Monday 26th August

- German IFO Business Sentiment

- US Durable goods orders, Dallas Fed Manufacturing

Tuesday 27th August

- German GDP

- French business and consumer and sentiment

- US house prices, Richmond Fed manufacturing index,

Wednesday 28th August

- Australian construction work

- German consumer sentiment

- Eurozone money supply

Thursday 29th August

- New Zealand business sentiment

- Australian Capex

- Japanese consumer confidence

- Europe: French final GDP, German unemployment and inflation, European Sentiment Indicator

- US: GDP 2nd estimate, initial jobless claims

Friday 30th August

- South Korean industrial output

- Japanese employment, retail sales

- Australian building permits and housing credit

- German retail sales

We’ll know the outcome from the Jackson Hole Symposium

Ultimately it appears that Powell’s speech on Friday (ie later today) is the main attraction. Traders are feverishly trying to decipher whether the 25 bps cut really was just a ‘mid cycle adjustment’, or there’s further easing to come. Yet the outcome of the talks could well spill over to next week, which could make early Monday trading more interesting than usual. Particularly if Powell is more dovish on the economy, given the latest set of tariffs.

G7 Summit comes to a close

The summit takes place between Saturday and Monday, with the final two days providing closing statements from central bank heads and key figures.

- Trade is not on the agenda, yet it could well be discussed during one-one-on meetings, so any headlines over the weekend could impact markets around Asian open. Besides, it’s hard to image Trump traveling all that way without trying to throw the cat among the pigeons. Tensions have been brewing in the trade war after the Trump administration turned their attention back to Europe, so any fallout here could weigh on sentiment next week.

- An interesting side story is whether Russia will be allowed back into the G7. It’s been reported today that France’s PM Macron is on board with the idea, which gives them the weekend to lobby the idea. Although it’s more likely to flare tensions than see G7 revert to G8.

- RBA’s Philip Lowe speaks on Sunday and, whilst we doubt it will be a platform to jawbone AUD (and not that he needs to…), he’s likely to be in support of world trade given the concerns raised in RBA’s August minutes.

- Boris Johnson meets with ECB president Donald Tusk on Sunday

- Emmanuel Macron gives the closing news conference after the G7 summit on (probably Monday European time)

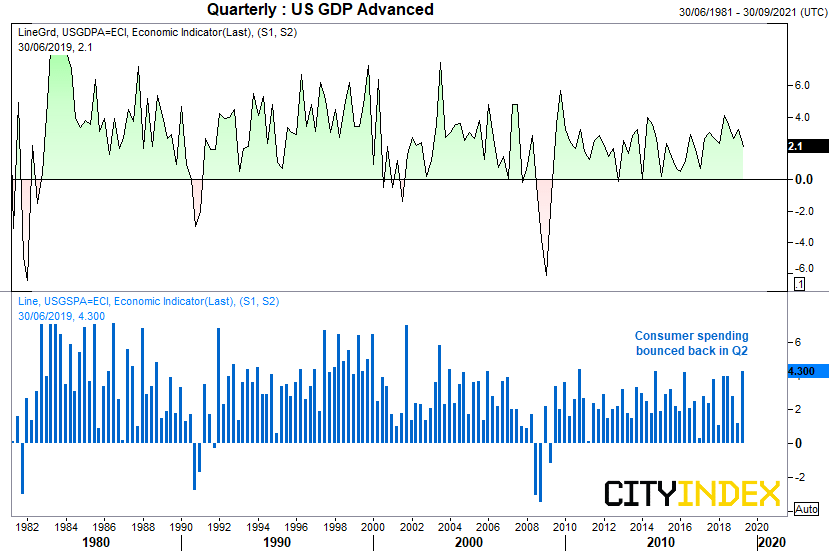

US GDP, 2nd Estimate: USD pairs, US Indices

GDP for the second quarter grew at 2.1%, not quite as slow as had been feared. Consumer spending jumped at its fastest rate since Q4 2017 (up from 1.1% in Q1) although business investment contracted by 0.6%, its first negative print since Q1 2016. If we’re to see GDP revised lower, it could weigh on UD sentiment as calls for Fed to act sooner would be in the rise again.

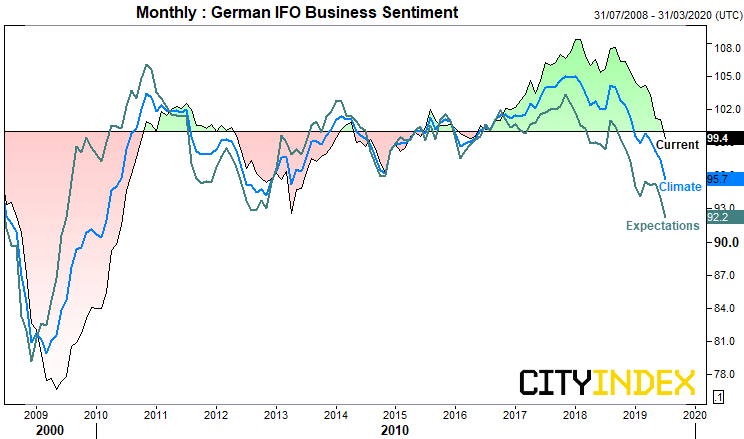

German IFO Business Sentiment: Euro crosses, DAX

Most indications for Germany are pointing towards a recession, and the IFO reads pull no punches on this. The current conditions index has weakened for four consecutive months, with July’s data contracting (pessimism) for the first time since May 2016. Yet this was to be expected, given the IFO climate index has contracted since March, is at its weakest since 2013 and IFO expectations are their lowest since 2019 (having nose dived for the past 12 months).

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Week ahead articles

Yesterday 04:48 AM

July 19, 2024 06:20 AM

July 12, 2024 01:32 AM

July 12, 2024 01:32 AM