Asian Indices:

- Australia's ASX 200 index fell by -6.2 points (-0.09%) and currently trades at 7,013.40

- Japan's Nikkei 225 index has risen by 157.36 points (0.56%) and currently trades at 28,255.61

- Hong Kong's Hang Seng index has fallen by -87.26 points (-0.31%) and currently trades at 28,363.03

UK and Europe:

- UK's FTSE 100 futures are currently up 3 points (0.04%), the cash market is currently estimated to open at 7,022.79

- Euro STOXX 50 futures are currently up 11 points (0.28%), the cash market is currently estimated to open at 4,010.91

- Germany's DAX futures are currently up 21 points (0.14%), the cash market is currently estimated to open at 15,391.26

Thursday US Close:

- DJI futures are currently up 31 points (0.09%), the cash market is currently estimated to open at 34,115.15

- S&P 500 futures are currently up 14 points (0.1%), the cash market is currently estimated to open at 4,173.12

- Nasdaq 100 futures are currently up 4 points (0.1%), the cash market is currently estimated to open at 13,498.09

Learn how to trade indices

PMI’s across Asia were on the soft side, with Australia’s composite falling to 58.1 from 58.9 prior, dragged down by the service sector. Japan’s flash manufacturing PMI was also lower, falling to 52.5 compared with 53.6. Should this trend continue through to Europe and US (which it sometimes can) then it may make for a slightly underwhelming finish to a week which has seen a strong attempt by equity markets to claw back earlier losses. But with inflation seemingly less of a concern (for today at least) then markets could well lap up any positive reads to help their respective equity markets. At the time of writing, futures markets across Europe and US have opened a touch higher, suggesting it could be a better end to the week than it looked when the week began.

Asian equities moved higher overnight, taking the lead from Wall Street which saw the Nasdaq 100 lead equities higher by nearly 2%. The Nikkei 225 was up around 1% whilst the MSCI’s APAC (ex-Japan) index was up 0.6%. Yet China’s CSI300 and SSE composite were down -0.8% and -0.45% respectively, and the ASX 200 currently trades around -0.15% lower.

FTSE 350: Market Internals

FTSE 350: 7019.79 (1.00%) 20 May 2021

- 260 (74.07%) stocks advanced and 80 (22.79%) declined

- 21 stocks rose to a new 52-week high, 3 fell to new lows

- 84.33% of stocks closed above their 200-day average

- 16.52% of stocks closed above their 20-day average

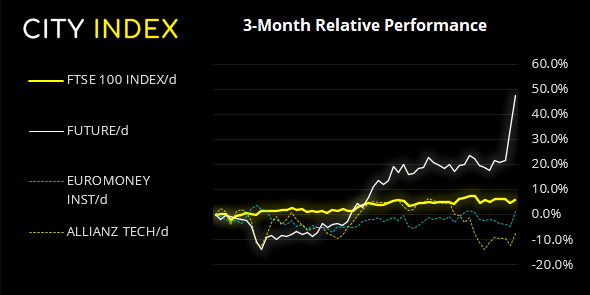

Outperformers:

- + 9.59% - Future PLC (FUTR.L)

- + 5.97% - Euromoney Institutional Investor PLC (ERM.L)

- + 5.60% - Allianz Technology Trust PLC (ATT.L)

Underperformers:

- -23.3% - Trainline PLC (TRNT.L)

- -4.37% - Helios Towers PLC (HTWS.L)

- -2.91% - Tui AG (TUIT.L)

Forex: Retail sales and PMI in focus for GBP traders

The US dollar index is on track for another bearish close this week and trades near its lowest level since February. Given the Fed aren’t likely to respond to stronger data, a PMI miss for the US may provide the more volatile response from the dollar than a strong PMI set, although it should help US equities remain supported.

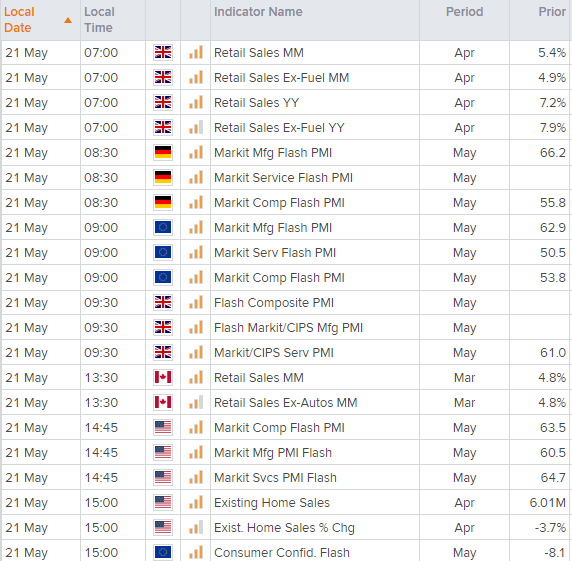

Retail sales for the UK is released shortly at 07:00 GMT, so we’ll find out if shoppers have maintained the momentum seen in April’s report. Given restrictions have been eased further, there’s a decent chance there could be some punch numbers in there today.

Separately, The BOE (Bank of England) are set to hold rates at 0.1% until 2023, according to a Reuters survey of economists. They also forecast the UK economy to grow 5.9% in 2021 and 5.3% in 2022. Current estimates for Q1 2020 have now risen to 4.1%, up from 3.5% in the April poll.

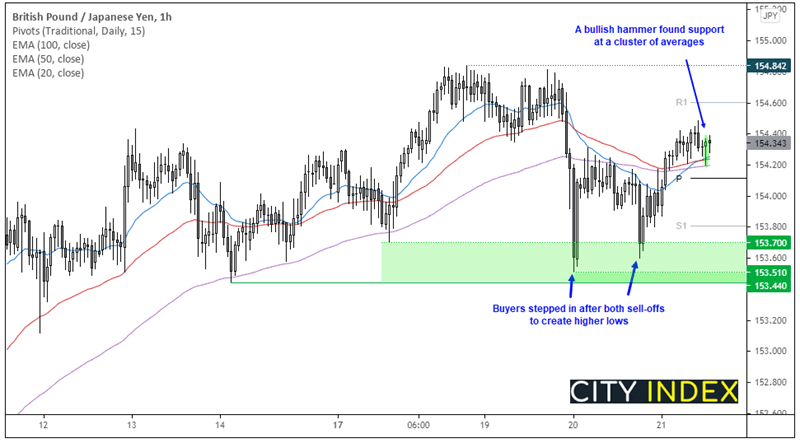

GBP/JPY printed a bullish inside day yesterday following the prior day’s bearish outside candle, which suggests demand above Wednesday’s low is building. We can see on the hourly timeframe that the prices have found support at the 20, 50 and 100-dar eMA’s and currently trade above the daily pivot. Should retail sales and PMI come in strong, it could retest yesterday’s high and move towards the daily R1 level at 54.60. Should prices drift lower initially, we’d still consider bullish setups above the daily pivot around 154.10 if evidence of a base presents itself. GBP/USD is in a similar situation to GBP/USD, where the daily pivot resides around 1.4160.

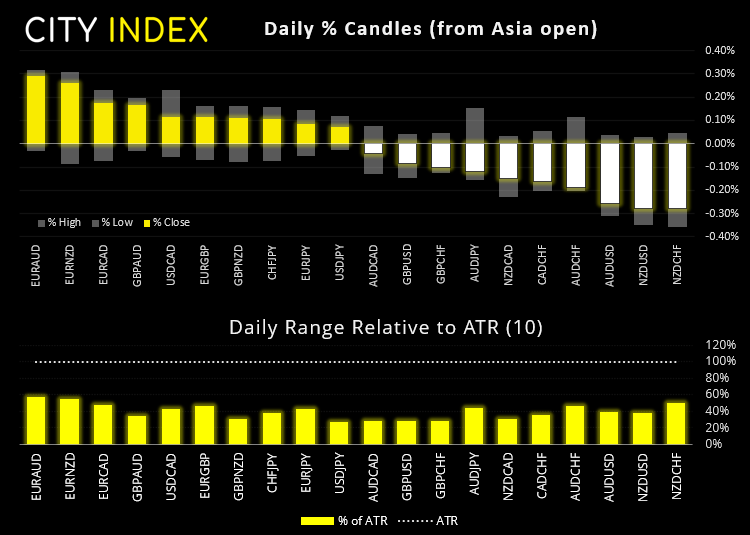

Elsewhere, commodity currencies (NZD, AUDN, and CAD) were weaker as the commodities rally continues to lose steam. Iron ore is also lower this week (after a meteoric rise) so has been acting as a headwind for the Australian dollar, whilst weak oil prices have also taken their toll on the Canadian dollar and, to a degree, NZD and AUD.

Learn how to trade forex

Commodities: Oil remains sensitive to Iran-deal headlines

Oil prices are trading near their lows after three consecutive bearish closes. In a nutshell, traders remain concerned that any deal with Iran (and lifting of sanctions) will increase oil supply, hence the weaker oil prices. Although we’d expect a bullish volatile reaction should it be confirmed that a deal will not be reached. See this morning’s Asian Open report for a closer look.

Metals were a touch lower overnight with spot palladium down -0.7% whilst gold and silver was off -0.3%. Gold is also down -0.3% against the euro and Swiss franc but flat against the Australian dollar. Platinum bucked the trend and currently trades 0.13% higher.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest FTSE 100 articles

July 10, 2024 11:55 PM

July 4, 2024 11:00 AM

June 19, 2024 12:00 PM

March 11, 2024 04:30 PM