Asian Indices:

- Australia's ASX 200 index rose by 34.8 points (0.47%) and currently trades at 7,414.10

- Japan's Nikkei 225 index has risen by 176.36 points (0.64%) and currently trades at 27,758.87

- Hong Kong's Hang Seng index has risen by 698.43 points (2.74%) and currently trades at 26,172.31

UK and Europe:

- UK's FTSE 100 futures are currently down -8 points (-0.12%), the cash market is currently estimated to open at 7,008.63

- Euro STOXX 50 futures are currently down -10.5 points (-0.26%), the cash market is currently estimated to open at 4,092.53

- Germany's DAX futures are currently down -43 points (-0.28%), the cash market is currently estimated to open at 15,527.36

US Futures:

- DJI futures are currently down -127.59 points (-0.36%)

- S&P 500 futures are currently down -47.5 points (-0.32%)

- Nasdaq 100 futures are currently down -6.25 points (-0.14%)

Learn how to trade indices

Asian indices bounce as China’s regulators ‘have a word’ with banks

Asian equity markets rebounded overnight to see the arguably oversold Hang Seng (HSI) rally over 3%, after its decline stalled around 25k on Monday. The clues for today’s bounce were apparent when China’s state-run media called for ‘calmness’, hence our bias for Asian markets to bounce ahead of today’s Asian open. Hong Kong markets took the lead with the HSCE and HSI rising 3.4% and 2.8% respectively, whilst the CSI300 rose 1.4%. It has since been reported that China’s regulators have had a ‘bit of a word’ with banks (between the lines: tell them to buy stuff) which helped soothe investors nerves.

A strong pound is acting as a headwind on the FTSE 100 and helped prevent it breaking above last week’s high and cluster of moving averages. Yet the index managed to close yesterday with a small bullish inside candle which shows compression is underway, in turn indicating a burst of volatility awaits. A break above 7038.65 assumes bullish continuation (although a weaker pound could certainly help with this) but, whilst resistance caps, a move back towards 6950 cannot be discounted. A break beneath 6930 suggests 7038.65 is a swing high.

FTSE 350: Market Internals

FTSE 350: 4040.22 (0.29%) 28 July 2021

- 219 (62.39%) stocks advanced and 112 (31.91%) declined

- 25 stocks rose to a new 52-week high, 2 fell to new lows

- 78.06% of stocks closed above their 200-day average

- 89.17% of stocks closed above their 50-day average

- 3.42% of stocks closed above their 20-day average

Outperformers:

- + 7.96% - Wizz Air Holdings PLC (WIZZ.L)

- + 7.84% - 4imprint Group PLC (FOUR.L)

- + 6.95% - Fresnillo PLC (FRES.L)

Underperformers:

- -11.9% - RHI Magnesita NV (RHIM.VI)

- -5.28% - Tyman PLC (TYMN.L)

- -3.63% - Vesuvius PLC (VSVS.L)

Forex: GBP trend defies rising Covid cases

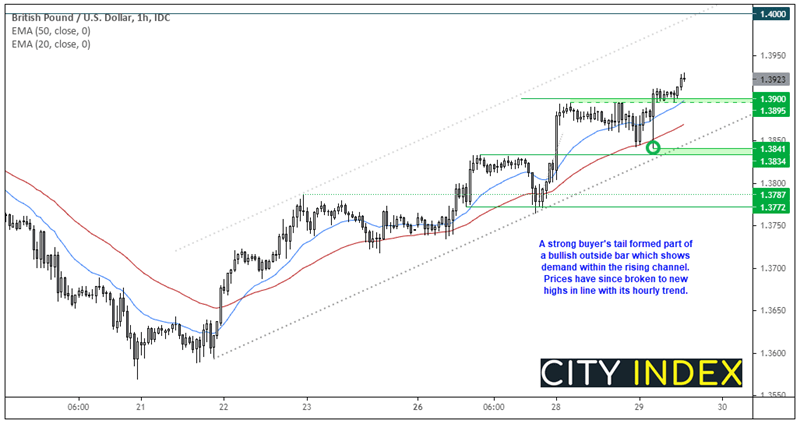

Our bias for GBP/USD to break above the June high materialised in the second half of overnight trade. We had hoped it would occur after the FOMC meeting, but there you go. But what the meeting did provide was a strong ‘buying tail’ on the hourly chart, which means prices were originally driven towards 1.3834 support before reversing sharply higher and closing the bar with an elongated bullish outside candle. Ultimately it shows demand at lower levels within the bullish channel.

Prices broke out of a small bullish flag at the highs which places support around 1.3895. We’d like to see prices hold support and continue higher but, we do have the European open to survive, and the usual pattern of late has been for prices to be driven lower before pushing onwards and upwards for the day. Therefore, our bias remains bullish above the 1.3841 high and / or the lower trendline, with 1.400 being the next major target.

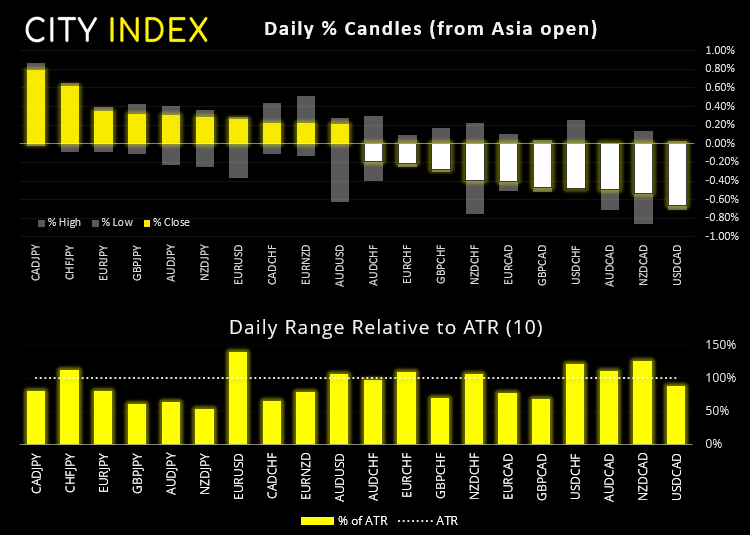

The US dollar is the weakest major overnight, and the Canadian dollar is the strongest, supported by hot (but not too hot inflation) and elevated oil prices. Should sentiment remain buoyant then CAD/JPY could be one to watch for a potential breakout above 88.0.

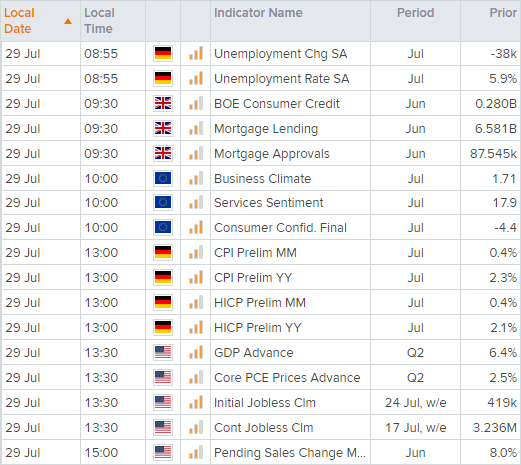

Preliminary GDP for Q in the US is the main calendar event. Depending on which source you look at, annualised GDP is estimated to land anywhere around 5.4% to 8.6%, compared with 6.4% in Q1. Interestingly the Atlanta Fed’s GBPNow model estimates GDP to remain at 6.4% as of yesterday’s close, which has fallen from an estimate of 7.4% just the day before. If there’s anything these numbers have in common it’s that they don’t agree on that today’s print is likely to be. So perhaps the key here is to see where it lands relative to Q1’ 6.4%.

Learn how to trade forex

Commodities: Copper holds steady at support ahead of U Q2 GDP

Gold prices rose to a 7-day high yet found resistance around 1818. We suspect there could be some more upside.

We’re also keeping an eye on the Thomson Reuters CRB commodity index. It is coiling just off its 4-year high and a small bullish inside candle formed yesterday above 217.72 support. If it breaks higher then great, but we’d still be interested in low volatility dips beneath key support due to its long-term uptrend. Today’s GDP print could be key to how it (or commodities in general) behave.

Copper futures have fallen for two days and retested its breakout level of 4.435. Whilst there’s no immediate sign of a swing low the potential for one to form remains. A strong GDP print could certainly help with that outcome.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest FTSE 100 articles

July 10, 2024 11:55 PM

July 4, 2024 11:00 AM

June 19, 2024 12:00 PM

March 11, 2024 04:30 PM