Key takeaways

- First big test for Netflix’s new strategy led by a crackdown on password sharing and its new advertising business

- Netflix has said revenue growth should accelerate in the second half of 2023, and analysts think subscriber additions will also speed-up

- Risk that progress with password crackdown is slower than hoped

- Advertising will be a slow burner, but has potential to provide new catalyst in 2024

- Netflix trades at a premium to rivals as the largest and most profitable streaming stock, but at a discount to the wider tech space.

- Speed of strategy will determine the reception of investors over coming quarters

When will Netflix report Q3 earnings?

Netflix will report third quarter earnings at 1300 PT on Wednesday October 18. A video interview with management will be held at 1500 PT.

Netflix earnings consensus

Netflix is forecast to report a 7.7% year-on-year rise in revenue to $8.536 billion, in-line with its guidance.

Its operating margin, its primary profitability metric, is expected to hold largely steady from the previous quarter at 22.0% and operating profit is seen rising 19.8% from last year to $1.89 billion, also bang on guidance.

EPS at the bottom-line is forecast to grow at 12.8% from last year to $3.50 thanks to topline growth combined with improved profitability.

Netflix Q3 earnings preview

This is a big quarter for Netflix as it will be the first true test of its strategy designed to stop households from the around the world from using its service for free by cracking down on password sharing and introducing new paid sharing options and its cheaper ad-supported tier.

Netflix began tightening the leash on those piggy-backing on the accounts of friends or family earlier this year. These ‘borrowers’, as Netflix calls them, are now being encouraged to set up their account, either an independent one or as an additional profile on an existing account. Either way, Netflix is making these borrowers cough-up, potentially monetising a huge number of consumers that already enjoy its platform. And it is a huge number - Netflix has previously said over 100 million households globally were getting access to Netflix for free!

Ultimately, this means many people will have been cut-off from Netflix and positioned with a choice; pay-up or lose access to its content. Netflix has said its crackdown is working across the board, although it will take several quarters for it to iron out. It will take time to encourage all these borrowers to convert and not all of them will, but it could provide a huge boost even if a minor fraction set up their own accounts.

Netflix has said the password crackdown and paid sharing options should lead to an acceleration in revenue growth in the second half of 2023.

The ad-supported tier may take more time to really make an impact and could be more of a slow-burner. Still, Netflix needs to scale-up quickly if it wants to attract marketing dollars in a competitive environment and is aiming to generate at least 10% of its overall revenue from adverts in the future.

While not as immediate as some may hope, this means it has a potential new catalyst to provide fresh momentum further down the line. Advertising will be a bigger theme in 2024 and won’t make a material contribution this year. Still, it is handy to be able to offer a cheaper tier at a time when it is trying to encourage a variety of different borrowers, from frequent users to those that dip in and out, to pay up.

Netflix has shaken up its tiers and pricing to try to ensure it has a plan suitable for everyone, ranging from as low as $6.99 to as high as $19.99 for each household in the US. This may see average revenue per member fluctuate in the near-term, but management are confident it will ultimately prove beneficial over the medium to longer term.

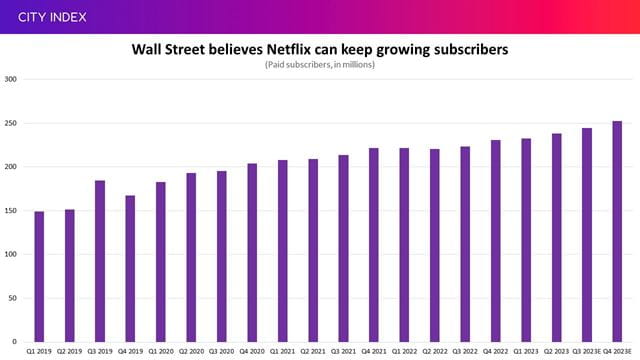

Netflix has stopped providing guidance for subscriber numbers and is now focusing more on revenue, margins and profits. Still, it is a closely-watched measure to gauge how demand is faring in light of its new strategy. Wall Street believes the crackdown will have led to faster subscriber growth in the third and see it accelerating again in the fourth. Netflix is forecast to add 6.175 million paying subscribers in the third quarter, taking its total to a new record-high of 244.5 million.

(Source: Company reports, with estimates from Bloomberg)

The outlook for the fourth quarter should see Netflix guide toward a faster pace of growth in the fourth quarter. Wall Street is looking for Netflix to target $8.8 billion in revenue (up 12% YoY) and operating profit of $1.23 billion. Any disappointment here would suggest its new strategy isn’t progressing as fast as hoped.

How will Netflix stock react?

Netflix is up 26% in 2023 and has outperformed other streaming stocks. This is because Netflix is not only the most popular platform, but the only one that is profitable. Disney’s struggle to get its streaming services out of the red has been one of the reasons the stock has lost ground this year. Netflix justifiably trades at a premium to its rivals as a result, although at a discount to the broader tech space.

The risk this season is that markets are expecting too much too quickly from the new strategy, especially on ads. The push into advertising has got markets excited but Netflix has repeatedly said it will take time for the business to build, potentially years. The password crackdown will now be the primary driver of growth over the coming quarters, although average revenue per member – which will be more closely-watched going forward – could struggle to improve in the short-term. That suggests there is room for disappointment if Netflix’s new plan doesn’t pay-off as quickly as investors hope, and that Netflix may have to over-deliver in order to really impress.

Meanwhile, other headwinds linger on the horizon as household budgets are tested, competition intensifies and its content slate remains under threat by ongoing strikes in Hollywood.

Where next for NFLX stock?

Netflix shares have been in a downtrend since peaking in July, having fallen almost 25% in less than three months! The stock has sunk to its lowest level in four-and-a-half months.

The stock has fallen below the 200-day moving average for the first time in 11 months and the RSI has been flirting with oversold territory for three weeks. We could see some support emerge between $356 and $348.50. A slip below this range could open the door to a sharper move toward $333.

The immediate job on the upside is to recapture the 200-day moving average, which is currently around $373. It may then need to reclaim the 20-day moving average at $380, with a chance that we could see the two moving averages crossover or converge in the near future. It needs to climb above $386 to set a new higher-high and pave the way for it to return to the upper chamber of the falling downtrend.

Wall Street sees significant upside potential for the stock over the next 12 months on the belief that its new strategy will provide the growth it needs to keep its valuation alive. The 44 brokers that cover Netflix, according to a Refinitiv-compiled consensus, currently have an average target price of $464.50, some 25% higher than current levels.

Nasdaq 100 analysis: Where next?

Netflix is among the top 20 stocks that carry the most weight in the Nasdaq 100, making it in the index to watch ahead of the results. It is also likely to spur a reaction in other streaming stocks such as Disney, Paramount and Warner Bros Discovery.

Let’s dive into the index. We can see an interesting setup in play at the moment, with the index currently pinging between a narrowing wedge. We saw it test the falling trendline at 15,333 yesterday and any move above that resistance would be bullish and allow it to target 15,500 and then the September-high at 15,600.

We can see the index has now climbed above all its moving averages this week and a convergence of the 50-day and 100-day moving averages at around 15,000 may help provide some support, although the rising trendline that can be traced back to 2022 remains the key level to watch.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM