Only a truly ‘radical’ shake-ups will stop the rot

Every silver lining…

One silver lining after HSBC’s latest quarterly earnings let down is that at least this time, the element of surprise is more nuanced. In August, when the group also missed key targets and jettisoned its CEO to boot, investors knew something must have been up. The stock lost around 7% that month and unsurprisingly had failed to regain traction by Friday’s close. The state of third quarter figures confirmed some worst fears, sending the shares down as 5%. That’s the biggest intraday drop since May, though could well have been more severe had the group not flagged in August that targets were in doubt.

Such doubts are confirmed on Monday as the revenue environment has now become “more challenging”. The key profit goal of an 11% Return on Tangible Equity (RoTE) has been scrapped whilst a warning has been given that charges are likely ahead of one of HSBC’s most radical revamps for years. Details have been deferred till the full-year earnings report, scheduled for February 2020. In the meantime, interim chief Noel Quinn had no update on whether or not he would become permanent, though noted that he had the full support of chair Mark Tucker.

The dividend will be held at its initially stated level whilst HSBC aims to maintain a Tier 1 equity capital ratio above 14%. That’s higher than the 13.5% median of Asia-Pacific peers, according to Bloomberg data.

How radical is ‘radical’?

Relative financial soundness will buy the bank some time. However, to stop the rot - which at a minimum, will see the shares deepen the year’s decline – any ‘radical’ shake-up needs to live up to its billing. For one thing, with Europe and U.S. contributing less than 10% of pre-tax profits though equating to around half of risk-weighted assets, further job cuts in the region seem almost inevitable. Yet the cut of 10,000 jobs mooted looks inadequate. True, internal and external brakes could be applied to higher headcount reductions. That could raise the risk that a new restructuring, like a similar exercise a few years ago, falls short. Disposals of the equity operations, or the French retail arm in France have also been aired, but these operations barely dent the asset base. As such would provide little financial benefit. At the same time, the truly radical step of severing incongruous Asia-Pacific and European sides remains off the cards.

On another front, outflows linked to Hong Kong unrest have been “very, very modest” so far, another silver lining. The trickle could turn into something else if the turmoil persists though. It’s another flank on which HSBC is exposed and adds to the bear case that’s been building in the shares all year.

Chart thoughts

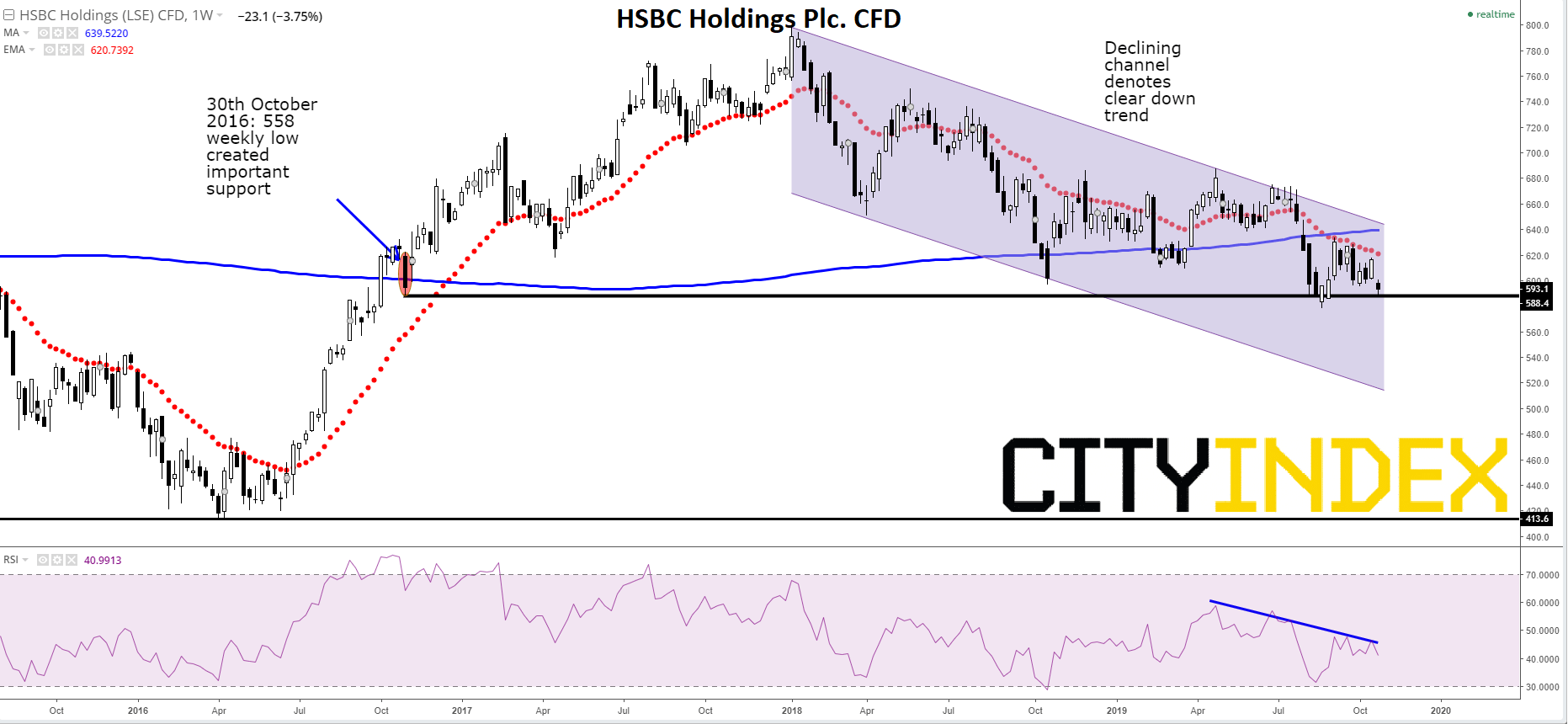

The decline from January 2018’s cycle high continues. Of most interest for the medium term: price has again approached the orbit of a vital support comprised of the low – 588.4p - during the week of 30th October 2016; the end of another troubled quarter. As the weekly relative strength index also falls in line, signifying a trend of more emphatic selling than buying, the easiest call based on momentum alone, is that the shares will see the underside of the support again very shortly. The probable importance of the threshold points to acceleration of the entrenched downtrend, if the major support were to break. Below it, the ultimate destination could be April 2016 lows around 415p.

HSBC Holdings Plc. CFD

Source: City Index

Latest market news

Yesterday 01:03 PM

Yesterday 12:52 PM

Yesterday 12:11 PM

Yesterday 07:49 AM

Latest Bank Stocks articles

October 10, 2023 09:31 AM

October 6, 2023 02:28 PM

July 17, 2023 04:03 PM

July 11, 2023 02:28 PM