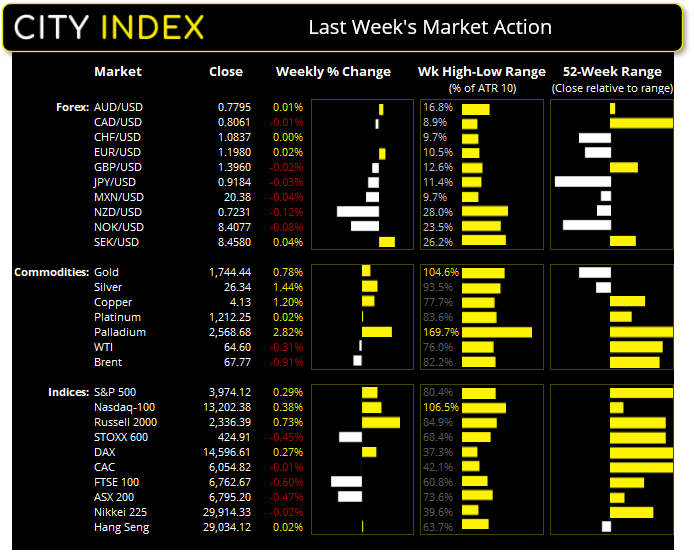

Asian Futures:

- Australia's ASX 200 futures are down -14 points (-0.21%), the cash market is currently estimated to open at 6,781.20

- Japan's Nikkei 225 futures are up 130 points (0.44%), the cash market is currently estimated to open at 30,044.33

- Hong Kong's Hang Seng futures are up 197 points (0.68%), the cash market is currently estimated to open at 29,231.12

UK and Europe:

- The UK's FTSE 100 futures are down -18.5 points (-0.27%)

- Euro STOXX 50 futures are up 15 points (0.39%)

- Germany's DAX futures are up 105 points (0.72%)

Wednesday US Close:

- The Dow Jones Industrial rose 189.42 points (0.58%) to close at 33,015.37

- The S&P 500 index rose 11.41 points (0.29%) to close at 3,974.12

- The Nasdaq 100 index rose 50.102 points (0.38%) to close at 13,202.38

Indices rally after the FOMC meeting

By raising growth and inflation forecasts yet pledging to keep interest rates low through to 2023, the Fed have maintained the perfect conditions for higher equity valuations. Whilst the dot plot showed a slight increase for an appetite to raise rates (previously it was one member expecting a raise in 2024), it fell short of fears/expectations of it happening much sooner. Read Matt Weller’s wrap on the March FOMC meeting and Joe Perry’s review of Powell’s Q&A.

The S&P 500 closed to its highest level on record at 3,974.12. Consumer cyclicals, energy and basic material sectors led the way higher, whilst utilities, healthcare and real estate were the only sectors in the red. 313 stocks in the index rose, 188 declined and 4 remained unchanged.

The Dow Jones also closed to a record high after breaking out of a small consolidation pattern on the daily chart. The bias remains bullish above 32,781 with an open upside target.

Lower bond yields allowed the Nasdaq-100 to a 2-week high and close at 13,202.38. Now back above its 10, 20 and 50-day eMA’s, the bias remains bullish above 12,997 although we now need to see prices break above 13,300 to confirm trend continuation.

Learn how to trade indices.

Forex: The dollar slumps

The US dollar index rolled over beneath 92 after failing to retest it yesterday, erasing most gains since Friday’s low and now back beneath its 10-day eMA. Interestingly this month’s high found resistance at its 10-month eMA and now trades just above the 200-month eMA after a brief hiatus above it.

Closing lower against all majors, it also had a tough time against emerging markets with USD/MXN and USD/ZAR.

- AUD/USD appears firmer ahead of today’s employment data (11:30 AEDT). Whilst a stronger print should help it trade higher in a weak USD environment, we’d want to see price break above 0.7237 resistance first before getting too bullish. At current levels, the reward to risk ratio is on the small side for bulls.

- NZD/USD formed a bullish outside (and engulfing) candle yesterday, leaving a prominent swing low at 0.7153.

- EUR/AUD remains in an established downtrend and is teasing this week’s lows with a second consecutive bearish pinbar on the daily chart. A break beneath yesterday’s low brings the 1.5253 low into focus.

Learn how to trade Forex

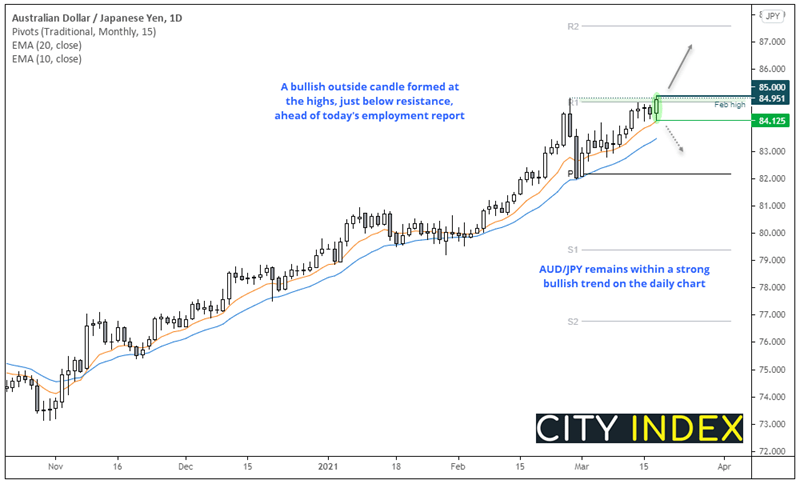

AUD/JPY is teasing its 2-year highs ahead of today’s employment data.

A bullish outside candle closed around the February high and respected the 10-day eMA, and the daily chart clearly remains in a strong bullish trend. We are now looking for a break higher on the back of a positive employment report.

- A break above 85.00 assumes bullish continuation.

- A break beneath 84.12 (yesterday’s bullish outside candle low) assumes a counter-trend move is underway.

- Whilst the monthly R2 pivot level sits at 87.60, traders can also use round numbers (86, 87) as interim targets depending on their trading timeframe.

Commodities: WTI slips further from its highs

A combination of rising US crude inventories and weaker European demand saw oil prices slip lower for a fourth consecutive session on Wednesday. Over recent days traders have digested a turn of events in Europe, with Italy planning to go back into lockdown over Easter, France imposing stricter lockdowns due to rising COVID-19 cases and Germany halting its use of AstraZeneca’s vaccine whilst cases also rise. Not to mention the slow vaccine rollout due to the European Union’s procurement red tape.

WTI teased with a break beneath Tuesday’s bearish hammer yet closed back above $65 and it’s 10-day eMA. A break below 65.13 suggests a deeper retracement. Until then we favour an upside break of its small daily triangle. Price action on Brent also looks corrective, although it trades slightly higher for the session and also holds above its 10-day eMA. A shallow retracement currently favours a retest and break above $70.

Gold closed above 1740 for the first time since March 1st, paving the way for a run towards 1760 resistance. Silver is still being silver, and trading in a seemingly ‘neither loved nor hated’ fashion, but possibly forgotten. Palladium continued to rally on supply concerns and broke to a 12-month high after being rangebound since September.

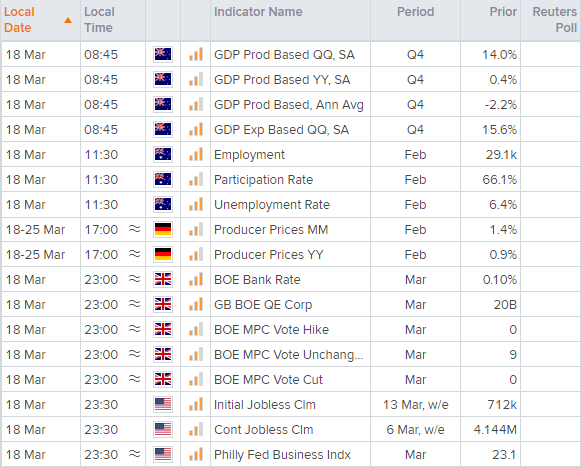

Up Next (Times in AEDT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- NZD’s Q4 GDP print is the main event in today’s Asian session. Read Tony Sycamore’s preview here: NZ Q4 GDP to showcase a two-speed economy NZD/USD

- Australia’s employment report is scheduled for 11:30 AEDT. Read Tony Sycamore’s preview here: Preview of AU jobs data and what it means for AUD/NZD

- And in the European session the BOE’s (Bank of England) policy meeting the main economic event. Read Matt Weller’s preview here: BOE preview: What’s the biggest risk for the UK economy?

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Indices articles

July 25, 2024 01:30 PM

July 25, 2024 01:01 AM

July 25, 2024 12:41 AM

July 24, 2024 07:26 PM