Key takeaways

- Instacart IPO priced at $30, giving it a valuation of almost $10 billion

- Instacart shares initially soared when they started trading before pulling back

- Valuation looks reasonable, but sales multiple slightly higher than rivals

- Has delivered rapid growth and has been profitable for 18 months

- But growth is slowing down and it will slip back into the red, setting a much more challenging outlook

- Pressure is high on its advertising business to drive growth

- Ambitious plans to expand into new industries and enter overseas markets

Instacart IPO to earn $10 billion valuation

Instacart, officially trading as Maplebear Inc, completed its initial public offering at $30 per share on Tuesday September 20, 2023. That raised $660 million for Instacart and gave it an initial valuation of just under $10 billion upon listing.

The stock, trading under the ticker 'CART', soared to as high as $42.95 when it started trading before pulling back and ending the day closer to its IPO price at $33.70. That gave Instacart a valuation of about $11.2 billion at the end of the first day of trading.

Instacart IPO valuation appears reasonable

Instacart’s IPO valuation could be one of the most reasonable we have seen for several years, and it appears to have learnt from the mistakes made by its rivals that set their IPO valuations too high.

For example, DoorDash went public in late 2020 at a valuation of $72 billion but has since seen this slump to less than $33 billion. Uber has also spent more time trading below its IPO price than above it since listing, although is now in back positive territory three years later thanks to the stellar recovery in the stock during 2023.

Instacart has also seen its valuation drop in recent years. It was worth as much as $39 billion at its peak during the pandemic before falling to $24 billion during a funding round in mid-2022. The price tag has continued to fall to reflect the fact Instacart faces weaker growth prospects today compared to the boom it experienced during the pandemic, as well as the more tempered valuations applied by public markets.

Instacart came to market with a valuation equal to around 3.9x its last annual sales (or 4.3x after the gains on the first day of trading). That is above its rivals, with DoorDash trading at 3.6 forward sales and Uber at 2.5x. Notably, both DoorDash and Uber went public at much higher multiples, showing how the attitude toward tech-based growth stocks has toughened following the lofty valuations we saw between 2019 to 2021.

The fact Instacart has been profitable at the bottom-line for the past 18 months should help support that higher multiple and could draw interest from investors seeking fast-growing tech stocks that can also turn a profit and sustain itself. Cornerstone investors Norges Bank, TCV, Sequoia, D1 Capital Partners and Valiant Capital Management could also provide some stability, which could have bought up to 60% of all the shares on offer through the IPO.

However, it is not all sunshine and rainbows. Instacart is facing slower growth, more intense competition and will not remain profitable for very long – all of which could hurt demand for the stock.

Let’s dive into the company and look at the opportunities and challenges that lie ahead…

Instacart: Don’t be fooled by pandemic-induced growth

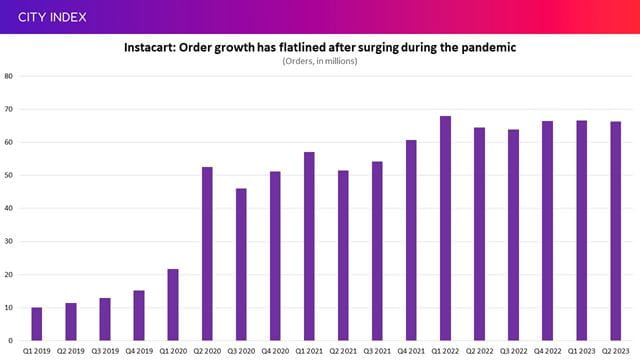

Instacart came into its element during the pandemic as more people started to order groceries online, leading to accelerated growth. Online orders quadrupled from just 3% of total US grocery sales in 2019 to 12% in 2022 – and Instacart found itself in the right place at the right time.

However, this boost has now subsided and Instacart is already gearing up for a slower pace of growth going forward, especially because economic conditions are much tougher as higher interest rates, inflation and dwindling savings all force consumers to tighten their belts. Orders through its Instacart Marketplace platform were up less than 0.5% year-on-year in the first half of 2023, and they have remained broadly flat for over a year.

(Source: Instacart prospectus)

Instacart is about much more than just facilitating online grocery orders (more on this later), but its entire business is highly sensitive to the state of the economy. Its fortunes are directly tied to the performance of the US grocery market, which is currently dealing with more cash-strapped consumers seeking better value. Instacart users are already making smaller orders less frequently in response to higher prices.

This environment challenges Instacart’s model, which now has to show its service adds worthwhile value for the added cost compared to shopping in-store. Consumers prioritised convenience when they had stimulus-ladened wallets during the pandemic, but that is slowly giving way to value as savings dwindle, inflation remains elevated and higher rates bite.

Instacart is profitable, but not for long

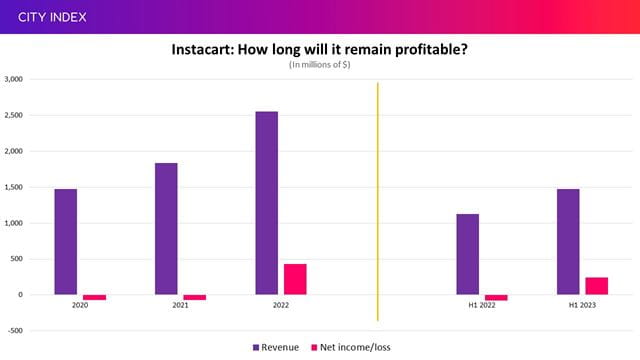

Instacart has lost almost $1 billion building the business over the past decade, but it turned profitable in 2022 and has managed to remain out of the red during the first half of 2023.

That will music to investor’s ears. As the economy chugs along at a slower pace, this has shifted the spotlight from growth stocks to those that offer value, produce profits and can sustain themselves. Based on its results over the past three-and-a-half years, Instacart appears to hit all the right notes by delivering rapid growth and profits.

(Source: Instacart prospectus)

It could be argued that Instacart has chosen an apt time to launch its IPO with 18-months of profit and some impressive pandemic-induced growth under its belt to impress the markets, especially as growth is slowing down and it is preparing to re-enter the red. Instacart has said it will “continue to prioritize profitable growth”, but investors should brace for more losses.

Instacart has said it will book losses in the current quarter and over the full year in 2023 because of the high amount of stock-based compensation, principally on RSUs (restricted stock units), that will spike once the listing is complete. There are millions of RSUs in issue and many have reached their vesting conditions, and Instacart has said most of the proceeds from the IPO will go toward satisfying these.

Plus, it is still very early days for Instacart and it remains in growth mode, which will require it to up investment in everything from headcount and marketing to incentives and its advertising business in order to grow its platform and broader ecosystem. With only the US grocery market conquered so far, Instacart has big plans to move into new industries and take its technology overseas into new international markets.

Instacart faces intense competition

Instacart has carved-out a unique role for itself after becoming the trusted technology partner for thousands of US grocery companies across the US, but competition is intensifying and its rivals are formidable.

Instacart’s appeal is that it can provide technology that no individual grocer could afford to develop on its own, but the largest grocers with the most firepower, like Walmart and Target, are refusing to rely on a third-party to lead their digital transformations and use Instacart to compliment their own offerings developed in-house. This has proven a problem before. Whole Foods was a major customer until it was bought by Amazon in 2019, leading to its being removed from Instacart and shifted onto Amazon’s own grocery platform.

Instacart’s ability to remain in demand among the biggest clients is crucial considering 43% of the gross transaction value that goes through its platform is from the top three players.

Ongoing consolidation within the grocery market could also change the landscape further. For example, Instacart has warned there is a risk that the pending merger of Albertsons and Kroger could see its relationship with the firms change.

Instacart’s goal is to become the company that provides all the tech grocers need to evolve and move into the digital age, but it is fundamentally underpinned by many of the same factors as companies like DoorDash and Uber. Notably, it also has to compete for employees with these same companies, with gig economy workers known to switch to the most lucrative platform.

Plus, it isn’t the only company trying to thrust supermarkets into the modern age. UK-listed Ocado, which uses its tech to build automated warehouses for companies like Kroger, Sobey’s, AEON and ICA while also running its own online-only grocery service, has been in the game since 2000 but took 15 years to generate its first profit and has struggled to stay in the black since. While Instacart is a different company to Ocado, it isn’t the only game in town and the pair share some challenges.

Meanwhile, Instacart’s fast-growing ads business is getting a lot of attention and seen as an engine of future growth, but it faces stiff competition here too from an array of platforms, including the major players like Meta and Alphabet.

Instacart: Can the flywheel keep going?

Instacart has spent over a decade solving a major problem for the US grocery market. There is no shortage of companies that deliver food from A to B, but Instacart has a broader vision to “build the technology that powers every grocery transaction”.

Whereas shoppers now happily buy everything from electronics to clothing online, the nature of the US grocery market means penetration is much lower, at about 12% currently after quadrupling during the pandemic. Instacart believes penetration will remain comparatively low versus other industries but sees it doubling “over time”. With this in mind, Instacart knows most of the money is to be made in-store, which is why it offers much more than a sales platform and delivery drivers by supplying an array of tech and services to power both online and in-store sales to over 1,400 companies.

Instacart has created a three-pronged business catering to different pockets of the market - one on consumers, another on grocers, and a third on consumer brands. This has helped it create a business that benefits from the flywheel effect…

Millions of Americans use Instacart Marketplace to order groceries to their door, most of which are signed up to the Instacart+ subscription service that offers them savings when they shop. They get a broader selection of products from a wider variety of shops, helping them find better value and save time.

That, in turn, provides a new digital avenue to market for US grocery chains that have not been able to invest in their own offerings because of their low-margins. The fact most of the orders placed on Instacart Marketplace are fulfilled by the company’s own ‘Shoppers’ – which pick, pack and deliver – doesn’t put any strain on their labour force.

Fulfilling orders on a nationwide scale and across thousands of different grocers gives Instacart unrivalled data on the industry and this will only improve the more orders it takes and fulfils. It then uses this data to provide insights to grocers, which can then use it to further improve sales for both them and Instacart.

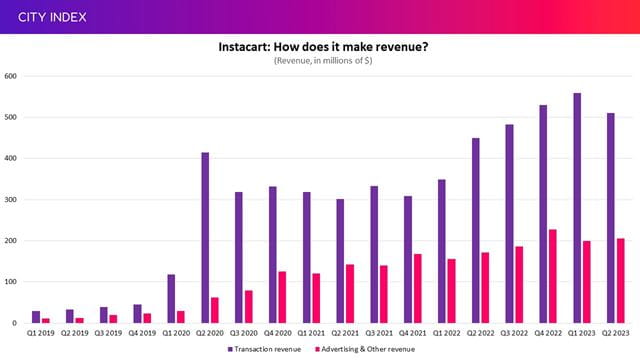

That data and reach is also underpinning its fast-growing ads business that is mostly targeted toward consumer goods brands, with companies like Campbell’s Soup, Nestle and Pepsi already utilizing its service. Investors are excited by the prospects here as the growth and profitability potential is much higher. Ads revenue doubled year-on-year in 2021, boosted by the pandemic, and grew another 29% in 2022.

(Source: Instacart prospectus)

Each unit feeds the other. More users leads to more transactions, which leads to more data and improves its enterprise business, which helps fuel further growth before repeating once again. This flywheel effect also improves profitability as Instacart benefits from improved scale, which is needed in order to generate the cash it needs to keep expanding.

Conclusion: Well-positioned, but challenges ahead

Instacart is much more than just a grocery delivery service and is solving a big problem for the industry by supplying new routes to market and, more importantly, the technological advancements that grocers so desperately need but simply can’t afford due to their low levels of profitability. By scaling its technology and offering it to thousands of different firms, Instacart is providing the tools to grocers at a lower cost compared to the expense needed to go it alone.

This has seen it evolve into a business underpinned by the flywheel effect, spun by its different services targeting consumers, grocers and consumer goods firms. It sits at the heart of the grocery industry’s digital transformation and is positioned to win so long as the entire market keeps growing.

However, the downside to the flywheel effect is that it can work both ways. A deterioration in one part of the business will hurt the rest. Lower user numbers would make it less useful to grocers and supply less data, hurting the reach and insight of its enterprise operations and so on.

Instacart benefited massively from the pandemic, which thrusted it several years ahead of schedule. But that has now unwound and the growth outlook from the grocery market is far less impressive, which is heightening pressure on its ads business to drive the business forward – but this too is sensitive to tougher economic conditions and fierce competition. The recent profits may also woo the markets, but it is already back in the red.

Ultimately, Instacart may be facing its toughest economic outlook since inception and the pressure is on for it to show consumers, grocers and consumer goods companies that it can offer value they can’t get anywhere else. It will need to cement its role as the trusted tech partners to grocers, demonstrate it is still the most convenient and cost-effective way to order groceries, and that it has the data and reach to supply ads that offer higher returns compared to the array of alternatives available on the market.

How to trade Instacart stock

You can trade Instacart shares, once they start trading, with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for ‘Instacart’ or ‘CART’ in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Or you can practice trading risk-free by signing up for our Demo Trading Account.

Latest market news

Today 01:39 PM

Today 11:05 AM

Today 10:46 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM