When will Big Tech stocks report earnings?

Big Tech earnings season will kick off on Tuesday January 24, when Microsoft will be the first to release its quarterly update before it rivals report the following week. Click to find out more about earnings season and how to read earnings reports.

|

Company |

Quarter |

Date of earnings |

|

Microsoft |

Q2 |

January 24 |

|

Meta |

Q4 |

February 1 |

|

Alphabet |

Q4 |

February 2 |

|

Apple |

Q1 |

February 2 |

|

Amazon |

Q4 |

February 2 |

Big Tech stocks: Where’s the value?

Big Tech stocks saw their valuations explode during the pandemic, when demand for tech boomed. We have seen their valuations fall back since then after the selloff that took hold last year, but most of Big Tech still boast lofty valuations that are still above the average of the S&P 500. Advertising-reliant stocks Meta and Alphabet are the exception considering their valuations are sharply lower than their historic averages as well as the market average.

|

Company |

P/E Ratio |

2-yr Average |

5-yr Average |

|

Microsoft |

22.9x |

28.8x |

27.4x |

|

Meta |

13.2x |

16.9x |

18.8x |

|

Alphabet |

15.8x |

20.9x |

21.0x |

|

Apple |

21.3x |

25.7x |

21.7x |

|

Amazon |

36.0x |

44.2x |

50.3x |

|

S&P 500 |

19.4x |

24.2x |

22.2x |

(Source: Bloomberg)

Big Tech earnings consensus

Every single member of Big Tech is expected to report lower earnings this quarter. Below is a table outlining market expectations in terms of both revenue and earnings growth for this quarter.

|

Company |

Revenue |

EPS |

|

Microsoft |

2.4% |

-6.9% |

|

Meta |

-6.3% |

-38.7% |

|

Alphabet |

1.9% |

-13.4% |

|

Apple |

-1.5% |

-6.9% |

|

Amazon |

6.0% |

-83.0% |

(Source: Bloomberg)

Big Tech earnings: What to expect this season

This will be one of the toughest earnings seasons for Big Tech on record, dominated by slowing sales and declining earnings.

Growth prospects, which underpin their valuations, still look bleak in the short term as rising inflation and higher interest rates pressure spending by both consumers and businesses, which are tightening their belts in fear a recession is just around the corner. Inflation has eased since peaking last year but remains well above the Federal Reserve’s 2% target and, as a result, interest rates are set to continue climbing before being held at higher levels.

That has weakened demand for everything from tech and online shopping to cloud computing and advertising, weighing on the topline, while rising costs continue to eat away at earnings. In response, we are seeing a broad push to cut costs, including thousands of layoffs that could deepen in 2023 as Big Tech looks to protect profitability and weather the storm.

Microsoft

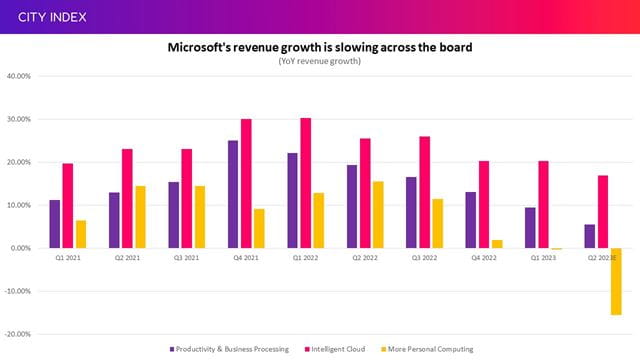

Microsoft is expected to report its slowest topline growth in over five years and the first drop in earnings in over eight years when it releases results covering the second quarter of its financial year.

Wall Street forecasts that Microsoft will report a 2.4% year-on-year increase in revenue to $52.97 billion. Sales growth is slowing across the board. Growth peaked in mid-2021 for its cloud computing and software divisions but both have been suffering a slowdown since then, while its hardware unit responsible for computers, games consoles and Windows is forecast to fall for a second consecutive quarter. That shows that demand for everything is waning.

(Source: Company reports, with estimates from Bloomberg)

The slowdown in growth from Productivity & Business Processes will be driven by softer demand for its suite of office products and its job-focused social media platform LinkedIn. The fact Intelligent Cloud is also slowing down shows business spending is taking a hit in the current environment. More Personal Computing will be the biggest drag as sales of both its Windows operating system and its devices are forecast to fall by double-digit percentages.

Meanwhile, EPS is expected to drop 6.9% to $2.31 as costs continue to rise at a faster pace than revenue, with operating expenses forecast to be up 3.1% from last year this quarter to squeeze its margin.

In response, we could see Microsoft take more drastic action to reduce spending. Sky News has reported Microsoft is preparing to axe around 5% of its 220,000-strong global workforce, which could see around 11,000 workers culled. The report said the number of layoffs could be even higher and that an announcement about reducing headcount would likely come before it releases its earnings.

Meta

Meta was the big loser in 2022 as the slowdown in demand for advertising hit social media stocks hard, which saw it lose almost two-thirds of its value last year. Its lowly valuation has attracted buyers back into the market and seen it regain significant ground, but is still worth just a fraction of its valuation this time last year.

Meta is expected to report its third consecutive quarter of lower sales and the fifth straight quarter of lower earnings when it reports results. Wall Street forecasts Meta will report a 6.2% year-on-year decline in revenue in the fourth quarter to $31.57 billion while EPS is expected to plunge over 38% to $2.25.

The slowdown in advertising continues and that, twinned with greater difficulty in targeting ads at users following Apple’s privacy changes and a shift to less-lucrative video formats in response to more intense competition with the likes of TikTok, is impacting prices.

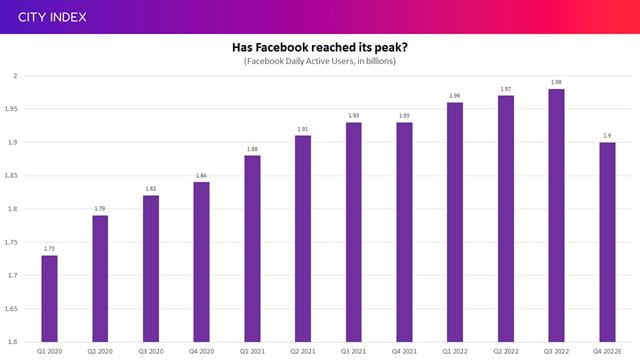

The fact markets believe Facebook will see daily active users fall to 1.90 billion at the end of 2022 from 1.98 billion at the end of September will only add to its woes and fuel further speculation that some of its social media platforms have reached their peak.

(Source: Bloomberg)

Meta has warned that earnings will remain under pressure in 2023 and markets believe they will continue to fall until the second half of the year. In response, Meta has announced it is downsizing its workforce by 13% through 11,000 job cuts. Meta’s workforce has more than doubled in size since the start of the pandemic and we are now seeing those that were the most aggressive in hiring starting to cut the fat as they try to protect profitability.

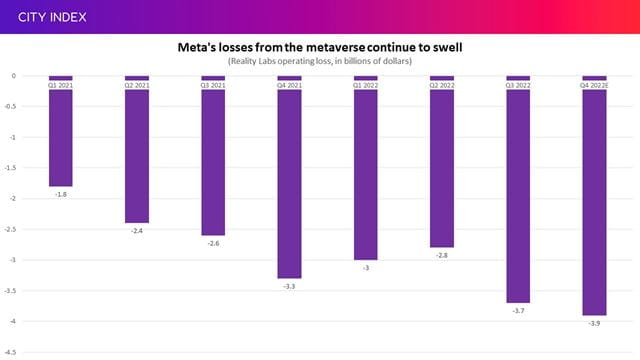

Meanwhile, Meta’s costly investment into the metaverse will continue to drag down the bottom-line further this quarter, with its Reality Labs loss forecast to come in at $3.9 billion – which would be the biggest quarterly loss on record so far. The company remains committed to its future even though its core business is under pressure, but cutting investment here would be the easiest way to protect the bottom-line without impacting the business that drives Meta today – although at risk of losing its leadership in what it believes is its new long-term opportunity.

(Source: Bloomberg)

While the metaverse continues to swallow up money without any form of return in sight for years to come, Meta has said it expects its monetisation efforts for WhatsApp and Messenger are likely to be the next major catalyst for the company.

Alphabet

Alphabet is expected to be among the minority that will keep on growing its topline this quarter, although revenue is set to rise at its slowest pace on record, while earnings are set to fall for a third consecutive quarter.

Wall Street forecasts Alphabet will report a 1.9% year-on-year rise in revenue to $76.8 billion and a 13.4% drop in EPS to $1.21.

Advertising revenue is forecast to be down 0.7% from last year. Google’s ad pricing dropped 5% in the last quarter, which showed search is proving far more resilient in the current environment compared to its social media rivals considering Meta’s prices were down by around 18%.

Meanwhile, its services unit that homes everything from the Google Play Store to other services like its Android operating system is expected to see revenue decline 0.5%. YouTube, which reported a surprise fall in sales in the last quarter, is expected to drop 4.2%.

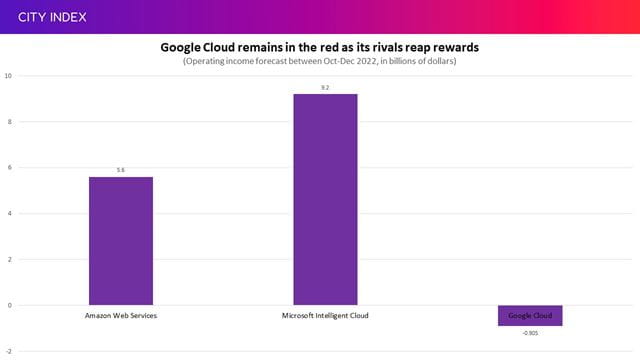

The saving grace will be Google Cloud, which is forecast to report a 30% jump in sales this quarter. While welcome, that will mark a major slowdown from what has been delivered in recent years. More importantly, while its cloud computing operations are helping prop up the topline it is still deep in the red whilst its rivals Amazon and Microsoft are both reaping massive profits from their respective cloud operations.

(Source: Bloomberg)

In response to the tougher environment, Alphabet has announced plans to layoff 12,000 workers, representing over 6% of its workforce. CEO Sundar Pichai said the company had grown rapidly in recent years ‘for a different economic reality than the one we face today.’ Alphabet’s workforce has almost doubled since the start of the pandemic.

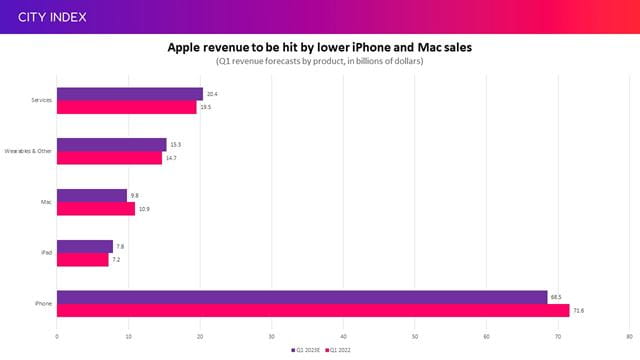

Apple

Apple proved to be more resilient than its Big Tech peers in the last quarter, but the situation has become more challenging for the iPhone maker since then as it tries to navigate supply chain problems and softening demand.

Wall Street forecasts revenue will fall 1.5% from last year to $122.06 billion in the first quarter of the financial year, which is typically its best quarter for sales of the year thanks to the holiday shopping season.

That would be the first fall at the topline in over three years, driven by the drop in iPhone and Mac sales as supply chain challenges and softer demand for devices bites. That is set to be enough to offset higher demand for iPads, its wearables and other devices, and services.

(Source: Bloomberg)

That would also mean Apple won’t be reporting sales growth over the so-called Golden Quarter for the first time since at least the start of the millennium. The debate now is how many of these sales will be pushed into 2023 and how many will be lost entirely. The longer it takes to iron out production problems, the higher the risk that shoppers will wait for the next iPhone to be launched in 2023 or turn to models offered by competitors.

Apple has trimmed its outlook by 3 million handsets in response to softer demand and supply chain constraints in China, but some analysts believe the impact could be greater. Lower-end models are not as in-demand as first hoped while premium-end models like the Pro and Pro Max have been hit by bottlenecks that could have seen supplies lag demand over the key quarter.

Its largest supplier Foxconn said the biggest iPhone factory has ‘basically returned to normal’ in January after suffering from Covid-19 disruption and worker unrest in December. In response, we have seen Apple continue to shift more production out of China and into countries like India, while also diversifying its supplier base to wean itself off relying so heavily on companies like Foxconn.

Earnings are also under pressure as costs continue to climb and sales fall, with operating expenses forecast to jump over 15% from last year in the quarter. EPS is expected to fall 6.9% to $1.95 as a result. Apple wielded its healthy cash balance last year and accelerated share buybacks to help support the bottom-line, a tactic it could continue to deploy should it want to capitalise on the drop in its share price and bolster EPS.

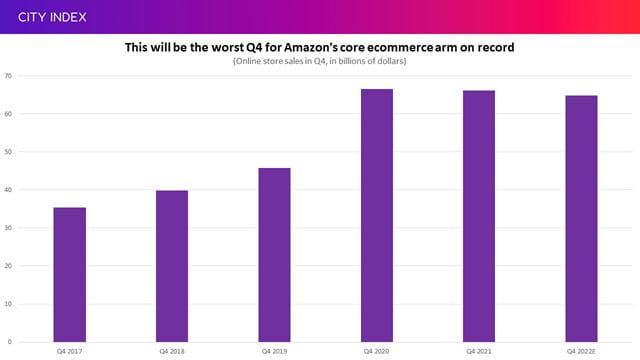

Amazon

Wall Street forecasts Amazon will report a 6% year-on-year rise in revenue in the fourth quarter to $145.7 billion (at the upper end of its $140 to $148 billion guidance) as weakness in its core ecommerce unit is countered by growth from its cloud computing arm Amazon Web Services, its subscriptions business underpinned by Prime, and its small but fast-growing advertising arm.

It has already admitted that revenue will experience its slowest growth on record for any holiday shopping season. This will be mainly driven by ecommerce, which is set to see its second consecutive year of lower revenue in the fourth quarter as the boom in demand for online shopping during the pandemic continues to unwind.

(Source: Bloomberg)

(Source: Bloomberg)

Meanwhile, EPS is expected to plunge almost 85% from last year to $0.21. Amazon has said operating income, which is its headline earnings measure, will be between breakeven and a $4 billion profit. Analysts are expecting $2.6 billion, according to the consensus, which would be down almost 26% from last year.

It is important to remember that Amazon Web Services generates the bulk of profits needed to fund its array of other operations. The unit is expected to report a 22.7% year-on-year rise in sales to $21.8 billion and, while strong, that will mark the fifth consecutive quarter of slower growth. The fact both AWS and Microsoft’s cloud computing units both missed expectations in the last quarter suggests the entire industry is cooling down as businesses delay investment and pullback on spending in response to the tough macroeconomic conditions. Topline growth at AWS is forecast to slow further in 2023 to below 20%. Rising costs for the likes of energy is also pressuring margins, which are forecast to fall just below the 26% mark this quarter, which will be the lowest on record in over three years.

Amazon is trying to cut costs in response to rising costs across the business, from energy to fulfilment. Total costs and expenses are forecast to be up 6.9% from last year, outpacing the topline. The company only trimmed $1 billion of costs off its books in the last quarter, below its $1.5 billion target. However, we could see better progress made on this front going forward considering Amazon has announced it is making 18,000 jobs cuts starting this month. Amazon, which is much more labour-intensive than its rivals, has seen its overall workforce more than double in size since the start of the pandemic but now, with earnings under pressure, Amazon is having to reverse this and start trimming the fat. Still, the 18,000 roles represent just 1.1% of its total employees, but around 5% to 6% of its 300,000 to 350,000 corporate workers.

Take advantage of extended hours trading

Big Tech stocks tend to release earnings after US markets close and this means most must wait until they reopen the following day before being able to trade. But by then, the news has already been digested and the instant reaction in share price has happened in after-hours trading. To react immediately, traders should take their positions in pre-and post-market sessions.

With this in mind, you can take advantage of our service that allows you to trade Big Tech stocks using our extended hours offering.

While trading before and after hours creates opportunities for traders, it also creates risk, particularly due to the lower liquidity levels. Find out more about Extended Hours Trading.

How to trade Big Tech stocks

You can trade Big Tech stocks with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the stock you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Or you can practice trading risk-free by signing up for our Demo Trading Account.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM