Eurozone Is deflation back

Only a few weeks ago it looked like the spectre of deflation had finally lifted from the Eurozone. However, today’s German CPI figures throw that […]

Only a few weeks ago it looked like the spectre of deflation had finally lifted from the Eurozone. However, today’s German CPI figures throw that […]

Only a few weeks ago it looked like the spectre of deflation had finally lifted from the Eurozone. However, today’s German CPI figures throw that into doubt. EU harmonised data for June shows that CPI fell 0.2% on the month, which pushed the annual rate down to 0.1% from 0.7% in May. So, is this just a pause in the uptrend for CPI, or is the trend over before it even began?

To answer this we need to dig a bit deeper into the data. Brandenburg and North Rhine Westphalia both released the breakdown of prices today. For Brandenburg the largest downward impacts on the CPI were rent and housing costs, utilities – mostly heating oil, transportation, communication and package tour holidays, which all saw prices drop by more than 1% compared to this time last year. In North Rhine Westphalia the largest downward pressures on CPI included transportation and communication, rent and housing costs and clothing. This is worth noting as the price declines were not only concentrated in the energy sector, but were broad-based suggesting that some areas of Germany’s economy could be losing their pricing power.

In fairness, one month does not necessarily reverse a trend, but it could keep the ECB on high alert for the overall Eurozone figure, which is released on Tuesday morning. If we see more evidence that inflation is weak then we could see the ECB’s focus shift back to its QE programme.

Will the ECB boost its QE programme?

The ECB’s only mandate is to protect price stability, so if CPI data starts moving backwards then we could see the ECB renew efforts – and potentially even boost – its QE programme. While we don’t think that this is likely now, combined with the economic impact of the Greek crisis on the currency bloc, this summer could see pressure build on the ECB to boost its QE programme.

So, while the EUR’s performance has been notable for its resilience to the most dangerous stage of the Greek crisis yet, it may falter if we see the ECB talking (or even taking) further steps to shore up the Eurozone economy from the effects of these two dangers.

What does this mean for the market?

In the short-term the market focus is all on Greece as we wait to see if Athens will default on Tuesday and the outcome of the bailout referendum next Sunday. However, we note two things to watch in the financial markets in the coming days and weeks that could limit EUR upside and boost European stocks:

1, German bund yields:

The two year yield is back below -0.20 basis points. Likewise, the 10-year yield is also below 0.85%, nearly 10 basis points lower than it was on Friday. While we expect yields to try and recoup some recent losses as Greek fears calm down, if we see an escalation of Greek concerns later this week, or a weak Eurozone CPI figure on Tuesday then we could see further weakness in German yields, which could limit EUR upside.

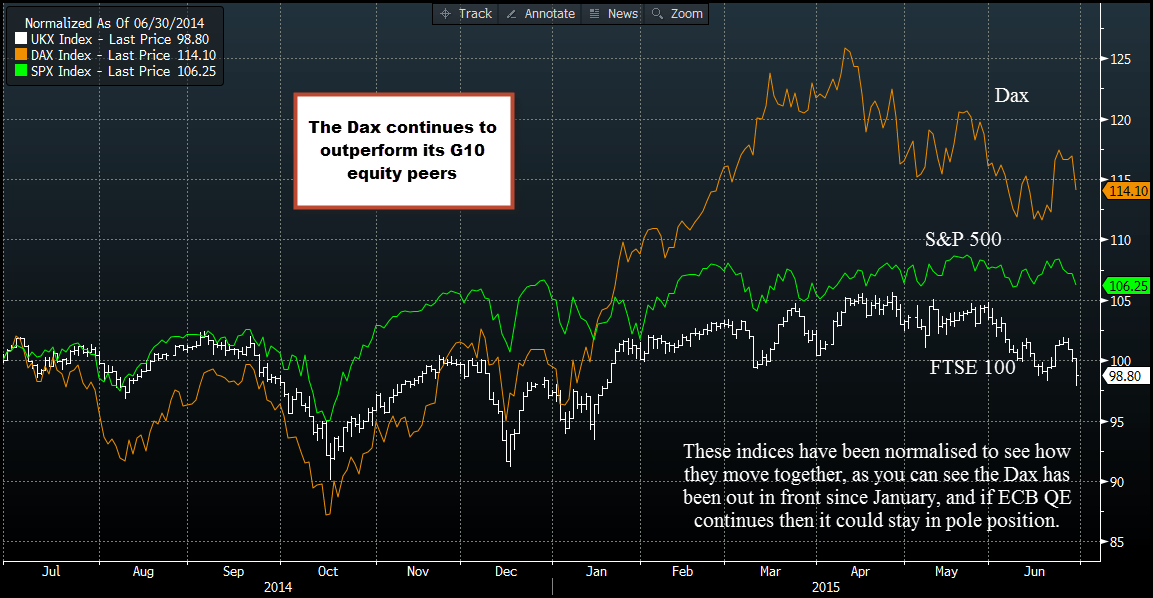

2, Dax: still king of the G10 equity space

The German index may have come under severe pressure earlier as news of Greek capital controls dominated the market, however, the Dax continues to outperform its US and UK counterpart, as you can see in the chart below. If we see weak Eurozone CPI this week then the prospect of a prolonged or enhanced QE package from the ECB in the coming months could keep the Dax at the top of the equity pile.

From a technical perspective, the Dax managed to stay above the 10,800 level on the back of the sell off at the start of this week – the low from earlier in June. Added to that, since the German CPI release, the Dax has had a moderate recovery, which could gain momentum on the back of weak Eurozone CPI on Tuesday.

Takeaway:

Figure 1:

Source: FOREX.com and Bloomberg