Key takeaways

- Big Tech has outperformed the wider market in 2023 and could come to the rescue again this earnings season

- Forecast to return to earnings growth this quarter while the broader S&P 500 is set to see its sharpest drop in three years

- Easier comparatives coming into play and will flatter results in the second half

- Cost-cutting and layoffs are starting to pay off

- AI catalysts do not appear to have been priced-in and are yet to provide major catalysts for the group of five

- Higher valuation multiples and uncertain economic outlook will make gains harder to come by in the second half,but Big Tech is likely to keep outperforming

Big Tech financial calendar

Below is a calendar outlining when each Big Tech stock is scheduled to report:

|

Company |

Quarter |

Date |

|

Microsoft |

Q4 |

Tuesday July 25 |

|

Alphabet |

Q2 |

Tuesday July 25 |

|

Meta |

Q2 |

Wednesday July 26 |

|

Amazon |

Q2 |

Thursday July 27 (TBC) |

|

Apple |

Q3 |

Thursday August 3 |

Big Tech earnings consensus

Below is table showing consensus figures for each company’s headline earnings per share figure for the most recent quarter:

|

Headline EPS |

Year ago quarter result |

Consensus for this quarter |

YoY Growth |

|

Apple |

$1.20 |

$1.20 |

0.2% |

|

Microsoft |

$2.23 |

$2.55 |

14.5% |

|

Meta |

$2.46 |

$2.92 |

18.6% |

|

Alphabet |

$1.21 |

$1.32 |

9.1% |

|

Amazon |

($0.20) |

$0.35 |

- |

(Source: Bloomberg)

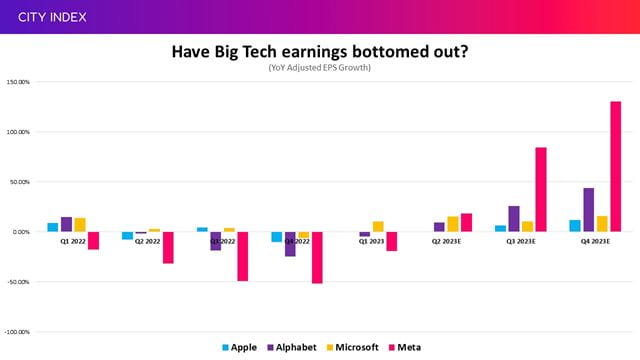

Growth, however varied across the group, will be welcomed considering profits have been falling over the past year. Earnings growth is expected to accelerate significantly in the second half, according to analysts, partly because they will face easier comparatives.

(Source: Company reports, with estimates from Bloomberg)

Wall Street has incorrectly predicted that earnings have bottomed-out in recent quarters, although the easier comps suggest this is less likely this time around. Still, they should be taken with a pinch of salt considering the performance of markets could still be largely at the behest of macroeconomic conditions.

Confidence is growing that interest rates are approaching their peak after inflation slowed in June while a cooling – but far from faltering – jobs market is providing hope that the US can avoid a severe recession. But the fight against inflation is far from over, a pivot won’t happen until 2024 at the earliest and a downturn is still on the cards. This threatens the optimism surrounding the second half and poses a risk to estimates.

Microsoft stock: Q4 earnings preview

Microsoft has the potential to be the standout performer this earnings season thanks to its diversified business model and leadership in artificial intelligence. Microsoft has reliably grown earnings over what has been a tumultuous few years for most and adjusted EPS is forecast to rise 14.5% to $2.55 this quarter, marking the fastest growth in over 18 months.

Revenue is forecast to be up 6.9% at $55.5 billion. Hardware remains under pressure, although we could see the first rebound in gaming in six months. This will be countered by healthy demand for its array of software, particularly its Office suite of products, and its cloud computing services. Both of these are vital to day-to-day operations for many, but they growth has slowed as businesses trim their budgets and consumers tighten their belts. The brakes are also being applied to LinkedIn, despite a resilient jobs market.

Meanwhile, Microsoft appears to be taking a lead on AI thanks to its relationship with OpenAI, the company behind ChatGPT. Not only is it already running generative AI workloads from ChatGPT on its cloud computing network, but it is also preparing to unleash new commercial tools that could provide major new revenue streams. Microsoft said it will charge $30 per month, per user for corporate customers for its new artificial intelligence products. The suite of products, named Microsoft 365 Copilot, will cost $30 per user each month. Barclays said this was higher than expected and described it as ‘a major next step for Microsoft’s AI monetisation’. Bernstein agreed and said it could set the gold standard for other companies. Analysts are bullish on demand in spite of the price tag due to the potential productivity gains on offer.

Microsoft shares have also found support lately as the regulatory hurdles facing its $69 billion acquisition of video game maker Activision Blizzard are falling away. They have had to extend the deadline in order to get things tied-off, but remain committed to the deal. As a result, Activision Blizzard shares have not traded this close to the $95 offer price in two years, showing markets have become increasingly confident that the deal can get done.

Alphabet stock: Q2 earnings preview

Alphabet, despite jumping almost 40% in 2023, has underperformed its rivals and continues to trade at a discount due to its reliance on advertising and its failure to convince the markets that AI is a major opportunity rather than a threat.

Encouragingly, revenue growth is forecast to accelerate for a second consecutive quarter and earnings are set to return to growth after a year of declines thanks to easier comps and milder cost pressures, with adjusted EPS estimated to rise 9.1% to $1.32. Revenue is forecast to rise 4.4.% to $72.7 billion. Ad sales on Google are expected to be up 1.8% while YouTube is forecast to see a more tepid rise of 0.9%.

Google Cloud should produce its second consecutive quarter of operating profits, marking an achievement that has been aptly timed considering it too has seen a slowdown in growth as companies become more stringent with spending. It is estimated to report a $142 million profit in the second quarter following the $191 million we saw in the first. This will support margins and markets would welcome any signs Google Cloud is on will start significantly contributing to the bottom-line. Still, it remains far behind rivals Amazon and Microsoft, which both boast larger and far more profitable cloud computing businesses.

Alphabet has so far failed to get markets excited about its AI prospects as markets ponder whether the breakthrough technology is a huge opportunity or threat to Google. Microsoft has already declared war on Google after reviving its Bing search engine and infusing it with new AI tools from ChatGPT. Risks posed from AI are very real, but Alphabet has been among those working on AI for the longest. Now it needs to show it can be a leader in the space and convince markets that AI will be a catalyst. It recently merged its DeepMind and Brain units together and it has recently relaunched its Bard AI chatbot in Europe after addressing security concerns, while also introducing it into other countries like Brazil.

Meta stock: Q2 earnings preview

This could be a big quarter for Meta, and one that could be needed to maintain the stellar gains booked in 2023 following the heavy selloff we saw last year. Earnings are forecast to grow for the first time in 18 months, its new Threads platform is taking off, and there is a chance Meta could stir up some excitement about its AI prospects.

Revenue is expected to rise 7.7% in the second quarter to $31.1 billion as it starts to come up against easier comparatives. Meta has done well to keep engagement going but is still suffering from lower prices as fewer businesses splash out on advertising.

Meta was the first to start making job cuts last year and was one of the most aggressive when it came to cost cutting, having become bloated during the pandemic. That is now starting to pay off as costs are expected to grow at a slower pace than sales for the first time in two years! As a result, adjusted EPS is forecast to increase 18.5% to $2.91.

Meta continues to spend big on its metaverse ambitions, having refused to pullback despite the pressure on earnings over the past two years. Its Reality Labs arm that homes these activities is forecast to report an operating loss of $3.7 billion. That will be higher than last year but down from the peak we saw at the end of 2022.

We are also likely to get some more insight into its new social media platform Threads, which has already secured over 100 million users. It is the fastest-growing app of all time, although this was helped by the fact Meta leveraged the existing user base on the already established Instagram. Threads, designed to compete directly with Twitter, could provide a major new catalyst if it takes off.

Meta could invigorate some excitement around its AI prospects amid reports it is preparing to launch a commercial version of its own AI model that can create text, imagery and code. This could see Meta, which has access to swathes of critical data that can feed AI models, catch up with its rivals that are currently have a lead in the race for AI supremacy.

Amazon stock: Q2 earnings preview

The outlook for Amazon is becoming rosier as the volatile comps seen in recent years finally starts to normalise, although most of its businesses remain highly sensitive to the economy and it is still struggling with inflationary pressures.

Ecommerce sales have fallen for two consecutive quarters but are seen rebounding this time around, with analysts predicting 2.9% year-on-year growth. The outlook here for the third quarter has already been flattered by news that its recent Prime Day sales event was the biggest on record.

Amazon Web Services, which is the real engine that drives profits, is expected to see revenue grow 10% from last year to $21.7 billion, marking the sixth consecutive quarter of slower growth as businesses scale-back their IT spending, with markets not expecting this to start growing again until late 2023. Amazon has remained quiet on the AI front and investors will want to know if it can follow Microsoft by countering the drop in enterprise spend with new workloads, but it is likely to be behind its rival in this early stage of the race.

Its small but fast-growing advertising business is forecast to report a 16.4% rise in sales, which has also slowed down lately but remains a welcome result when you consider the challenging conditions being faced by Meta and Alphabet. Growth from its subscription business remains stable as consumers continue to assign value to Prime and its other services.

Operating profit is estimated to jump 41.5% to $4.7 billion and markets think this will more than double year-on-year in the third and fourth quarters thanks to more normal comps.

Still, costs are still rising at a faster pace than revenue and this may heighten the need to get a tighter grip. Fulfilment and everyday costs are falling but Amazon continues to raise spending on technology and marketing.

Amazon is only trading at around half the peaks we saw in 2021 despite being a much larger and more profitable business today than back then, suggesting there is plenty of room for shares to keep up the momentum.

Apple stock: Q3 earnings preview

Apple’s results have been uninspiring so far this financial year but this has not stopped the company from climbing to fresh all-time highs and earnings that $3 trillion valuation. Forecasts for this quarter are not overly rousing either with sales forecast to fall for a third consecutive quarter and earnings predicted to come in flat.

Revenue is expected to fall 1.8% from last year at $81.5 billion. Weak demand for hardware remains the problem. iPhones, which account for over half of revenue, are expected to be down 2.2% at $39.8 billion while appetite for Macs and iPads remains under pressure. Don’t forget, Apple is likely to unveil its newest iPhone in September so demand starts to taper off as consumers wait for the newer model.

The new Vision Pro headset has helped drive Apple shares higher, although don’t expect any sort of material contribution to its financial results until 2024 at the earliest (and probably later) following troubles establishing a supply chain due to its complex design.

Its services arm, underpinned by the likes of the App Store, Apple Pay, AppleCare and Apple Music, should continue to steadily grow and see sales rise 5.8% to $20.7 billion.

North America is where demand is faltering the most. China has failed to provide a boost since reopening and analysts think this will have remained the case in the third quarter, although there is potential for surprise here – as well as from newer emerging markets such as India.

Adjusted EPS forecast to edge up just 0.2% from last year to $1.20. That would be the slowest of any Big Tech member. Apple often beats expectations by flexing buybacks, although analysts think these will slow to less than $18.5 billion in the third quarter from around $19.5 billion in the first two.

Big Tech and AI valuations

Markets have already assigned huge value to the AI prospects of some stocks, like NVIDIA, but valuations across the broader Big Tech space are not at extreme levels to suggest markets have not got carried away like they have when other breakthrough technologies have emerged in the past. For example, the Nasdaq 100 trades at a long-term price-to-earnings ratio of around 35x at present. That is above the 10-year average of just 26x but is nowhere near the extreme levels we saw just before the dot com crash in 2000, when PE ratios hit as high as 175x before the bubble popped.

The ratio stands lower at 29x based on the earnings estimates for the next 12 months. That suggests two notable things. Firstly, that expectations remain fairly tempered and that investors have not flooded into the next big thing too quickly. Secondly, it suggests AI is yet to drive an upgrade in earnings estimates in the broader market as companies and investors try to find their footing in this new rapidly-developing industry.

That appears true for Apple, Microsoft, Amazon, Meta and Alphabet – with valuations currently lingering only marginally above the historic averages we have seen over the past decade. This suggests AI still has the potential to significantly boost share prices if they can monetise their efforts.

Picks and shovel stocks like semiconductor makers and hardware manufacturers are set to be the first to benefit but those supplying critical infrastructure, such as cloud computing companies, should follow closely behind.

Microsoft is a leader in this group considering its cloud arm is already working on generative AI workloads due to its relationship with Chat GPT owner Open AI, and looks ready to deploy the first commercial AI-infused tools. The pressure is building for the others to catch up, but it is still very early days and not many are better positioned than data-rich Big Tech.

Big Tech has got us excited about the game-changing potential of AI but will come under increasing pressure as time goes on to show us how. You can find out more in What is the Outlook for AI Stocks in H2 2023?

Where next for Big Tech stocks?

This is expected to be a tough earnings season for the S&P 500, which is forecast to see the sharpest drop in quarterly earnings in two years. But Big Tech’s scale and stability have helped drive the markets higher in 2023 and, with the majority expected to grow their bottom-lines, they could come to the rescue once again.

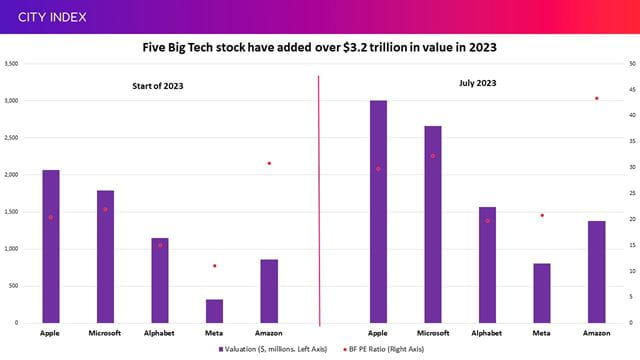

However, valuations have exploded this year, albeit from a low-base following the selloff we saw in 2022. The group of five alone has added over $3 trillion in value in just over six months, and that has led to higher multiples. That means the bar is getting higher and the outlook more challenging and this could make it harder for them to find higher ground for the remainder of this year, but Big Tech has what it takes to keep outperforming the wider market - especially if they reap rewards from AI catalysts, which should start coming into play later this year before taking-off in 2024.

Any disappointment this earnings season could result in a pullback in these valuations, and AI-boosted premiums could erode if they fail to monetise them quickly enough this year. It is worth remembering that Big Tech tends to outperform the markets when they are rising, but usually underperform when markets are in decline.

Take advantage of extended hours trading

The five tech behemoths will release earnings after markets close and most traders must wait until they reopen the before being able to trade. But by then, the news has already been digested and the instant reaction in share price has happened in after-hours trading. To react immediately, traders should take their positions in pre-and post-market sessions.

With this in mind, you can take advantage of our service that allows you to trade Big Tech stocks using our extended hours offering.

While trading before and after hours creates opportunities for traders, it also creates risk, particularly due to the lower liquidity levels. Find out more about Extended Hours Trading.

How to trade Big Tech stocks

You can trade Big Tech stocks and indices with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the stock or index you want in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Or you can practice trading risk-free by signing up for our Demo Trading Account.

Latest market news

Yesterday 01:32 PM

Yesterday 09:35 AM

Yesterday 07:23 AM

Yesterday 04:48 AM

Yesterday 12:17 AM

July 25, 2024 10:39 PM

Latest Equities articles

June 8, 2024 02:00 AM

June 3, 2024 05:56 AM

June 3, 2024 03:34 AM