March 13, 2020 11:10 AM

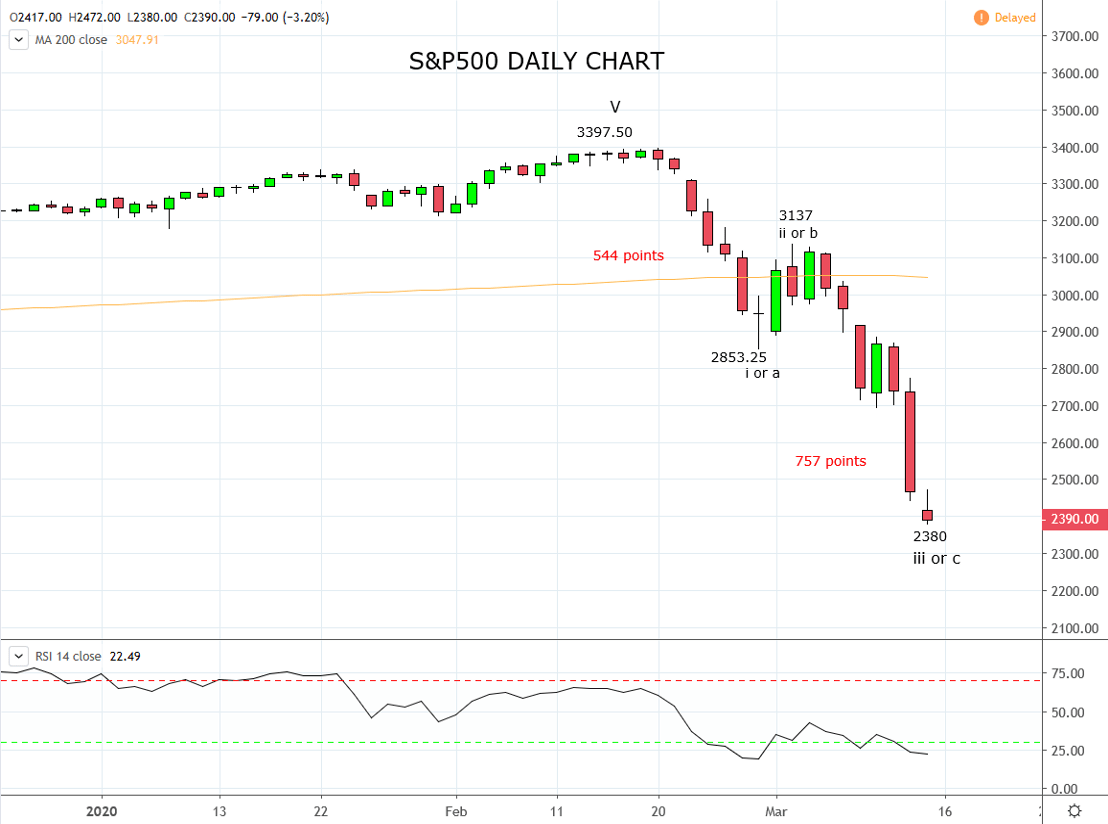

On the eve of Friday the 13th, U.S. equity indices suffered their largest one day fall since the 1987 stock market crash. Globally, key equity markets have exceeded most downside expectations stemming from Covid-19 and are now approximately -30% below their highs from just four weeks ago.

Contagion from equities markets has spread across asset classes including traditional safe-haven assets, U.S Treasury bonds and gold and prompting the question “Why is everything being sold and where is the selling coming from?”

As mentioned recently, when prices across different asset classes fall simultaneously, it often indicates leveraged investors are either reducing their risk/positions across the board, being margin called or investors are withdrawing money.

Risk Parity Funds would appear to be vulnerable to the type of moves viewed across various asset classes this week and may be partially to blame for some of this week's downside acceleration.

As opposed to a standard Balanced Fund that holds 60% of its assets in stocks and 40% in bonds, Risk Parity funds hold a higher allocation of their portfolios in bonds (sometimes using leverage) at the expense of equities as modelling confirms the volatility in bonds is far lower than that of equities. Risk Parity funds also include commodities such as gold and oil in their portfolios to provide increased diversification.

Risk Parity Funds first emerged in the mid 1990’s and gained popularity after the Global Financial Crisis as they outperformed traditional Balanced Funds. Their larger portfolio allocation into bonds and the subsequent rally in bond markets providing some nice offset to the losses from the equity component of portfolios.

The rapid moves in markets this week is likely to have forced Risk Parity funds and other similar volatility targeting funds to deleverage and rebalance, creating a vicious cycle of selling across asset classes.

Potentially the bigger question around Risk Parity Funds is this. In a world that is swiftly returning to zero interest rates and where bonds can then only provide limited portfolio returns and by definition diversification, will the events of the past week end the popularity of Risk Parity strategies once and for all?

Source Tradingview. The figures stated areas of the 13th of March 2020. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Australia 200 articles

February 15, 2024 11:33 PM

February 15, 2024 01:42 AM

February 14, 2024 05:39 AM