Key takeaways

- Netflix is among the best performers in the Nasdaq 100 this year after recovering from the selloff we saw in 2022.

- Subscriber growth is back on the right trajectory, with its dual-push to revive growth through its new ad-supported tier and crackdown on password sharing.

- Markets hope this will be the trough for earnings and believe a recovery in the second half will be enough to let Netflix deliver record earnings in 2023!

- Password policing to have a more immediate impact, with its ad-supported tier likely to provide more of a boost later this year and help boost margins

- Rosy outlook should be supportive for Netflix stock if it can keep up with optimistic market expectations.

- Netflix valuation multiples have more than doubled and sit at a large premium over rivals, but this has been earned as Netflix is the only profitable pure-play streaming stock.

Netflix Q2 earnings date and time

Netflix will report second quarter earnings after US markets close on Wednesday July 19, at 1300 PT. A video interview with management will be made available on the same day at 1500 PT, when they will respond to questions submitted by investors ahead of the event.

Netflix Q2 earnings consensus

Netflix is forecast to report a 3.7% year-on-year rise in revenue in the second quarter to $8.265 billion and an 11.1% decline in EPS to $2.85, according to consensus numbers from Bloomberg.

Netflix Q2 earnings preview

Netflix has rallied over 48% since the start of the year as the streaming giant regains the confidence of the markets with its plan to revive growth and improve profitability through its crackdown on password sharing and its new ad-supported tier.

That has put it among the top performers in the Nasdaq 100, but it is still trading around half the value compared to when it peaked in late 2021 when markets went on an over-zealous buying spree after subscribers surged during the pandemic, only for growth to become slower and more volatile as that demand unravelled when lockdown restrictions were removed.

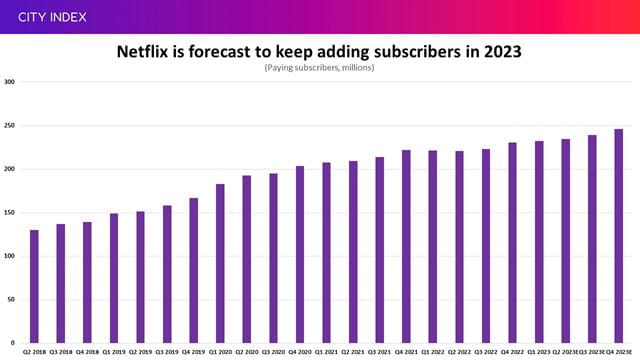

Netflix’s subscriber growth is back on the right path following the ups and downs we saw in 2022. It is expected to have added 1.8 million net new subscribers during the second quarter to end June with 234.3 million of them on its books. Netflix is no longer providing formal guidance for subscriber growth going forward but it may provide some commentary. Markets anticipate we will see a notable acceleration in subscriber growth in the second half, with consensus figures suggesting it can end 2023 with a record 245 million users.

What investors will want to know is how many additions are stemming from its new strategy. The crackdown on password sharing, underpinned by stricter procedures to contain accounts to one household and encouraging those piggy-backing to sign-up through a new paid sharing option, is likely to be a bigger driver in the near-term because it has a more immediate impact. Netflix delayed the bulk of the rollout to the second quarter but it is now live in over 100 countries, so this will be the first update on what the initial effect has been. It has already warned that some of the boost provided from password sharing will be pushed into the third quarter because of the delay. It may lose some users as a result of the plan, but there are over 100 million households using Netflix without paying for it and that is a huge pool that can contribute significantly to growth even if only a minority convert.

Meanwhile, Netflix has previously said its ad-supported tier could be a slow burner that starts to really kick in later this year, but any signs it is already finding significant momentum would be very well-received by the markets and could lead to estimates for the remainder of the year being upgraded. Netflix revealed for the first time that five million subs had signed up to its ad-supported tier back in May, suggesting there is appeal for a cheaper option in the current environment.

The fact Netflix has two substantial new catalysts to help keep subscriber numbers climbing to new record highs suggests there is an opportunity for a beat this quarter. On the other hand, a miss would suggest the new plan isn’t taking-off as quick as markets have been banking on this year.

The new strategy is also key for Netflix’s hopes of restoring margins. It has already revealed that it is earning more revenue from each US user on its ad-supported tier than it does from those paying for their subscription. That’s not only good for revenue growth but also profitability, and demonstrates that advertising could be a highly lucrative market for Netflix.

Netflix is expected to report an operating margin of 19.1% in the second quarter, in-line with its guidance but down from 20% the year before, mainly because of the negative impact of a stronger US dollar. Netflix has got a tight grip on costs over the past year, with expenses rising at low single-digit rates compared to the 20%-plus rises we saw consistently in 2021 and early 2022. That discipline, combined with the higher margins coming form its ad-supported tier, bode well for Netflix’s margins. It is aiming for a margin of 18% to 20% over the full year and markets think it will land in the middle of that range, which would mark an improvement from the 17.8% seen when margins took a hit in 2022.

That means revenue and subscriber growth are both set to accelerate in the second half and profitability is improving. Earnings are forecast to decline for a fourth consecutive period in the second quarter but markets believe it will start to reap rewards in the second half and that EPS will begin to grow again, partly helped by easier comparatives from what we saw in the back-end of 2022 – enough so that it is forecast to report record annual earnings in 2023 despite the pressure seen on the bottom-line in the first half. Netflix is also aiming to generate at least $3.5 billion of free cashflow in 2023, having raised its goal from $3 billion in the last quarter. That would be more than double the $1.6 billion reported in 2022.

All of that has the potential to keep providing Netflix shares with momentum, but only if it can keep up with market expectations. Markets have bought into Netflix’s new strategy and now it is time to start delivering. Netflix’s valuation multiple has risen to around 33x forward earnings compared to just 15x at the start of the year. That is a significant premium over its rivals like Paramount and Disney, but one hard-earned as the only profitable pure-play streaming stock out there.

Netflix’s valuation multiple is still considerably lower than we saw before the pandemic, when it was solely underpinned by its growth potential. However, we are unlikely to see a return to those lofty levels now that Netflix is leaning more toward maximising revenue and profitability to counter slower, but hopefully steadier, growth.

DIS stock: Is Disney a takeover target?

Disney, equipped with its namesake streaming channel as well as Hulu and ESPN+, has emerged as Netflix’s biggest rival on the stock market in recent years. The House of Mouse’s decision to enter streaming originally helped propel the stock but the opposite has been true since markets became less concerned with growth and more worried about profits, with Disney now racing to make its streaming operations profitable.

Disney experienced the same rout as Netflix in 2022 as markets sold tech stocks in their droves but it has not experienced the rebound like its rival this year because its streaming operations are now seen as a drag on the bottom-line (especially as Disney+ has also been losing subscribers this year) while concerns are growing over its theme parks and resorts as recession risks rise. Disney shares are up just 1.7% this year and it is trading at less than 19x forward earnings, almost 40% below its five-year average and at an even steeper discount compared to Netflix.

That has prompted another round of takeover rumours, fuelled by Needham analyst Laura Martin predicting this week that Disney will be sold within the next three years. The analyst has touted a potential sale of Disney before and proven incorrect, but it has once again reignited discussions about what company could be interested. Apple, as was the case in the past, has been touted as a potential frontrunner on theories it could leverage Disney’s world-class content with its growing services business and two billion installed devices. However, recent regulatory probes suggest any company large enough and rich enough to afford to take on Disney could face a tough time convincing regulators.

Where next for NFLX stock?

Netflix shares have risen over 52% since the start of 2023, putting it in the top 15 performers in the Nasdaq 100 this year.

The streaming giant has found it more difficult to find higher ground over the past month, but it has managed to keep up the momentum and the stock is currently at 17-month highs after returning above the $450 threshold.

The next upside target is $457, representing the peak we saw in February 2022, before the 61.8% retracement at $490 is on the radar.

On the downside, we have seen the 50% retracement from the lows we saw over a year ago of $429 provide some support over the last three weeks, although the last low of $417 remains in play. Any slip below here risks seeing it fall back toward the 38.2% retracement at $367, supported by the supportive trendline that has been in the works for over a year. The RSI remains on the cusp of overbought territory to suggest it may become harder to climb from here.

Nasdaq 100 analysis: Where next?

The Nasdaq 100 has climbed to 18-month highs, fuelled by easing inflation and hopes that interest rates are approaching their peak.

The rally has taken the index firmly over the 78.6% retracement and has opened the door for the index to keep climbing back toward the all-time highs we saw in late 2021 if it can keep up the momentum. We could see 15,650, marking the level of resistance seen in September 2021, act as a midway target.

The RSI is once again in overbought territory to suggest we could see some pullback before more gains are made. The 78.6% retracement at 15,300 should provide some support if it comes under pressure but any slip below here risks a sharper decline toward 14,300, in-line with the 50-day moving average and the 61.8% retracement. Notably, volumes have been broadly declining over the past month.

Take advantage of extended hours trading

Netflix will release earnings after US markets close and most traders must wait until they open before being able to trade. But you can get ahead of the game by taking a position in premarket hours by taking advantage of our service that allows you to trade Netflix and other tech stocks using our extended hours offering.

While trading before and after hours creates opportunities for traders, it also creates risk, particularly due to the lower liquidity levels. Find out more about Extended Hours Trading.

How to trade Netflix stock

You can trade Netflix, Disney and the Nasdaq 100 with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the stock or index you want in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Or you can practice trading risk-free by signing up for our Demo Trading Account.

Latest market news

Today 01:39 PM

Today 11:05 AM

Today 10:46 AM

Today 05:56 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM