Asian Indices:

- Australia's ASX 200 index fell by -17.2 points (-0.23%) and currently trades at 7,517.70

- Japan's Nikkei 225 index has risen by 321.91 points (1.14%) and currently trades at 28,410.97

- Hong Kong's Hang Seng index has risen by 159.36 points (0.62%) and currently trades at 26,038.35

UK and Europe:

- UK's FTSE 100 futures are currently up 28.5 points (0.4%), the cash market is currently estimated to open at 7,148.20

- Euro STOXX 50 futures are currently up 28 points (0.67%), the cash market is currently estimated to open at 4,224.41

- Germany's DAX futures are currently up 68 points (0.43%), the cash market is currently estimated to open at 15,903.09

US Futures:

- DJI futures are currently up 39.11 points (-0.11%)

- S&P 500 futures are currently up 29 points (0.19%)

- Nasdaq 100 futures are currently up 12 points (0.27%)

Learn how to trade indices

China’s equity markets higher overnight

China’s manufacturing PMI was revised lower in August, meaning the sector contracted for the first time in 16-month. Expectations were set at 50.2 with the miss being blamed on China’s strict lockdown measures in hope of achieving zero cases. Yet Asian indices recovered after a slow start, with a mixture of stronger earning, a dovish Fed and potential expectations of more stimulus form China supporting sentiment.

The FTSE 100 printed a bearish outside candle yesterday, although around of its daily range was wick (and most of it lower to show demand near the lows). Still, 7087 remains the key support level for bearish to conquer to suggest further downside towards 7,000.

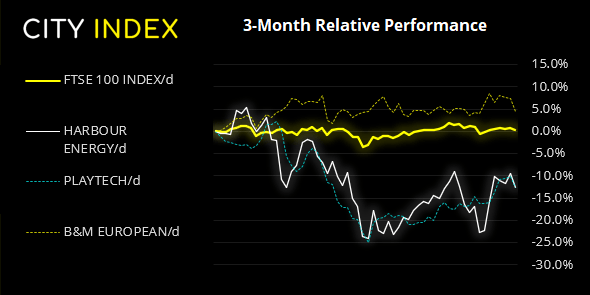

FTSE 350: Market Internals

FTSE 350: 4123.45 (-0.40%) 31 September 2021

- 191 (54.42%) stocks advanced and 147 (41.88%) declined

- 48 stocks rose to a new 52-week high, 0 fell to new lows

- 75.21% of stocks closed above their 200-day average

- 75.5% of stocks closed above their 50-day average

- 24.79% of stocks closed above their 20-day average

Outperformers:

- + 5.75% - Chrysalis Investments Ltd (CHRY.L)

- + 5.37% - Trustpilot Group PLC (TRST.L)

- + 4.04% - Trainline PLC (TRNT.L)

Underperformers:

- -3.41% - Harbour Energy PLC (HBR.L)

- -2.76% - Playtech PLC (PTEC.L)

- -2.75% - B&M European Value Retail SA (BMEB.L)

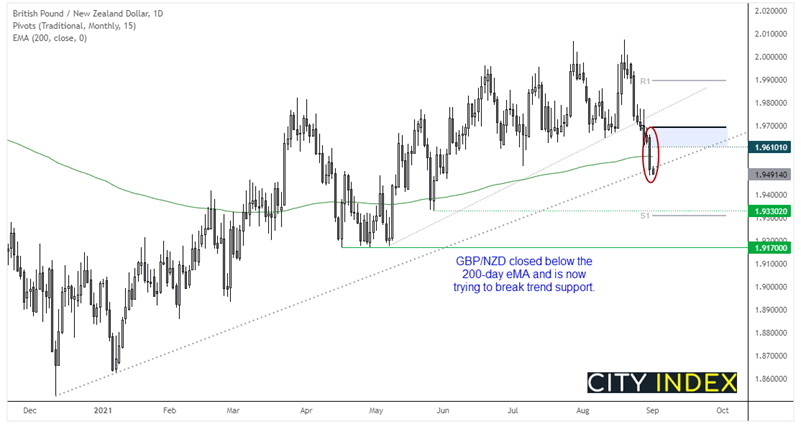

Forex: Kiwi holds onto gain, GBP/NZD probes trend support

NZD held onto yesterday’s gains and remained the strongest major overnight, although volatility across the board was low. CHF and JPY were the weakest during a noneventful session.

GBP/NZD is trying to break trend support after closing beneath its 200-day eMA yesterday. Bearish momentum has accelerated since topping out around 2.00 and, given covid cases are seemingly moving lower, we see further downside potential for the cross. As its near a trendline we can expect some volatility around it. Should prices perform a rebound we’d be interested in bearish setups below the monthly pivot at 1.9700, with the next bearish target sitting around monthly S1 and 1.9330 low.

EUR/GBP still shows the potential to break higher, despite yesterday’s minor attempt to break above 0.8594 resistance yesterday. Prices are retesting that key level ahead of the UK open.

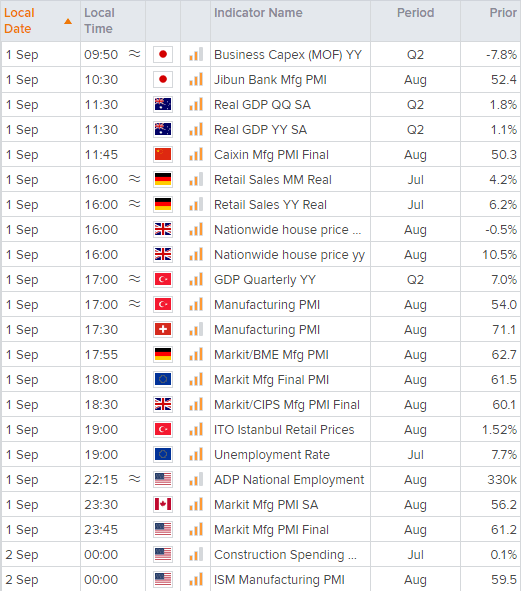

Australian GDP beat expectations, rising 0.7% in Q2 compared with 0.5% forecast, although down from 1.8%. Annualised GDP came in at 9.6%, up from 1.1% in Q2. ON the surface this seems good, until we consider the growth was slowing leading into the (now extended) lockdowns with little sign of restrictions in the two largest states being lifted. The Australian dollar was little changed

German retail sales is scheduled for 07:00 BST, although the jump in sales for June is not expected to carry over in July’s report with a forecast of -0.9%, down from 4.2%. The final read for manufacturing PMI is also released at 08:55 (with Eurozone PMI released shortly after at 09:00). As always, traders want to see a large deviation from the prior read and / or expectations for a volatility response to be expected.

As we head into the US session it is the ADP national employment report that kicks things off at 13:15, and it could sway sentient for Friday’s NFP is it comes in above or below expectations by a wide enough margin. Forecasts sits around 640k jobs to be added, which would erase the past two months of negative prints it that comes to fruition. Also that note that ISM manufacturing PMI report scheduled for 15:00.

Learn how to trade forex

Commodities: Oil prices consolidate ahead of OPEC+ meeting

Brent futures gapped lower and found support at the 200-day eMA today. The OPEC+ meeting is on today ad the consensus is for members to agree to increase output, which could place additional pressure to prices if they exceed expectations. The 200-day eMA sits around 71.51 and may prove to be a pivotal level, with resistance at 72.62 from yesterday’s low.

Copper futures are also retreating from last week’s high as it enters a corrective phase. From here we would like to see prices stabilise at or above 4.30 before reconsidering a bullish bias.

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

10.1.1

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest FTSE 100 articles

July 10, 2024 11:55 PM

July 4, 2024 11:00 AM

June 19, 2024 12:00 PM

March 11, 2024 04:30 PM