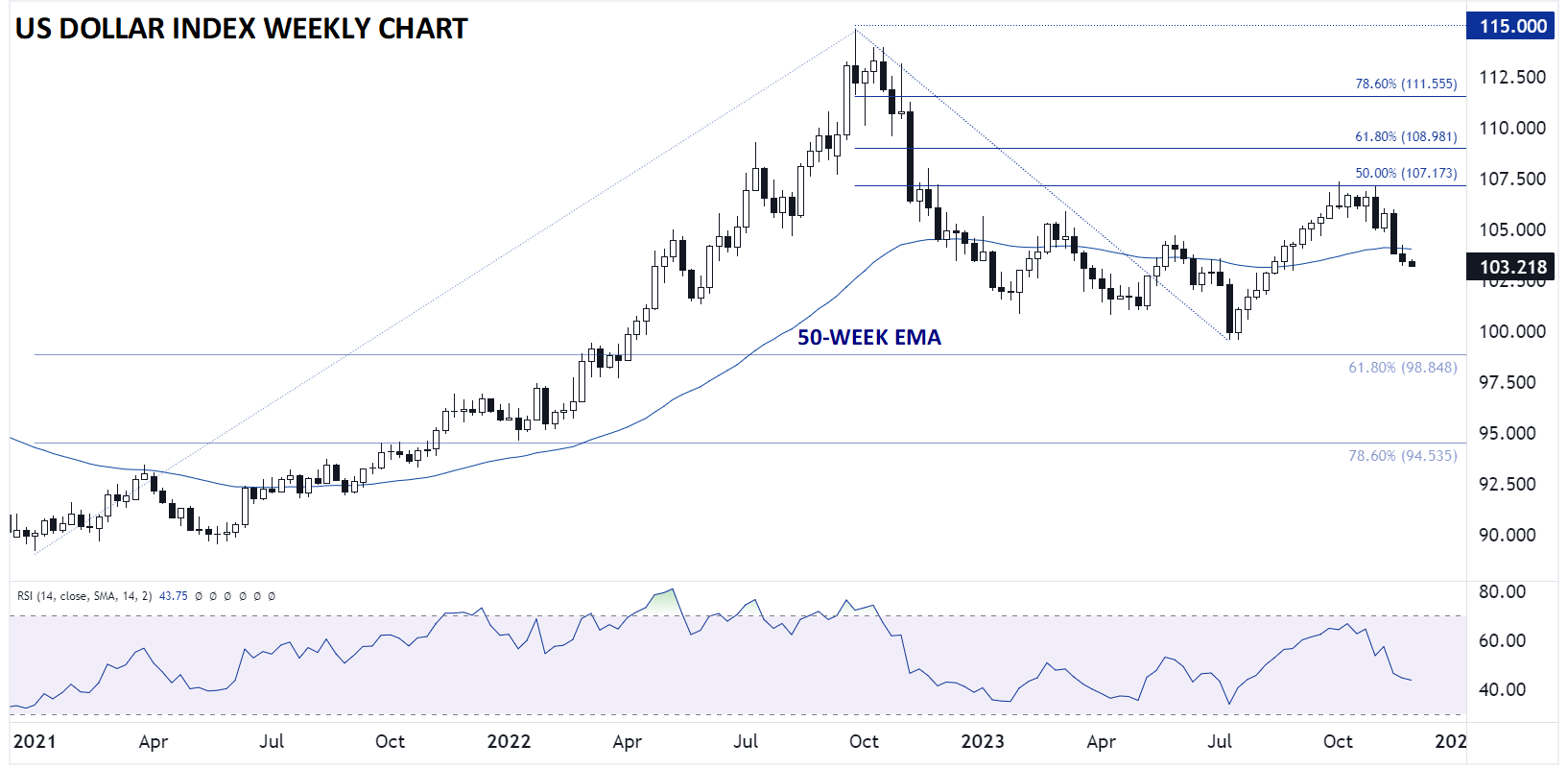

US Dollar Index Technical Analysis – DXY Weekly Chart

Source: TradingView, StoneX

As the chart above shows, the US Dollar Index (DXY) spent most of 2023 to date marking time around the 104.00 area. The world’s reserve currency did see a consistent bout of strength through the third quarter of the year, but as of writing in late November, appears on track to close the year near where it started.

Looking ahead to 2024, the US economy has generally held up better than most of its major rivals, and if that trend continues, the US dollar could rise as traders start to push back interest rate cuts to the second half of the year. In that scenario, the US Dollar Index could rally toward its 2023 highs in the 107.00 range if not toward the 61.8% Fibonacci retracement of the 2022-2023 drop at 109.00.

-- Written by Matt Weller, Global Head of Research

Follow Matt on Twitter: @MWellerFX

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest US Dollar articles

July 19, 2024 11:30 AM

July 18, 2024 10:00 AM

June 6, 2024 01:54 PM

May 23, 2024 05:03 AM